DAILY MORNING NOTE | 2 June 2026

Recent Podcasts:

Sea Ltd.-2026 an investment year

Airbnb Inc – Modest booking and ADR growth

Wee Hur Holdings Ltd – Construction and worker dorm anchor growth

Week 24 equity strategy: Uncertainty and sensational headlines can create investment opportunities. Last year, it was the tariff war, and this year, the Middle East conflict. Equity markets have rallied to record highs as uncertainty ebbs. The latest uncertainty to have cropped up is Indonesia’s plans to create a massive state entity, Danatara Sumberdaya, to manage commodity exports (coal, CPO, ferroalloys). It is to be effective in January 2027. Indonesian commodity names are getting punished – First Resources (-32%), Geo Energy (-25%), and Golden Agri (-18%). Indonesia exports around 500mn tonnes of coal per year. In contrast, commodity giant Glencore produced and marketed around 150mn tonnes of coal in 2025. The ability to scale up, manage and buy the enormous volume of just this single commodity is monumental in the near term. We think the likeliest pathway is to report and monitor the exports for better transparency of taxes and control of the currency. Under-reporting of commodity selling prices not only lowers tax, but it also allows more foreign currency to be kept offshore. Oil prices falling by almost 19% this week is another driver of the weak sentiment. Our base case is elevated commodity prices from the rising risk of a major El Niño and the never-ending Hormuz crisis.

The AI euphoria is still alive. Last Friday, Dell shares surged 33%. 1Q27 product revenue surged 117% YoY to $38bn, and net income spiked 256% to $3.4bn. Growth came from AI servers, with an almost eightfold rise in revenue to $16bn as data centres get rolled out. Even with a $51bn AI backlog, demand exceeds supply, with memory the constraint. Even traditional servers grew 92% YoY from pull-forward orders to ensure access, support agentic AI and concerns over higher prices. PCs are also growing as customers want more capable PCs for agentic workloads. Dell is guiding 50% revenue growth for 2Q27.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore stocks ended higher on Friday (May 29) amid hopes of a US-Iran truce deal, even as regional markets showed mixed performance. The Benchmark Index gained 1% or 48.67 points to close at 5,037.86.

The S&P 500 rose on Monday, even as oil prices advanced, with Nvidia leading technology higher following the launch of a new chip for PCs. The S&P 500 index advanced 0.26% to close at 7,599.96, while the Nasdaq Composite gained 0.42% to close at 27,086.81. The Dow Jones Industrial Average added 46.42 points, or 0.09%, and ended at 51,078.88. All three indexes reached new all-time intraday highs and closed at records.

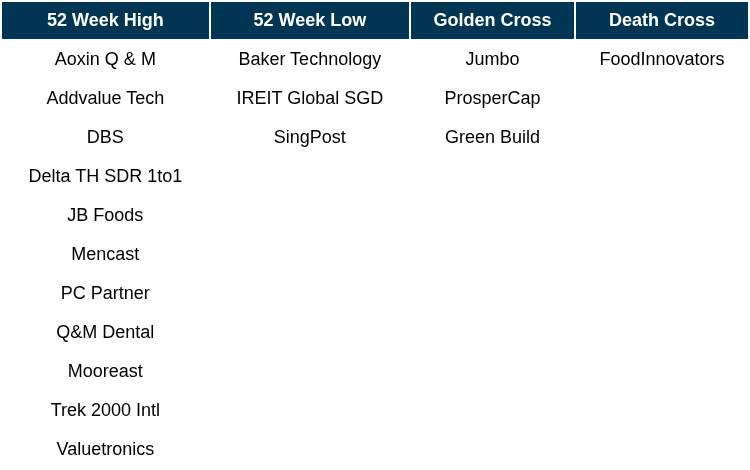

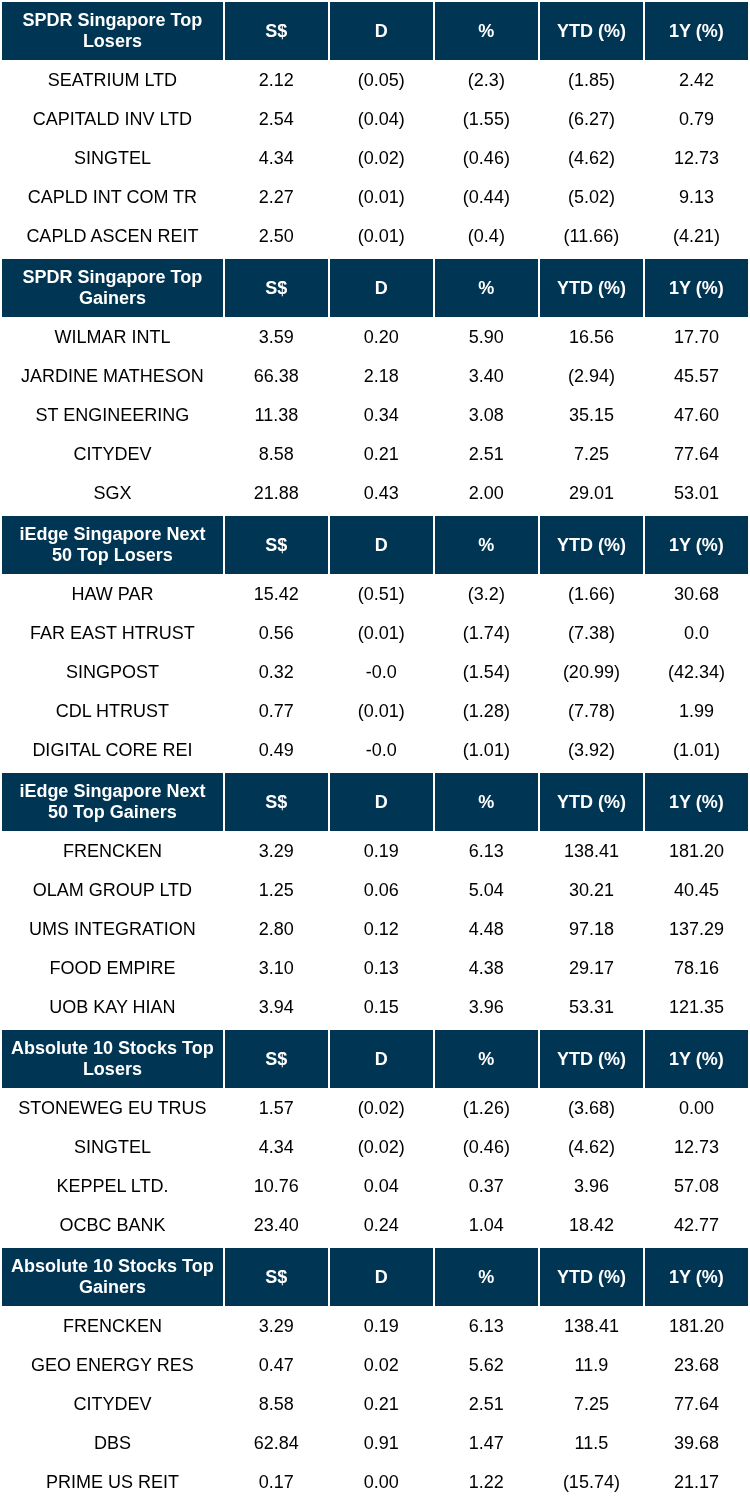

Singapore Technical Highlights

TOP 5 GAINERS & LOSERS

EVENTS OF THE WEEK

SG

CapitaLand Ascott Trust (CLAS) is selling its 336-unit The Robertson House for S$360mn (4% above book value), netting a gain of S$38.1mn.

Thakral Corporation has completed the acquisition of an additional 81.6% stake in TIL Investments, raising its ownership in a 21-acre mixed-use healthcare-led development in Gurugram, India to 95.3%.

Sembcorp Development has received investment approvals for four new Vietnam Singapore Industrial Parks (VSIPs) in Hai Phong, Ha Nam, Nghe An, and Binh Duong,

Lincotrade has secured 7 new contracts worth S$16.8mn in Q1 2026, lifting its order book to S$107mn. The company has also commenced operations at its new Tuas facility, which includes a 204-bed dormitory offering potential recurring rental income.

Concord New Energy (CNE) has entered into a S$158.2mn sale-and-leaseback deal with Industrial Bank Financial Leasing, selling equipment from its China energy-storage projects and leasing them back over 14 years.

Li & Fung Limited has announced the acquisition of a 55% stake in New Advent Global Limited, a US$1.7bn revenue product platform spanning furniture, knitwear, and beauty for US$250mn. New Advent was originally spun off from Li & Fung in 2018 and is being partially reacquired from Fung Holdings, a controlling shareholder.

Yangzijiang Shipbuilding has completed its acquisition of a 10% equity stake in Poseidon Corp. The consideration was fully paid in cash from internal resources.

Ascent Bridge Limited has completed the disposal of its wholly-owned subsidiary, MTBL Cultural Centre Pte. Ltd.

US

Nvidia is entering the PC market with its new RTX Spark Superchip, a combined CPU/GPU chip built with MediaTek that runs Windows on Arm. Launching this fall in laptops and desktops from Dell and Lenovo, it targets the premium segment and is designed to handle AI workloads and high-end gaming.

SpaceX has lowered its IPO valuation target to at least US$1.8tn (down from US$2tn), seeking to raise up to US$75bn.

Meta plans to test an AI pendant within the next year and launch a business-focused “Wearables for Work” service, as it looks to reverse losses at its Reality Labs hardware division. The company aims to sell 10mn wearable devices in H2 2026, expanding its AI glasses lineup and distribution.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

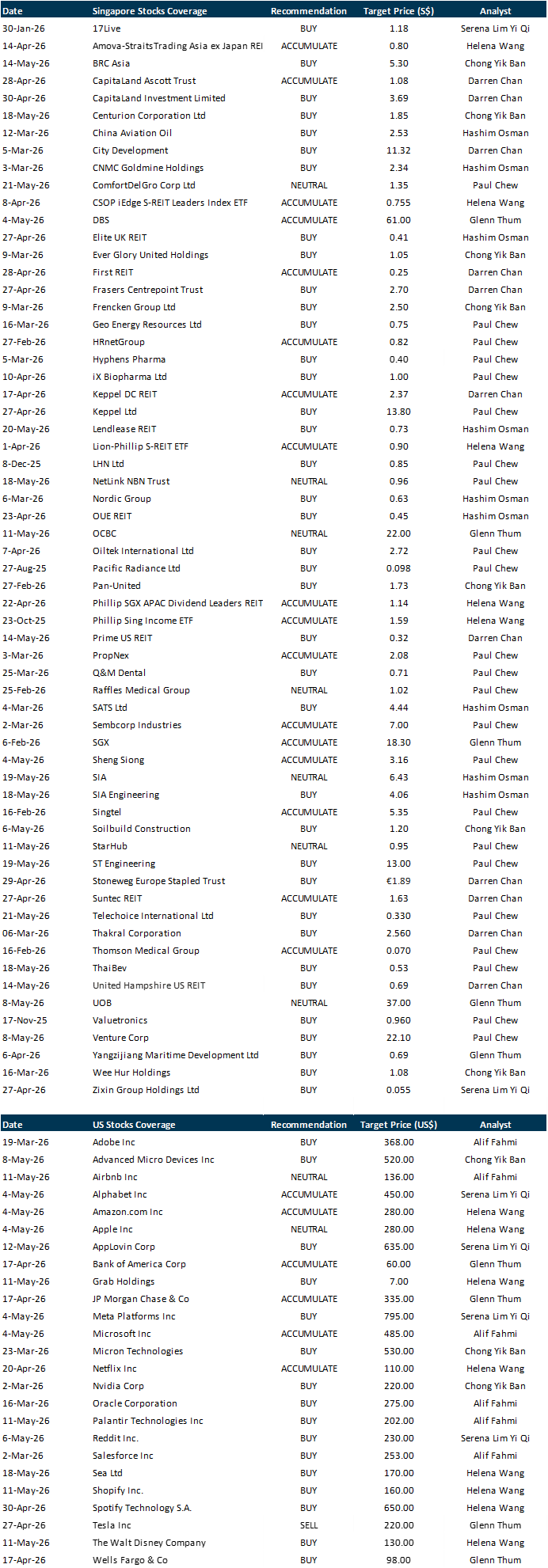

RESEARCH REPORTS

Geo Energy Resources Ltd – Still on track

Recommendation: BUY; TP S$0.75; Last close: S$0.4700; Analyst Paul Chew

- 1Q26 results were below expectations. Revenue/PAT were 17%/7% of our FY26e forecast. 1Q26 production declined 36% YoY to 2.0mn MT, caused by a 1.2mn MT decline at the TBR mine. As TBR approaches the end of its mine life, production will shift to the larger TRA mine, which has the new infrastructure. Production target for FY26e of 11.5-12.5mn MT is unchanged (FY25: 12.5mn MT).

- The new 92km US$190mn integrated infrastructure (hauling road and jetty) is 90% complete and undergoing truck testing. Geo will utilise the infrastructure in July by transferring coal haulage from an existing road that charges US$7-8 per MT. On 11 May, Resource Invest signed a term sheet for a substantial investment in infrastructure (i.e., MBJ) of US$1.5bn. The investments will be made in 3Q26 and 1Q27.

- We maintain our FY26e earnings as we expect production to ramp up in 2H26 with the new infrastructure. Coal prices are also trending 30-40% higher YoY in 2Q26. Our BUY recommendation and DCF target price of S$0.75 are unchanged. The sector has been under pressure since the Indonesian Government’s proposed centralisation of commodity export controls. There are no details on implementation, but centralisation or supervision could lead to incremental fees and tighter currency controls. The trifecta boost in earnings from the higher coal prices, jump in coal production, and infrastructure income is on track.

Valuetronics Holdings Ltd- Returning more capital, but earnings sluggish

Recommendation: BUY; TP S$1.29; Last close: S$1.1700; Analyst Paul Chew

- FY26 results were below expectations. Revenue/adj. PATMI was 93%/91% of our FY26 forecasts, respectively. Adj. PATMI declined 16% YoY to HKD67mn. Effective tax in 2H26 more than tripled to around 15% due to full utilisation of tax losses in Hong Kong and the partial end of tax incentives in Vietnam. The company intends to return HKD300mn (S$49mn) in FY27/28 via special dividends and share buybacks. The ordinary dividend payout ratio is also raised from up to 50% to between 50% and 70%.

- The company made a HKD45mn provision on its GPUs and related hardware. There is a better demand for GPU-as-a-Service using US hardware in Hong Kong. We expect the company to dispose of the remaining ~HKD130mn GPUs. Trio Ai is no longer reported as an associate due to cumulative losses.

- We lowered our FY27e earnings by 12% to HK$163mn to account for higher effective tax. The target price is raised to S$1.29 (prev. S$0.96), or 20x PE FY27e (prev. 13x PE), in line with the re-rating of industry valuations. Our ACCUMULATE recommendation is maintained. There will be two major drags on earnings for FY27e. The phasing out of legacy consumer electronic products and higher effective tax (esp. 1H27) will contract earnings. The dividend yield of 5.4% is supported by the special dividend of at least HKD0.16 (~2.6 cents). The company also intends to buy back shares in FY27 of not less than HKD80mn (~S$13mn).

Market Journal articles powered by PhillipGPT

Elite UK REIT Shows Strong Capital Management and Portfolio Growth, BUY Rating with S$0.41 Target

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Yoma Strategic Holdings Ltd [NEW]

Date & Time: 3 June 26 | 12PM-1PM

Register: poems-20260603-148171

Corporate Insights by AvePoint [NEW]

Date & Time: 3 June 26 | 7PM-8PM

Register: poems-20260603-149098

Corporate Insights by First REIT

Date & Time: 11 June 26 | 12PM-1PM

Register: poems-20260611-146839

Corporate Insights by AIMS APAC REIT

Date & Time: 17 June 26 | 12.30PM-1.30PM

Register: poems-20260528-145702

POEMS Podcast:

Research Videos

Weekly Market Outlook: NVDA, SIA, Micron, ST Engineering, Singtel & More!

Date: 25 May 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials