DAILY MORNING NOTE | 2 February 2026

Recent Podcasts:

Netflix Inc. – Content, ads, and scale drive the next leg of growth

The Walt Disney Company – Streaming Turns Profitable

Nvidia 3Q26 Results

Analyst: Zane Aw

- Review of asset classes performance in January – Most ETFs were in the green, except those tracking US Treasury Bonds (IEF) and Bitcoin (BITO), which fell 0.2% and 4.6% respectively. The top gainer was the ETF tracking Oil (XOP), which surged 11%.

- For their current trends, the S&P 500, Gold and Singapore Equities are in an uptrend. Meanwhile, US Treasury Bonds, Oil and the Hang Seng Index are in a range consolidation. On the other hand, Bitcoin is in a downtrend.

- Heading into February, we expect gains for the ETFs tracking the S&P 500, Oil, Singapore Equities, and the Hang Seng Index. On the other hand, ETFs tracking Gold and Bitcoin are likely to pull back. Meanwhile, the ETF tracking US Treasury Bonds is likely to remain rangebound.

Trades Initiated in Past Week

Week 6 equity strategy – Singapore equities rose 5.6% in January, registering a record of nine consecutive months of gain that totalled 28%. Property and construction were the outperformers in January with a gain of 16%. There is still strength in this equity rally, in our opinion. In the US, GDP Now is tracking at 5% growth, the highest since 3Q23. For Singapore, economic conditions are vibrant. Industrial production surged 19% YoY in 4Q25, underpinned by electronics demand from semiconductors and hard disk drivers.

Supplementing the growth is a major capital spending cycle in semiconductors, renewables, AI and construction. There is room for valuation expansion with the current low interest rates of 1.16% (3M SORA), which has more than halved (Figure 13), and captive EQDP+ liquidity flowing into Singapore equities can create a liquidity premium. Singapore equities are trading at 16x forward PE against its 25-year historical average of 15x. With earnings momentum and valuation expansion, we believe it is plausible to reach the 1SD valuation of 19x, implying a target index of 5700, or a gain of 15%.

The two sectors with visibility and momentum are semiconductors and construction. TSMC raising its capex outlook significantly over the next three years has seen ASML bookings spike 85% YoY in the December quarter to EUR13bn. This is a positive for Frencken, which is a key parts supplier. ASML is trading at 50x PE. In construction. BCA raised its construction demand guidance for 2026 by 18% from S$42.5bn to S$50bn (mid-point). There will be a slew of construction contracts in 2026. There are the massive T5 tenders, followed by hospitals, BTOs, Marina Bay Sands and Harbour Front Redevelopment. Residential property is another bright spot. Demand is healthy and underpinned by low interest rates, HDB upgraders, population growth, wealth transfer by parents, lifestyle choices and low unsold inventory for launch.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

The local benchmark index slid 0.5% or 24.9 points to 4,905.13, with index heavyweights DBS, UOB and OCBC all finishing lower.

The S&P 500 fell 0.43% to finish at 6,939.03, its third straight down day. The Dow Jones Industrial Average pulled back 179 points, or 0.36%, to settle at 48,892.47. The tech-heavy Nasdaq Composite underperformed, dropping 0.94%, to end the day at 23,461.82. All three indexes fell more than 1% at session lows.

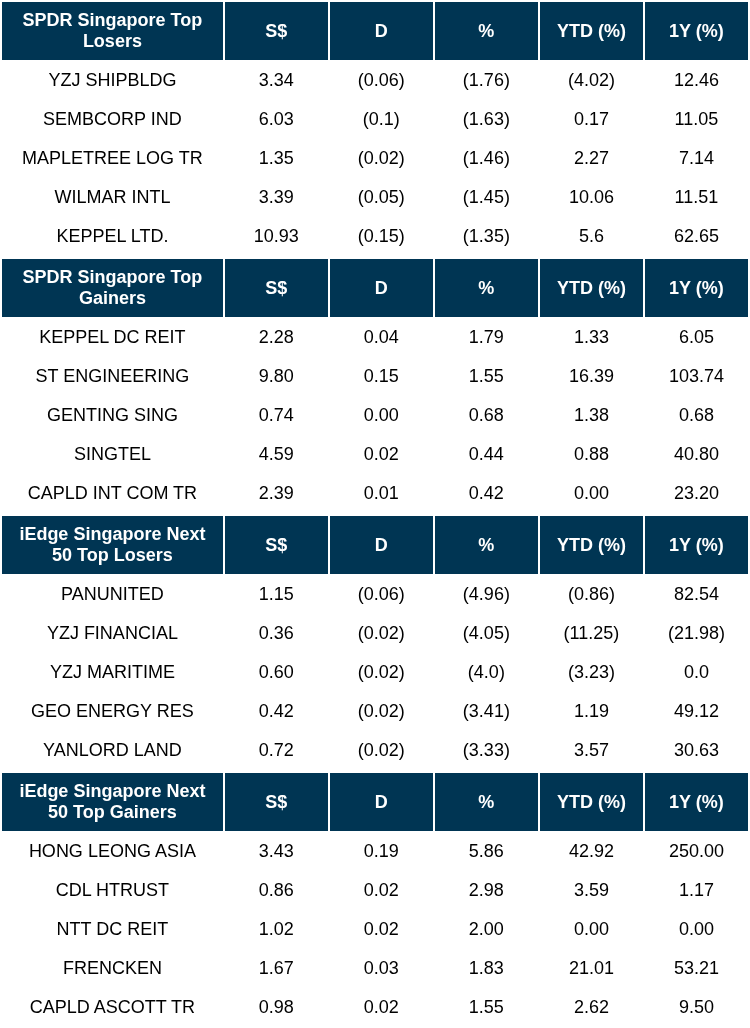

Singapore Technical Highlights

TOP 5 GAINERS & LOSERS

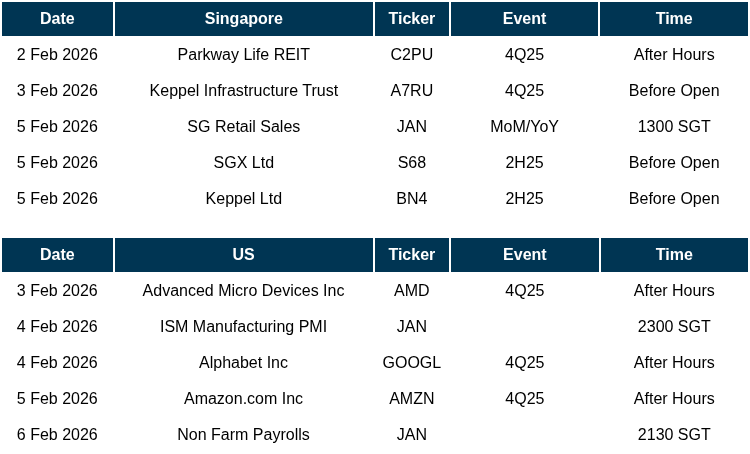

Events Of The Week

SG

CDL’s Newport Residences sells 57% or 140 of its units at launch.

Moneymax announced it is expected to record a significant YoY improvement in its profit net of tax for 2H2025 and FY2025.

Rex International Holding Limited announced a discovery has been made in the “Knockando Fensfjord” prospect in the Brage Field in which Rex’s indirect subsidiary Lime Petroleum AS has a 33.8% interest.

AcroMeta secures S$1 million subscription, shares to be issued at the higher of S$0.06 per share or a 10% discount to the average weighted price per share.

Singapore’s bank lending in December 2025 charted the highest monthly increase since December 2024, driven primarily by an increase in loans to businesses.

Co-living operator Coliwoo Holdings is acquiring 2 Changi Business Park Avenue 1 for S$101 million.

Reclaims Global is planning a one-for-one bonus share issue to improve accessibility for investors

iWow Technology plans to acquire company providing meals for elderly for $11.2 million.

Fu Yu Corp has appointed its largest shareholder Victor Lim as managing director, with effect from Feb 1.

Singtel and KKR are nearing a deal to buy ST Telemedia Global Data Centres in a deal that values the assets at more than $13 billion .

US

Nvidia Corp’s negotiations to invest as much as US$100 billion ($126.99 billion) in OpenAI have broken down.

Oracle has been awarded an $88 million firm-fixed-price task order for the U.S. Air Force’s Cloud One program.

Oracle said it expects to raise between $45 billion and $50 billion of gross cash proceeds in 2026, through a mix of debt and equity financing.

SpaceX generated about US$8 billion in profit on US$15 billion to US$16 billion of revenue last year, two sources familiar with the company’s results said.

Boeing has been awarded a $2.8 billion contract to upgrade F-15 fighter jets for the Republic of Korea Air Force, the U.S. Department of War announced Friday.

Waymo, Alphabet’s autonomous driving unit, is aiming to raise about US$16 billion in a financing round that would value the unit at nearly US$110 billion

Alphabet’s Google persuaded a federal judge in San Francisco on Friday to reject a bid by consumers for more than $2 billion in penalties over the company’s past collection of data from users who had switched off a key privacy setting

Northrop Grumman Systems Corp. has secured a $50 million contract from the U.S. Department of War for commercial agile software development services.

President Donald Trump said he intends to nominate Kevin Warsh to be the next chair of the Federal Reserve.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

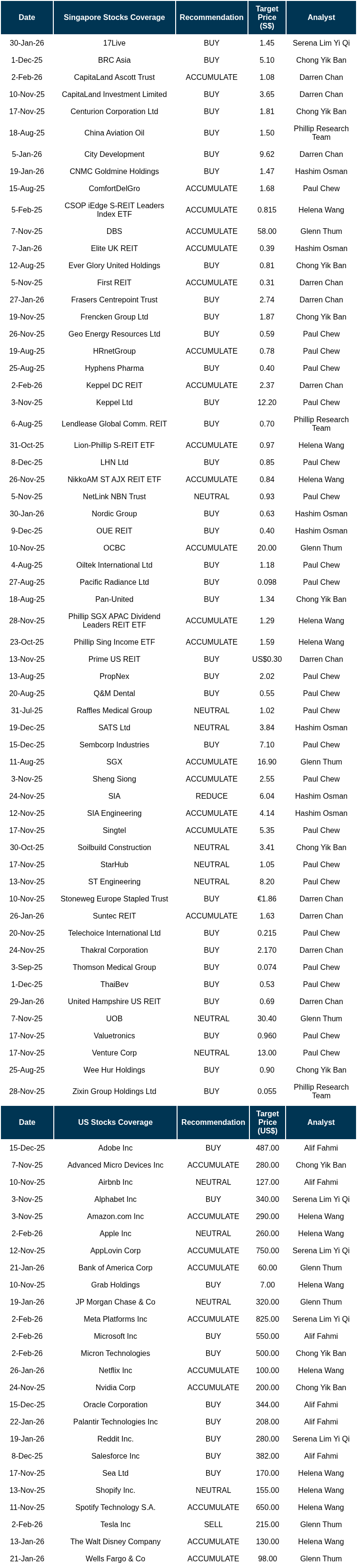

RESEARCH REPORTS

CapitaLand Ascott Trust – Stable DPU for 2026

Recommendation: ACCUMULATE; TP S$1.08; Last close: S$0.9800; Analyst Darren Chan

- FY25 DPU of 6.10 Singapore cents was stable YoY, in line with our expectations. Income available for distribution rose 11% YoY to S$256.7mn, driven by stronger operating performance and portfolio reconstitution initiatives. After retaining S$23.2mn to fund asset enhancement initiatives (AEI) and working capital, total distribution to unitholders rose 1% YoY to S$233.5mn.

- 4Q25 portfolio RevPAU rose 2% YoY to S$180 (FY25: S$161, up 3% YoY), driven by a 2ppt increase in occupancy to 83%. CLAS reported a 1.7% increase in portfolio valuations for the year, driven by stronger operating performance.

- Maintain ACCUMULATE with a higher DDM-TP of S$1.08 (prev. S$1.05) as we roll forward our forecasts. CLAS remains our top pick in the hospitality sector, underpinned by its balanced mix of stable (FY25: 65%) and growth income streams, alongside strong geographical diversification for earnings resilience. We expect low single-digit portfolio RevPAU growth in FY26e, supported by improving occupancy. CLAS has guided to a stable DPU YoY for FY26e at 6.1 Singapore cents, supported by past divestment gains used to offset the impact of major ongoing AEIs. There is over S$300mn of such gains still available on the balance sheet. The current share price implies an FY26e dividend yield of 6.2%.

Keppel DC REIT – Record high DPU

Recommendation: ACCUMULATE; TP S$2.37; Last close: S$2.2800; Analyst Darren Chan

- 2H25/FY25 DPU of 5.248/10.381 Singapore cents (+7.1%/+9.8% YoY) was in line with our expectations, forming 51%/102% of our FY25e estimates. The YoY growth was driven by the acquisitions of KDC SGP 7 & 8 and Tokyo DC 1 & 3, stronger contributions from contract renewals and escalations, and lower finance costs.

- Portfolio occupancy remained stable at 95.8% QoQ. FY25 portfolio rental reversion was strong at +45% (4Q25: +2%, with no major contract renewals). Portfolio valuations rose 25.6% YoY to S$6.1bn, driven by acquisitions. On a same-store basis, it rose 3.7%.

- We upgrade from NEUTRAL to ACCUMULATE due to the recent share price performance, with a lower DDM-derived TP of S$2.37 (prev. S$2.40) as we roll forward our forecasts. We lower our FY26e DPU by 6%, reflecting the loss of income from the divestment of NetCo bonds and slightly higher assumed finance costs. The potential recovery of over S$50mn in overdue rent from Bluesea remains a key catalyst, though still unresolved. Additionally, the granting of tax transparency for SGP 7 & 8 in the coming months should provide further upside to DPU. We expect the strong positive rental reversion momentum to continue into FY26, particularly from Singapore colocation lease renewals. The stock trades at an FY26e DPU yield of 4.8%.

Phillip Singapore Monthly: February 2026 – Breaking Records

Analyst: Paul Chew

- Singapore equities rose 5.6% in January, registering a record nine consecutive months of gain that totalled 28%. Property companies led the advance, driven by attractive valuations and optimism on new launches, due to favourable interest rates and a reduced risk of cooling measures. Shipyards retreated over soft container rates and litigation concerns.

- Economic conditions in Singapore are vibrant. Industrial production surged 19% YoY in 4Q25, underpinned by electronics demand. A major capital spending cycle is underway. Semiconductor equipment spending will trend up following TSMC’s guidance of significantly higher Capex over the next three years. 2026 will be another record year of construction demand in Singapore, led by massive T5 contracts. It will benefit the entire supply chain, including contractors, building materials, and related property services (dorms and co-living).

- Singapore equities are trading at 16x forward PE against its 25-year historical average of 15x. With momentum in earnings and valuation expansion from low interest rates and EQDP+ flows, we believe it is plausible to reach the 1SD valuation of 19x, implying a target index of 5700, or a 15% gain.

SG Bonds – Week 06 : SGS yields ease across the curve

Recommendation: REDUCE; TP S$; Last close: S$; Analyst Phillip Research Team

- U.S. Treasury yields were mixed over the week. Front-end yields declined, with the 2Y and 5Y falling 5bp and 7bp WoW, respectively, while the 10Y was broadly unchanged. In contrast, long-end yields edged higher, with the 30Y rising 4bp to 4.87%.

- SGS yields drifted lower, with the 2Y down 2bps WoW, while the 5Y and 10Y declined by 7bps and 6bps, respectively.

- Looking ahead, Fed funds futures currently price one 25bps rate cut around the June 2026 meeting, followed by a second cut later in 2H26, taking the implied policy rate toward the 3.1–3.2% range by end-2026, with little additional easing priced into 2027. Domestically, MAS kept its policy stance unchanged, with the decision carrying a mild hawkish tilt. While growth remains firm, uncertainties around the durability of the AI-driven upswing and its spillovers suggest that the April review may be too early for any policy adjustment. With inflation pressures still broadly contained, MAS is likely to stay on hold in the near term, leaving the July review as the more relevant checkpoint should inflation prove more persistent.

Apple Inc. – Booming iPhone 17 VS soaring memory costs

Recommendation: NEUTRAL; TP US$260.00; Last close: US$259.48; Analyst Helena Wang

- 1Q26 revenue and PATMI were within our expectations. Revenue grew 16% YoY, fastest growth in four years, mainly driven by growth in iPhone (+23% YoY) and China market (+38% YoY). 1Q26 revenue/PATMI were at 31%/34% of our FY26e forecasts.

- Demand for the iPhone 17 lineup remains strong, with current demand outpacing supply. Management guided 2Q26e revenue growth of 13–16% YoY, supported by continued iPhone sales momentum. Rising memory costs are expected to become more pronounced in the coming quarters, posing a margin headwind in the long run.

- We raise our FY26e revenue and PATMI assumption by 2% and 3%, respectively, to account for the strong growth in iPhone 17. We have also increased our terminal growth rate from 3.0% to 3.5% to reflect the long-term monetization potential from AAPL’s collaboration with Gemini, which strengthens Apple Intelligence and supports sustained ecosystem engagement. We upgrade our recommendation from REDUCE to NEUTRAL, raising the DCF target price to US$260 (prev. US$230). WACC of 6.5% remains unchanged. We remain cautious on AAPL, as the stock is still in a “prove-it” phase, particularly at a ~30.7x forward FY26 P/E. Ultimately, AAPL’s ability to sustain product-led growth and execute a successful Siri rollout will be critical to underpinning its current valuation.

Meta Platform Inc. – Resilient ad performance back strategic spending

Recommendation: ACCUMULATE; TP US$825.00; Last close: US$716.50; Analyst Serena Lim Yi Qi

- 4Q25 results exceeded our expectations, with revenue up 24% YoY to US$59.9bn and adj. PATMI increased 9% YoY to US$22.7bn, driven by robust ad revenue growth. FY25 revenue/PATMI were at 100%/110% of our FY25 forecasts. Earnings pulled down by Reality Labs losses of US$6bn in FY25.

- Video and Threads continued to show attractive monetisation and engagement opportunities, with Instagram Reels watch time increasing 30% YoY in the US, while FB video watch time grew double-digits.

- We maintained ACCUMULATE rating but raised the DCF target price to US$825 (prev. US$770). As we rolled into the new financial year, our FY26e revenue and PATMI forecast was upgraded by 7% & 8% respectively, reflecting the expected continued benefits of integrating LLMs with META’s recommendation models, which should further enhance ad efficiency and pricing.

Micron Technology, Inc – DRAM shortage fuels pricing upside

Recommendation: BUY; TP US$500.00; Last close: US$414.88; Analyst Yik Ban Chong (Ben)

- Micron’s high bandwidth memory (HBM) products are in high demand, with its HBM3E chips designed into Nvidia’s Blackwell GPU and AMD’s MI355 GPU. With industry-leading next-generation HBM4 speeds of over 11 gigabits per second (Gbps), we believe Micron can chip away SK Hynix’s market share when its HBM4 ramps beyond CY2Q26e. There is still strong demand visibility from hyperscalers, as Meta and Microsoft recently guided 2026e capex to increase by 76%/90% YoY respectively, to support growing AI demand.

- Industry memory supply shortage is driving dynamic random access memory (DRAM) prices to the highest levels since 2019. Both Micron and SK Hynix mentioned that their HBM products are sold out for 2026e. Micron and SK Hynix’s combined capex-to-sales ratio rose 6ppt YoY to 34% in 4Q25. However, we expect the capex-to-sales ratio to decline in 2026 as Micron’s capex intensity falls ahead of Idaho fab construction in 2027, while SK Hynix guided it will maintain at mid-30s levels in 2026. We are assuming 56% rise in DRAM prices for FY26e.

- We initiate coverage on Micron with a BUY recommendation, TP US$500. Our target price is based on 16.8x FY26e P/E, a 34% discount to its peers’ average FY26e P/E.

Microsoft Corp – Prioritising Azure amid supply shortage

Recommendation: BUY; TP US$540.00; Last close: US$430.00; Analyst Alif Fahmi

- 2Q26 revenue met our expectations with revenue/adj. PATMI was at 50%/51% of our FY26e forecasts. Revenue grew 17% YoY driven by 40% YoY growth in Azure cloud revenue. Adj. PATMI rose 23% YoY to US$30.9bn, driven by higher operating leverage.

- For 3Q26e, Microsoft expects revenue to rise 16% YoY to US$81.2bn, driven by continued strong growth across commercial businesses. Azure is projected to grow 37%, as the company continues to prioritise supply amid demand exceeding capacity. Commercial RPO rose 110% YoY to US$625bn and are expected to be recognised over the next 2.5 years.

- We upgrade our recommendation to BUY from ACCUMULATE with an unchanged DCF target price of US$540, due to recent price performance. There are no changes to our forecast. The company is currently valued at a blended forward PE of 23.9x, below the -1 standard deviation of 27.2x.

Tesla Inc. – All-in on autonomous vehicles and robotics

Recommendation: SELL; TP US$215.00; Last close: US$425.83; Analyst Glenn Thum

- 4Q25 results were above our expectations. FY25 revenue/adj. PATMI was at 109%/111% of our FY25e forecasts, driven by higher-than-expected auto gross margins. Adj. PATMI (excl. stock-based compensation, “SBC”) fell 16% due to a decline in vehicle deliveries, lower regulatory credit revenue, and higher OPEX from AI and R&D projects.

- 418k deliveries (-16% YoY), a record YoY decline from the removal of the US$7,500 EV tax credit. Gross margins improved by 3.8% points YoY and 2.1% points QoQ. ASPs rose by 6% YoY as selling prices of EVs rose with the removal of the EV tax credit, while auto revenue declined by 11% YoY from lowered demand due to the higher prices.

- We maintain our SELL recommendation and a lower DCF target price of US$215 (prev. US$220) as we roll over our valuations to FY26e. We lower FY26e earnings by ~29% as we lower auto revenue and raise OPEX estimates. We expect auto deliveries to continue declining in FY26e due to the removal of the US$7,500 EV tax credit in the US. Our WACC/growth rate assumptions of 9%/5% remain unchanged. We remain cautious on TSLA. It faces multiple headwinds, including tariffs, loss of tax credits, and a decline in market share in China. Significant revenue contribution from multi-year initiatives (FSD, Robotaxi, Optimus robot) is still far out (>5 years), and steep valuations of ~360x PE FY26e suggest this has already been priced in.

Nordic Group – Recurring maintenance meets capex upcycle

Recommendation: BUY; TP S$0.63; Last close: S$0.4850; Analyst Hashim Osman

- Customer capex is accelerating across Nordic’s markets such as marine, defence, and infrastructure. The book-to-bill ratio is increasing consecutively: 0.71x (FY23), 1.09x (FY24), and 1.45x (FY25e). Orders are growing faster than billings, signaling expanding backlog and future revenue growth. Future opportunities include P86/P87 FPSO tenders, Paya Lebar Air Base relocation opportunities, and Starburst’s shooting range pipeline.

- The orderbook is largely made up of high-margin maintenance services (20% net margin in FY24, 65% of order book as of Sep 2025), which generate recurring revenue from long-tail contracts. With the balance sheet approaching net cash in FY26, Nordic is well positioned to pursue earnings accretive acquisitions.

Market Journal articles powered by PhillipGPT

Bank of America Shows Strong Growth Momentum with Record Net Interest Income

JPMorgan Chase Delivers Solid Q4 Results Despite Investment Banking Headwinds

Wells Fargo Reports Mixed Q4 Results as Severance Costs Weigh on Performance

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Keppel Pacific Oak US REIT(KORE)

Date & Time: 4 February 26 | 12PM-1PM

Register: poems-20260204-138115

Corporate Insights by Keppel DC REIT

Date & Time: 4 February 26 | 3PM-4PM

Register: poems-20260204-138266

Corporate Insights by Elite UK REIT

Date & Time: 10 February 26 | 11AM-12PM

Register: poems-20260210-138117

Corporate Insights by OUE REIT

Date & Time: 12 February 26 | 12PM-1PM

Register: poems-20260212-138119

Corporate Insights by Prime US REIT

Date & Time: 13 February 26 | 12.15PM-1.15PM

Register: poems-20260213-138121

Corporate Insights by Lendlease REIT [NEW]

Date & Time: 26 February 26 | 12PM-1PM

Register: poems-20260226-138683

Corporate Insights by Stoneweg Europe Stapled Trust (SERT) [NEW]

Date & Time: 27 February 26 | 12PM-1PM

Register: poems-20260227-138685

POEMS Podcast:

Research Videos

Weekly Market Outlook: NFLX, BAC, WFC, Mag7, Suntec REIT, Tech Analysis, SG Weekly & More!

Date: 26 Jan 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials