DAILY MORNING NOTE | 18 May 2026

Recent Podcasts:

Wee Hur Holdings Ltd – Construction and worker dorm anchor growth

Advanced Micro Devices Inc. – Clear Instinct GPU roadmap, strong CPU demand

Netflix Inc. – Content, ads, and scale drive the next leg of growth

Week 21 equity strategy: It has been a busy week of results. Let me share some broad takeaways:

(i) Genting Singapore: The results disappointed, with net profits falling 55% YoY. There was a significant market share loss in VIPs from an estimated 30% in 4Q25 to 20% in 1Q26. Credit provided was more selective. We think the company looks more interesting in 2029 when closer to completing RWS 2.0. It is now a WIP site.

(ii) SIA : SIA is faring much better than other airlines. It is adding capacity and taking share from Middle East airlines as its customers turn more cautious on their hubs. Air India remains a bugbear with no visibility of an immediate turnaround. A precursor to jet fuel disruption is rationing, and that has not happened to SIA.

(iii) SingPost: Underlying net profit in FY26 is S$10mn from SingPost Centre (SPC), which is weighted down by losses in the letter and postal network. It announced a restructuring to keep the SPC and turnaround losses in other divisions. There is upside in earnings from the pending IMDA review, monetising warehouses, the January postal hike, and leasing out more space at SPC.

(iv) AEM: Raised revenue guidance by 20% to around 44% YoY growth for FY26. Revised forecast is due to demand from its new GPU customer, which is pushing this year’s demand. The existing CPU customer is gaining momentum, but yet to fully ramp up with its new foundry opportunities and rise in CPU demand from agentic AI.

(v) First Resources: Backdrop for palm oil is positive. Indonesia’s move to B50 3.6mn tonnes of demand or 4% of global demand. The spike in diesel price has also led equipment makers to use B100 or full biodiesel. The risk of a Godzilla El Niño and under-fertilisation could suppress production significantly next year.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

US stocks retreated from artificial-intelligence-fuelled record highs on Friday (May 15), as spiking crude prices ignited global inflation fears. All three major US stock indexes veered sharply lower, each shedding more than 1 per cent as a jump in benchmark Treasury yields, reflecting surging energy prices and concerns about long-term inflation, offered an attractive alternative to higher-risk equities. Despite the sell-off, the S&P 500 logged its seventh straight weekly gain, its longest since a nine-week streak ended in December 2023.

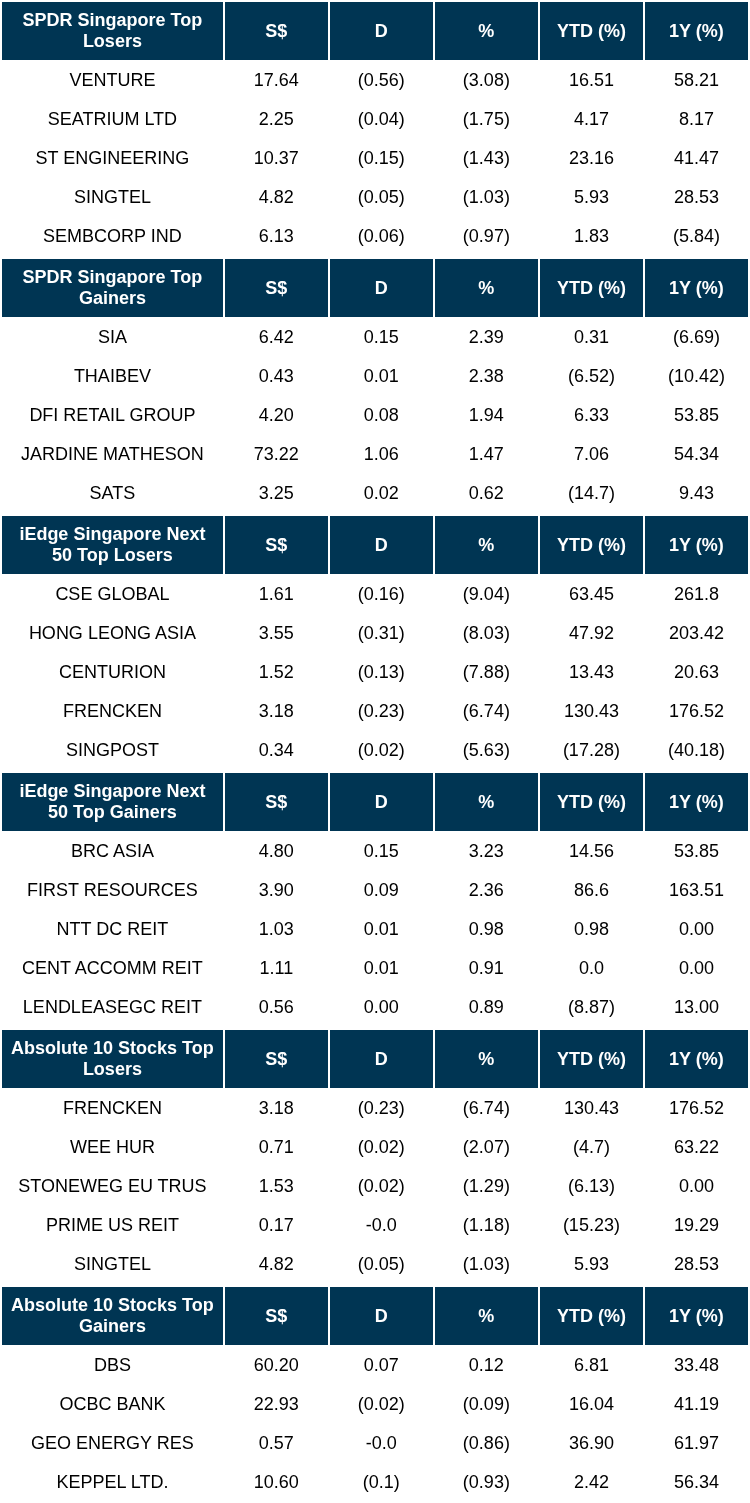

Singapore stocks ended lower on Friday (May 15). Stocks lost 0.1 per cent or 6.86 points to finish at 4,989.08. Singapore Airlines led the gainers, rising 2.4 per cent or S$0.15 to S$6.42. The worst performer was Venture Corporation, which fell 3.1 per cent or S$0.56 to close at S$17.64. The three local banks ended mixed on Friday. DBS rose 0.1 per cent or S$0.07 to S$60.20, while OCBC fell 0.1 per cent or S$0.02 to S$22.93 and UOB finished 0.2 per cent or S$0.07 lower at S$37.30.

Singapore Technical Highlights

TOP 5 GAINERS & LOSERS

EVENTS OF THE WEEK

SG

Singapore Technologies Engineering‘s 1QFY2026 revenue was up 11% y-o-y to $3.26 billion, with “strong” growth across its various segments. The company plans to pay an interim dividend of four cents per share for 1QFY2026. ST Engineering’s defence and public security segment, which has been enjoying strong momentum in new orders won, was the largest revenue contributor with an increase of 7% to $1.41 billion.

Data centre operator DayOne is considering a US$5 billion dual Singapore-Nasdaq IPO. The listing will likely be one of the first under the so-called Global Listing Board (GLB), which lets companies with a market cap of at least $2 billion list on both exchanges using the same prospectus. Singapore-headquartered DayOne is expected to have a market cap of US$20 billion with the IPO.

Most retail investors will no longer be required to seek mandatory financial advice before purchasing complex investment products such as investment-linked policies (ILPs). This comes under changes finalised by the Monetary Authority of Singapore (MAS) on Friday (May 15). The move aims to provide investors the flexibility to opt in or out of financial advice.

National power company SP Group and EV-Electric Charging debuted the first electric vehicle (EV) fast-charging hub within an HDB car park on Saturday (May 16). EV-Electric Charging is the unit of Land Transport Authority that is rolling out Singapore’s charging network.

US

China has agreed to purchase at least US$17 billion of agricultural products from the US annually to 2028. China said it agreed with the US to lower levies on some products to promote bilateral trade, underscoring how ties between the world’s two largest economies are further stabilising after the historic meeting of the leaders.

Tesla raised the prices of its Model Y cars in the United States on Saturday, according to its website. The company increased the price of its Model Y premium all-wheel drive and Model Y premium rear-wheel drive by US$1,000 to US$49,990 and US$45,990 respectively. The company also raised the price of its Model Y Performance all-wheel drive to US$57,990 in the United States, up US$500 from earlier, the website showed. In August last year, the company raised the price of its most-expensive Cybertruck pickup truck model by US$15,000 in the United States despite softer-than-expected sales and recalls. Tesla did not provide a reason for the price increase. The last time the company increased the price of Model Y cars was two years in 2024 ago.

Starbucks is planning to open a technology office in India as the coffeehouse chain seeks to cut US$2 billion in costs. The new hub is slated for the company’s fiscal year 2027, which starts in October, according to a message sent to workers and seen by Bloomberg News. It will be the company’s first corporate office in India, and Starbucks expects to start recruiting there once it settles on a site later this year.

Arm Holdings is facing an antitrust investigation by the US Federal Trade Commission (FTC) over the UK company’s licensing of its semiconductor technology, part of ongoing global scrutiny of the business. The US competition and consumer protection regulator is probing whether Arm is trying to illegally monopolise parts of the semiconductor market.

SpaceX notified investors that it is executing a 5-for-1 stock split, a move that will reduce the price investors will pay for each share offered in its impending initial public offering. Shareholders were notified in an e-mail that the current fair market value per share has been adjusted to about US$105.32 from US$526.59 as a result of the split. SpaceX is aiming to list its shares as early as Jun 12 and has picked the Nasdaq as the trading venue for its blockbuster market debut.

Amazon.com was sued on Friday (May 15) by consumers seeking refunds for costs passed on to them in the form of higher prices as a result of tariffs the US Supreme Court later concluded had been unlawfully imposed by US President Donald Trump. Consumers in a proposed class action filed in federal court in Seattle alleged that the e-commerce giant collected hundreds of millions of US dollars in unlawful tariff costs by raising prices on imported goods before the Supreme Court had ruled.

Tata Electronics and ASML on Saturday signed an agreement to build India’s first front-end semiconductor fabrication plant in the state of Gujarat, as the country accelerates efforts to develop a domestic chip industry.

Oil prices gained more than 3 per cent on Friday (May 15), after comments by US President Donald Trump and Iran’s foreign minister further dented hopes of a deal to end ship attacks and seizures around the Strait of Hormuz. Brent crude futures settled at US$109.26 a barrel, up US$3.54, or 3.35 per cent.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Centurion Corporation Ltd – Entry into key worker accommodation

Recommendation: BUY; TP S$1.85; Last close: S$1.5200; Analyst Yik Ban Chong (Ben)

- Centurion Corporation Limited (CCL) released 1Q26 update with limited financials. 1Q26 revenue is within our expectations, at 24% of our FY26e forecast. 1Q26 revenue spiked up 30% YoY to S$89.4mn, driven by revenue growth across all PBWA and PBSA segments. 1Q26 revenue included an additional 55% stake of 8000-bed Westlite Mandai, and additional 5,460 new beds (+16% capacity) from AEI expansion, driving Singapore revenue up 29% YoY to S$62.6mn.

- CCL entered Australian key worker accommodation (KWA) through two separate acquisitions in Apr 2026 – 321 beds in Karratha, and 125 beds in South Hedland. Both Karratha and South Hedland are in Pilbara region, which produces approximately 96% of Australia’s iron ore export. We estimate the KWAs could contribute ~S$6.5mn in FY26e revenue (2% of FY25 revenue), assuming acquisitions complete from Jul 2026.

- We maintain BUY with a higher TP of S$1.85 (prev. S$1.81). We raised FY26e revenue/adj. PATMI by 6%/8% respectively, due to higher contributions expected from management contract secured for a 1500-bed third-party dormitory, EPIISOD Macquarie Park, and Australia KWA. Management service fees of CAREIT contributed S$7mn to 1Q26 revenue (1Q25: S$0.2mn). We expect CAREIT management fees to contribute ~S$16mn to FY26e PATMI (15% of FY25 adj. PATMI).

NetLink NBN Trust – Fixed cost creeping up but cash stable

Recommendation: NEUTRAL; TP S$0.96; Last close: S$1.0200; Analyst Paul Chew

- FY26 revenue met our expectation, but EBITDA was below at 100%/96% respectively, of our forecast. 2H26 DPU improved 1.1% YoY to 2.71 cents. FY26 DPU was 1.1% higher at 5.42 cents. 2H26 EBITDA declined 5% YoY to S$143.5mn. The higher contribution of non-RAB revenue and staff costs pressured margins.

- Residential fibre connections have started to recover in 2H26 (+3.7k) after the major contraction in 1H26 (-9.7k). Operators have been removing inactive connections as plans upgrade from 1GB to 10GB. Gross connections have been stable.

- The target price is raised to S$0.96 (prev. S$0.93) as we roll forward our valuations. Our NEUTRAL recommendation is unchanged. Operating cash flow remains stable at S$258mn, covering the S$211mn in dividends. Capital expenditure is to fund future returns. NetLink’s distribution yield of 5.4% is supported by its stable cash flows. We expect FY27e to be affected by rising fixed operating costs and finance expenses.

SIA Engineering Co. Ltd – Poised for growth amid geopolitical headwinds

Recommendation: BUY; TP S$4.06; Last close: S$3.1500; Analyst Hashim Osman

- 2H26/FY26 PATMI rose 20.9%/21.0% YoY to S$85.6mn/S$168.9mn, forming 47.8%/94.4% of our FY26e estimates. This was primarily driven by a 22.5% surge in associates and JV income in FY26.

- Associates and JV income rose 22.5% YoY to S$145.3mn. The engine and component segment was the primary driver, up 23.1% to S$139.2mn, driven by higher engine repair deliveries. Airframe and line maintenance contributed S$6.1mn (+10.9%), supported by a 3.3% increase in flights handled at Changi.

- We upgrade to BUY from ACCUMULATE with TP of S$4.06 (Prev: S$4.14) due to share price weakness. We roll forward our financials and reduce P/E multiple from 26x to 25x to account for heightened sector-wide risk from the US-Iran conflict. Future growth drivers include: i) SAESL engine capacity increasing 33% to 400 engines p.a. by 2028, ii) new Pratt & Whitney GTF engine-related coating capabilities in 2027 to capture the elevated shop visit volumes, and iii) expansion of landing gear and airframe maintenance capacity across Southeast Asia.

Thai Beverage PLC – Record gross margins

Recommendation: BUY; TP S$0.53; Last close: S$0.4300; Analyst Paul Chew

- Results were within expectations. 1H26 revenue/PATMI were 50%/59% of our forecasts. 1H is seasonally stronger. Gross margins expanded by 1.7% points to a record 32.3% in 1H26 due to lower material costs, namely malt and molasses. There was a THB1.7bn impairment on its 25% stake in e-commerce company NocNoc that was wound down.

- Underlying PATMI grew 8.5% YoY to THB16bn, largely driven by 41% growth in beer earnings. Despite volume contraction 0.6% YoY, margins expanded by 2.4% points to 27.6% from a massive 6% points decline in material costs. Spirits (73% of net profits) grew 5.6% from a modest 1% rise in margins due to lower material and operating costs.

- We upgrade our recommendation from ACCUMULATE to BUY due to recent share price performance. Our FY26e earnings and target price of S$0.53 are unchanged. Our valuations are based on 12x FY26e PE or the 4-year average forward PE. Consumer spending remains sluggish, but the company is realigning marketing and admin spend, raising prices and right sizing packaging. The lower raw material cost should persist till year-end as purchases we made before the recent Middle East conflict. The upcoming World Cup should give a volume lift in 2H26.

Sea Ltd.- 2026 an investment year

Recommendation: BUY; TP US$170.00; Last close: US$88.23; Analyst Helena Wang

- Both 1Q26 revenue was in line with expectations, while PATMI underperformed slightly due to sharply increased growth investments in Shopee. (Sales & Marketing expense +52% YoY). 1Q26 revenue/PATMI was at 24%/22% of our FY26e estimates.

- Revenue delivered strong growth of 47% YoY, supported by strong Shopee growth (+44% YoY), rapid loan-book expansion at Monee (+41% YoY), and continued strength at Garena (bookings +20% YoY).

- We maintain our BUY recommendation, with an unchanged Target Price of US$170.00. We increase our FY26e and FY27e sales and marketing expense assumptions by 3% and 2% (56 % of OPEX) to account for the increase in investment. Revenue, Adj. PATMI, terminal growth and WACC assumptions remain unchanged. We believe the investments are strategically beneficial over the longer term as they support user acquisition, merchant retention and ecosystem engagement, strengthening Shopee’s competitive moat.

Market Journal articles powered by PhillipGPT

Meta Platforms Inc. Upgraded to BUY Despite Higher CAPEX Concerns, US$795 Target Price

Sheng Siong Group Delivers Strong Growth with Market Share Gains, Target Price Raised to S$3.16

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Centurion Corporation Limited

Date & Time: 19 May 26 | 12PM-1PM

Register: poems-20260519-145629

Corporate Insights by OxPay

Date & Time: 20 May 26 | 12PM-1PM

Register: poems-20260520-145503

Corporate Insights by Yoma Strategic Holdings Ltd [NEW]

Date & Time: 3 June 26 | 12PM-1PM

Register: poems-20260603-148171

Corporate Insights by First REIT

Date & Time: 11 June 26 | 12PM-1PM

Register: poems-20260611-146839/a>

Corporate Insights by AIMS APAC REIT

Date & Time: 17 June 26 | 12.30PM-1.30PM

Register: poems-20260528-145702

POEMS Podcast:

Research Videos

Weekly Market Outlook: AAPL, Disney, Grab Holdings, PLTR, AMD, UOB, OCBC, SG Weekly & More!

Date: 11 May 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials