DAILY MORNING NOTE | 20 September 2022

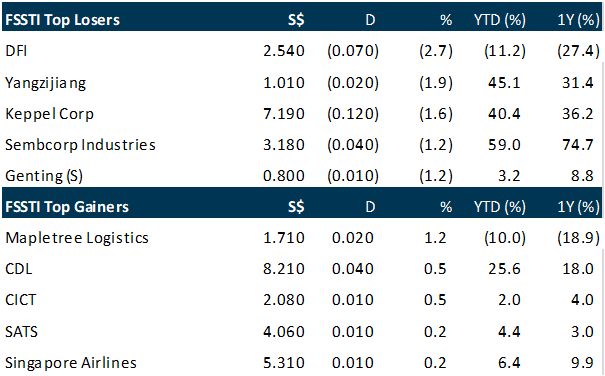

Stock markets in Asia extended last week’s rout on Monday (Sep 19), as investors remain cautious over concerns of another outsized rate hike by the United States Federal Reserve this week. Key bourses in Asia closed in the red. Singapore’s benchmark Straits Times Index (STI) fell 0.4 per cent, or 11.98 points, to 3,256.31. Losers outnumbered gainers 295 to 188, as some 1.02 billion securities worth S$811 million exchanged hands. Japan’s Nikkei 225 dropped 1.1 per cent, while Hong Kong’s Hang Seng Index declined 1 per cent. It is not just the Fed rate hike of the expected 75 basis points that the market is watching. Charu Chanana, market strategist at Saxo Capital Markets, said that the Bank of England is expected to follow with a 0.5 per cent rise the day after, while the Bank of Japan will also meet on Thursday. Several STI constituents declined by more than 1 per cent on Monday. The day’s top decliner was DFI retail group, which fell 2.7%, or US$0.07 to US$2.54. Yangzijiang Shipbuilding is the second-highest decliner, dropping 1.9 per cent, or $0.02 to S$1.01. Mapletree Logistics Trust was among the few counters to buck the trend, rising 1.2 per cent, or S$0.02 to S$1.71, emerging as the day’s best performer.

Major U.S. stock indexes inched up Monday and bond yields hit their highest level in more than a decade as investors looked ahead to the Federal Reserve’s interest-rate decision later this week. The S&P 500 rose 26.56 points, or 0.7%, to 3899.89. The broad market index opened with losses but rallied in the last hour of trading, putting it firmly into positive territory. The Dow Jones Industrial Average advanced 197.26 points, or 0.6%, to 31019.68. The technology-focused Nasdaq Composite climbed 86.62 points, or 0.8%, to 11535.02. This week, investors are largely focused on a round of interest-rate decisions by central banks. The Fed’s decision, to be announced Wednesday, will be followed Thursday by the Bank of England. Investors sold government bonds in the run-up to the Fed meeting, sending yields to their highest level in years. The yield on the 10-year U.S. Treasury note rose to 3.489%, its highest 3 p.m. ET settlement level since 2011, and up from 3.447% on Friday. The two-year yield, which is much more sensitive to near-term interest rate expectations, climbed to 3.946%, its highest settle since 2007, up from 3.859% on Friday. Yields and bond prices move in opposite directions.

Top gainers & losers

SG

Real estate developer Yanlord Land Group on Monday (Sep 19) said an indirect subsidiary, together with two other parties, has been awarded a residential site tender at Lentor Central in Singapore at a bid price of S$481 million, or S$1,108 per square foot per plot ratio (psf ppr). UED Alpha, a wholly-owned subsidiary of Yanlord’s United Engineers Limited, submitted the tender with Forsea Residence and Soilbuild Group Holdings. The parties plan to build a residential development of about 470 units on the 144,714 square feet (sq ft) site, located within the new Lentor Hills estate. The site has a maximum permissible gross floor area of about 434,140 sq ft. The second highest bid of nearly S$1,069 psf ppr was from CapitaLand Development’s Tanglin Land. GuocoLand teamed up with Intrepid Investments to place the lowest bid of nearly S$1,038 psf ppr. Shares in Yanlord ended flat on Monday at S$1.04.

Singapore’s Employment Claims Tribunal (ECT) has ordered payment services company OxPay Financial to pay its former chief executive and chief financial officer S$77,501.52 following wrongful dismissal claims by the 2 individuals, according to copies of the orders seen by The Business Times. Former executive director and chief executive Anthony Koh resigned from MC Payment, as Oxpay was known at the time, on Jul 1, 2021, according to filings on the Singapore Exchange. A day later, CFO Madeline Sam also resigned. Their departures came after Oxpay controlling shareholder Ching Chiat Kwong succeeded in his bid to replace the directors of the company’s board. At the time, MC Payment said that both individuals would serve a required 6-month notice period. However, in a bourse filing on Dec 1, OxPay Financial announced the immediate termination of Koh and Sam, about 1 month before their notice periods were up. As part of ECT orders issued on Jul 28 that were seen by BT, OxPay Financial was ordered to pay Koh S$20,000 as part of the wrongful dismissal dispute, S$20,000 for the pay he was owed for the month that he was terminated early as well as costs of S$400. OxPay SG, a subsidiary of the company, was also ordered to pay Sam S$16,800 as part of the wrongful dismissal dispute, S$19,901.52 for the pay she was owed for the month she was terminated early, the paid annual leave she was owed as well as costs of S$400. In response to queries by BT, OxPay Financial said that it had sought leave to appeal against the ECT’s decision. That leave for appeal has however been rejected by the Singapore District Court. Oxpay said that it and its subsidiary do not intend to pursue any further legal action, and that it intends to “move forward and focus on growing their businesses”. Shares of OxPay closed up S$0.005, or 3.7 per cent at S$0.141 on Monday (Sep 19).

Singapore’s dollar has established itself as Asia’s most resilient currency against the US dollar this year, and some strategists are betting on more strength if price pressures force the nation’s central bank to tighten its exchange-rate policy again next month. Goldman Sachs Group, Citigroup and MUFG Bank are among banks that are bullish on the currency, underpinned by an expectation that the Monetary Authority of Singapore (MAS) will extend policy tightening at its October meeting to help rein in core inflation that hit a 14-year high in July. The predictions come as almost every major currency retreats against the dollar with the US Federal Reserve set on an aggressive rate hike cycle. While the MAS’ stance has turned the nation’s currency into a winner against peers in Asia, it’s still down more than 4 per cent against the greenback this year. MUFG Bank puts the likelihood of additional tightening by the MAS next month at 50 per cent, which could translate into a gain of more than 1 per cent for the local currency versus the dollar over the following months. MUFG forecasts the Singdollar rising to 1.38 against the dollar by year-end. It closed last week at 1.4070. Still, even if the MAS does extend its policy tightening for a fourth time this year, there’s no guarantee the local currency will rally against the greenback – the Singapore dollar slumped to its lowest level in more than 2 years earlier this month before paring its 2022 decline to 4.1 per cent by the end of last week. The risk for Singapore dollar bulls is that the MAS decides to keep its policy unchanged next month, which can’t be completely ruled out – the central bank maintained its 2022 inflation projections in August, indicating the existing policy stance may be sufficient to tame inflation. The next test comes on Friday with the release of core CPI for August, which is forecast to increase 5 per cent from a year earlier. The currency could come under pressure if the data disappoint and expectations for further MAS tightening diminish.

US

Ford Motors on Monday warned investors that the company expects to incur an extra $1 billion in costs during the third quarter due to inflation and supply chain issues. Ford said supply problems have resulted in parts shortages affecting roughly 40,000 to 45,000 vehicles, primarily high-margin trucks and SUVs that haven’t been able to reach dealers. The company expects to complete and deliver the vehicles to dealers in the fourth quarter and is still projecting 2022 adjusted earnings before interest and taxes of between $11.5 billion to $12.5 billion. Shares of the company fell about 5% in extended trading following the update. Ford cited recent negotiations resulting in inflation-related supplier costs that will run about $1 billion higher than originally expected. The automaker anticipates third-quarter adjusted earnings before interest and taxes to be in the range of $1.4 billion to $1.7 billion. Ford added that executives will “provide more dimension about expectations for full-year performance” when it reports its third-quarter results on Oct. 26. Ford’s largest crosstown rival, General Motors, announced similar issues earlier this year. GM on July 1 warned investors that supply chain issues would dent its second-quarter earnings, noting it had about 95,000 vehicles in its inventory that were manufactured but lacked some components.

Instacart Inc. doesn’t plan to raise much capital in its initial public offering and instead plans to have most of the listing come from the sale of employees’ shares, said people familiar with its thinking. In meetings with prospective investors in recent weeks, Instacart executives said they didn’t plan to issue many new shares in their IPO, the people said. The sale of mostly employee shares would allow Instacart’s staff, including some of its earliest hires, to at last cash out of some of the shares they have been accumulating. The move could help Instacart, which was founded in 2012, retain talent by allowing employees more ways to benefit from their shares. Listed shares could also make Instacart more attractive to new employees than startups that have decided to wait for a better market to list. The IPO market is headed for its worst year in decades, leaving some startups with few options but to spend through their cash reserves while they wait for the stock market to calm. Instacart turned a net profit in the second quarter, which could explain why it is focusing its public listing on the sale of employee shares. While Instacart will sell a small percentage of new shares, the bulk of its offering will come from employee shares that will be sold directly to new investors at an agreed-upon price ahead of a stock-market debut. Details of the listing could change depending on market conditions and other factors. Instacart had previously leaned toward going public through a direct listing, The Wall Street Journal previously reported. In a direct listing, a company’s shares simply start trading on an exchange on a set day. There is a reference price for where trading could start, but no shares are sold in advance at that price. Existing shareholders can sell their shares, but companies don’t raise any cash by going public. Instacart said earlier this year that it had more than $1 billion in cash and marketable securities and last raised money in March 2021.

The US dollar held firm near 2-decade highs against other major currencies on Monday (Sep 19), biding its time ahead of a slew of central bank meetings that include 1 by the US Federal Reserve (Fed) that is likely to deliver another hefty rate hike. Trade was generally subdued, with markets in London and Tokyo closed for public holidays. Still, world stock markets remained on edge and the US dollar maintained its firm tone, given expectations that the Fed would maintain its aggressive rate-hike path to contain uncomfortably high inflation. The US dollar index, which measures the currency against 6 counterparts, was up 0.4 per cent at 110.06, heading back towards a 20-year high of 110.79 hit on Sep 7. This week is also smattered with holidays that could thin liquidity and result in sharper price moves, with Japan and Britain off on Monday, Australia on Thursday, and Japan again on Friday, among others. The euro was 0.25 per cent lower at US$0.9993, sterling was 0.4 per cent weaker at US$1.1378 and within sight of Friday’s 37-year lows, while the New Zealand and Australian dollars slipped more than 0.5 per cent each. Canada’s dollar fell to its lowest in almost 2 years at 1.3324 per US dollar. The US dollar was around 0.4 per cent firmer at 143.46 yen, hovering beneath a strong resistance level at 145 that has been reinforced by Japanese policymakers’ toughened talk of currency intervention.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, PSR

RESEARCH REPORTS

Upcoming Webinars

Guest Presentation by Emperador Inc. [NEW]

Date: 20 September 2022

Time: 12pm – 1pm

Register: https://bit.ly/3x4jh9I

Guest Presentation by ComfortDelGro Corporation Limited [NEW]

Date: 29 September 2022

Time: 12pm – 1pm

Register: https://bit.ly/3Ql57J7

Guest Presentation by MeGroup Ltd [NEW]

Date: 5 October 2022

Time: 12pm – 1pm

Register: https://bit.ly/3RSOTXY

Guest Presentation by RE&S Enterprises Pte Ltd [NEW]

Date: 21 October 2022

Time: 2pm – 3pm

Register: https://bit.ly/3REOBnY

POEMS Podcast:

Research Videos

Weekly Market Outlook: Prime US REIT, Frasers Centrepoint Trust, Sembcorp Industries, SG Weekly…..

Date: 19 September 2022

Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Phillip Research in 3 minutes: #29 Keppel Corporation; Initiation

Click here for more on Phillip in 3 mins.

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials