DAILY MORNING NOTE | 23 March 2026

Recent Podcasts:

Wee Hur Holdings Ltd – Construction and worker dorm anchor growth

Advanced Micro Devices Inc. – Clear Instinct GPU roadmap, strong CPU demand

Netflix Inc. – Content, ads, and scale drive the next leg of growth

Week 13 equity strategy – There is a pathway to a US$200 crude oil price. The risk of a ground offensive in Iran is rising. Whilst President Trump said he is considering winding down military operations in Iran, in just a week, he has sent two deployments of Marines totalling 4000-5000 to the Middle East. Ground troops could be sent to capture Kharg Island oil facilities or the Iranian coastline to secure the Straits of Hormuz. The US is still climbing up the escalation ladder of this war. Capturing critical Iranian oil infrastructure or US troops on Iranian soil may lead to more aggressive retaliation on the region’s oil infrastructure. As the US exposes its troops to attack and gets further drawn into the war, it becomes similar to the US first sending Marines into Vietnam to defend the Da Nang air base in 1965. The final escalation will be tit-for-tat destruction of civilian infrastructure across the Gulf.

The last Middle East conflict that saw a major spike in oil prices was the Kuwait war (2Aug90). Crude oil price jumped from an average of US$15 (Jun90) to US$42 peak (Oct90), or a 275% rise. Assuming a similar rise of Brent oil average of US$68 (Jan26), it implies a $187 peak. The impact could be worse on paper. Kuwait and Iraq were 7% of the global oil supply that was embargoed. The current estimated impact is 10% loss. The Kuwait war had the threat that Iraq could also invade Saudi Arabia. This is no different from Iran destroying much of the Gulf oil infrastructure. The secondary effects on the global economy are worse. We have already seen several force majeure events by petrochemical companies in Singapore, such as Aster Chemicals, PCS and TPC. Industries impacted include plastic packaging, automotive, tyres, detergents, construction, electronics, medical consumables, appliances, etc. The situation is worse than the pandemic, where the bottleneck was shipping. Currently, there is no supply. Inflationary pressure will keep interest rates elevated and positive for banks and SGX. Admittedly, Singapore short term rates such as 3M SORA have been falling since the conflict began.

Paul Chew

Head Of Research

Paulchewkl@phillip.com.sg

Singapore stocks ended lower on Friday (Mar 20), as the Iranian conflict continued for a third week and oil markets remained under pressure. The local benchmark fell 0.4 per cent or 18.74 points to 4,948.87. The iEdge Singapore Next 50 Index declined 0.9 per cent or 12.88 points to 1,464.78.

US stocks tumbled in volatile trading Friday as the U.S.-Israel conflict with Iran showed no sign of abating and oil prices continued their ascent. The Dow Jones Industrial average shed 443.96 points, or 0.96%, ending at 45,577.47. The S&P 500 fell 1.51% and closed at 6,506.48, while the Nasdaq Composite lost 2.01% and settled at 21,647.61. The small-cap Russell 2000 declined more than 2% and slipped into correction territory.

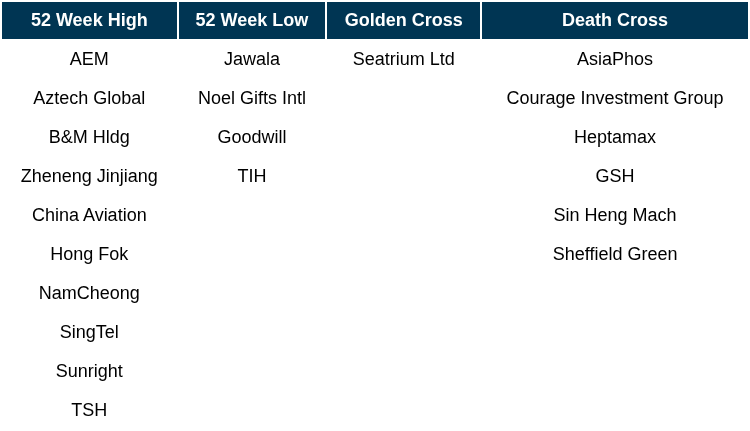

Singapore Technical Highlights

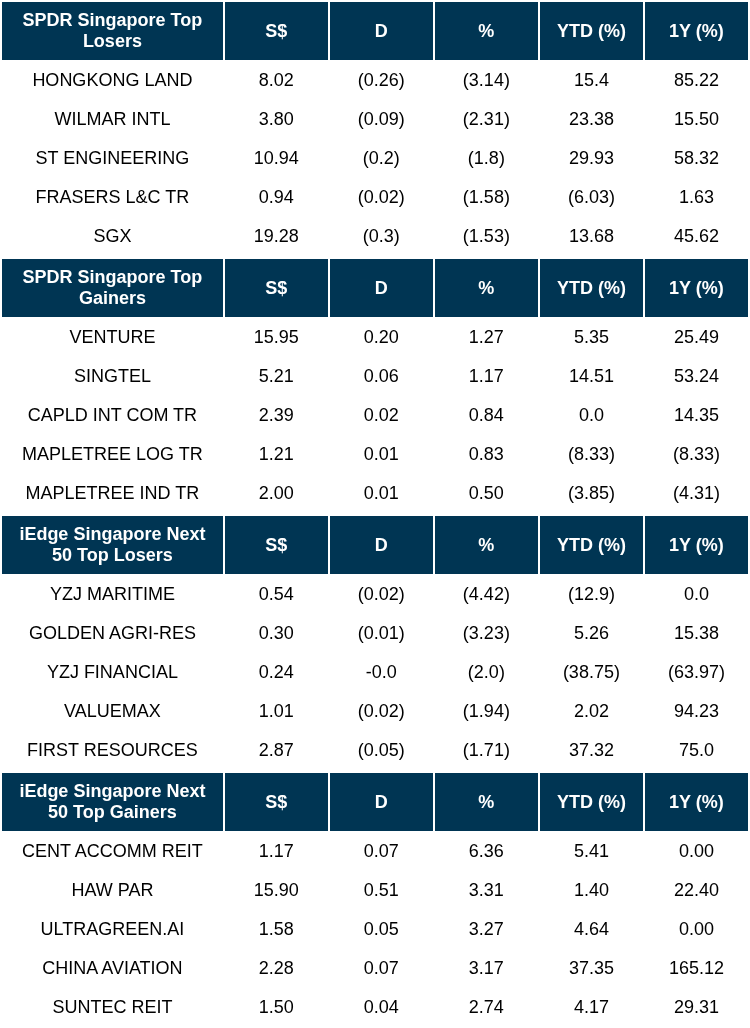

TOP 5 GAINERS & LOSERS

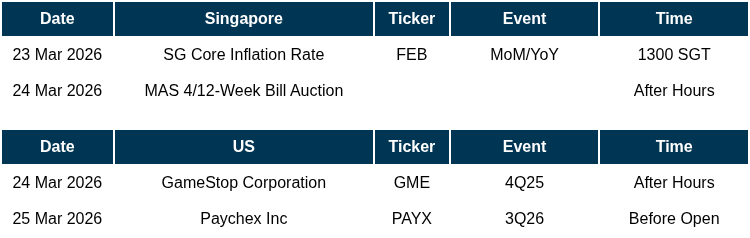

Events Of The Week

SG

Semiconductor equipment maker AEM has partnered ASE Technology, one of the world’s largest semiconductor testing and packaging companies, to develop disruptive test solutions for artificial intelligence (AI) and high-performance computing (HPC) markets.

Singapore Airlines on Friday (Mar 20) extended the cancellation of its flights between the city-state and Dubai to the end of April, citing escalating geopolitical tensions in the Middle East. Despite the pullback in the Middle East, the airline said it is shifting aircraft capacity to capture rising travel demand for its London and Melbourne routes for the northern summer season.

OCBC is unable to claim US$56 million from a group of insurers for a vessel that it offered mortgage after the Court of Appeal allowed the five insurers’ appeal. The Court of Appeal, in overturning the lower court’s judgement, pointed out that OCBC had not proved the rig was lost by peril of the seas as it did not offer a cause of seawater entering the vessel by chance. The bank had not shown as well that the vessel sank in wholly unexplained circumstances.

Singtel’s outage on Monday (Mar 16) affected about 600,000 customers and was due to a mechanical fault at one of its network facilities. Separately, about 2,000 customers experienced mobile connectivity problems on Mar 17 because of a software bug from a planned IT system upgrade.

Catalist-listed HGH Holdings has agreed to sell its 200,000 shares or a 20% stake in its wholly-owned subsidiary, Premium Concrete, for $2.4 million. The company had entered into a share purchase agreement (SPA) with Lim Kui Teng, founder of private construction company, Chuan Lim Construction.

ISE Foods Holdings (IFH), a subsidiary of SGX-listed Ellipsiz, has received a $65 million loan from Maybank to help fund the development of Singapore’s fourth egg farm. Ellipsiz’s plans for this egg farm extend as far back as 2021 and has received the support of the Singapore Food Agency. Presumably, the higher production eggs here can help with food security.

US

Unilever is in talks to separate its food business and combine it with spice maker McCormick in an all-stock deal. The major strategy shift by Unilever would continue a trend of consumer conglomerates streamlining their businesses and would leave U.K.-based Unilever focused on beauty, personal-care and home products.

Eight states filed a motion for a temporary restraining order to stop the $6.2 billion Nexstar Media and Tegna merger, which closed Thursday. The states argue the merger would result in too much concentration in local TV markets and cause irreparable harm to the public interest. The emergency motion seeks to prevent Nexstar from integrating or commingling the assets and operations acquired from Tegna.

FedEx raised its full-year revenue growth forecast to 6% to 6.5% and adjusted earnings per share outlook to $19.30 to $20.10. FedEx reported a fiscal third-quarter profit of $1.06 billion, with revenue rising 8% to $24.0 billion. The company reduced its capital spending outlook to $4.1 billion and confirmed its Freight segment spinoff is on track for June 1.

Prestige Consumer Healthcare has signed a deal to buy a portfolio of brands that includes the Breathe Right nasal strip from privately held Foundation Consumer Healthcare for $1.045 billion. Prestige on Friday said the portfolio, which also includes the Dimetapp cough and cold relief brand, generated about $200 million in revenue in 2025.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Micron Technology, Inc – Extended agreements signal structural demand growth

Recommendation: BUY; TP US$530; Last close: US$422.90; Analyst: Yik Ban Chong (Ben)

- 2Q26 revenue was within our expectations, 1H26 revenue at 50% of our FY26 forecast. 2Q26 adj. PATMI exceeded our expectations, 1H26 PATMI at 58% of our FY26 forecast. 2Q26 adj. PATMI spiked 686% YoY to a record US$14bn, driven by bit shipment growth (est. +35% YoY) and a spike in DRAM/NAND ASPs (est. +107%, 118% YoY respectively).

- Micron entered its first five-year strategic customer agreement (SCA) with an undisclosed ‘large’ customer. Specific terms of the agreement are not disclosed. Previous long-term agreements (LTA) usually last only a year. We believe high-end chipmakers and hyperscalers view memory as strategically critical in the AI race, as longer-term contracts are being signed across the industry.

- We maintain BUY with a higher TP of US$530 (prev. US$500). We raised our FY26e revenue/PATMI by 43%/100%. Ongoing industry shortage in memory chips is expected to push DRAM/NAND ASPs higher. We expect industry supply to increase meaningfully starting from CY2H27e, as SK Hynix aims to maintain 2026 capex-to-sales ratio at about mid-30% level (2025 industry: ~31%). We lower our PE multiple to 9x FY26e PE (prev. 16.8x), a 43% discount to comparables’ forward PE of 15.7x, due to higher risks from the Middle East conflict. The closure of the Straits of Hormuz threatens 30% of global supply of helium, a critical component in semiconductor wafer manufacturing. We believe Micron is better insulated from the conflict than its Korean competitors due to its stronger presence in the US, which accounts for about 45% of global helium production (Qatar: ~30%).

Singapore REITs Monthly – Interest cost savings intact

Recommendation: Overweight (Maintained); Analyst: Darren Chan

- The S-REITs Index fell 1.9% in February 2026, reversing the 0.7% gain in January 2026. Stoneweg Europe Stapled Trust (SERT SP, BUY, TP €1.89) was the top performer for the month, rising 6.9% on strong FY25 results. Prime US REIT (Prime SP, BUY, TP US$0.32) was the worst performer, falling 12.9% after rising 14.2% the month before, as investors weighed a slower-than-expected recovery in portfolio occupancy. Among the sub-sectors, Singapore retail led gains, rising 0.8%, while overseas commercial was the weakest, declining 8%, dragged by the US office S-REITs.

- Despite inflation concerns from heightened geopolitical tensions in the Middle East and expectations that the Fed will maintain higher-for-longer rates, we see potential for stronger DPU growth in FY26 from interest cost savings as benchmark SORA rates continue to decline. Valuations remain undemanding, with the sector trading at a forward dividend yield spread of c.3.8% (mean) and a P/NAV of 0.97x (-0.4 s.d.). UI Boustead REIT (UIBREIT SP, non-rated) began trading on SGX on 12 March at an IPO price of S$0.88, debuting to a lukewarm reception.

- We reiterate our OVERWEIGHT recommendation on S-REITs, as their stable performance and defensive positioning reaffirm their safe-haven status for global investors amid market volatility and uncertainty from heightened geopolitical tensions. Within sub-sectors, we prefer retail, where rental reversions are expected to remain strong in the high single-digits in 2026. We also favour overseas S-REITs offering high yields of over 8% with resilient portfolios, such as Stoneweg Europe Stapled Trust (SERT SP, BUY, TP €1.89), Elite UK REIT (ELITE SP, BUY, TP: £0.41), and United Hampshire US REIT (UHU SP, BUY, TP US$0.69). In addition, we like Prime US REIT (PRIME SP, BUY, TP US$0.32), for its cheap valuation (0.37 P/NAV) and improving portfolio occupancy.

Market Journal articles powered by PhillipGPT

SIA Engineering Posts Strong Q3 Results on Associate Earnings Growth

Raffles Medical Group Faces Sluggish Growth on Mixed Results

Grab Holdings Achieves First Full Year of Net Profit with Strong Revenue Growth

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by LHN Ltd

Date & Time: 25 March 26 | 12PM-1PM

Register: poems-20260325-140477

Corporate Insights by Lum Chang Creations Limited

Date & Time: 27 March 26 | 12PM-1PM

Register: poems-20260327-141688

Corporate Insights by Thakral Corporation Ltd

Date & Time: 31 March 26 | 12PM-1PM

Register: poems-20260331-141690

Corporate Insights by Thakral Corporation Ltd

Date & Time: 31 March 26 | 6.30PM-7.30PM

Register: poems-20260331-141692

Corporate Insights by Beng Kuang Marine

Date & Time: 2 April 26 | 12PM-1PM

Register: poems-20260402-142364

Strategy & Stock Picks (Investment Symposium 2026) – SG Market [NEW]

Date & Time: 11 April 26 | 2.30PM-6PM

Register: poems-20260411-142749

POEMS Podcast:

Research Videos

https://www.youtube.com/embed/v72GfRG-rG8?list=PLv41YzcbRaXG98t4efd7aXkAfH33gq-2u

Date: 16 March 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials