DAILY MORNING NOTE | 25 May 2026

Recent Podcasts:

Sea Ltd.-2026 an investment year

Airbnb Inc – Modest booking and ADR growth

Wee Hur Holdings Ltd – Construction and worker dorm anchor growth

Week 23 equity strategy: The Space Exploration Technologies Corp (SpaceX/SPCX) S1 prospectus has been lodged. It plans to raise US$75bn-80bn with a market cap of US$1.75tr. It suffered a net loss of US$5bn in FY25, which ballooned to US$4.3bn net loss in 1Q26. The 1Q26 loss comes largely from the xAI (or Grok) business of around US$2.5bn operating loss, while Starlink connectivity is US$1.1bn in operating profit. The rocket launch space segment lost US$660mn.

So what is the dream? The addressable market opportunity is US$28.5tr (US$26.5tr AI, US$1.6tr connectivity, US$370bn space). Firstly, the next-generation Starship V3 rocket cargo load jumps to 100MT from the current Falcon 9 18MT. Secondly, push Grok toward AGI and create limitless duplicates of human-like intelligence. Terafab will help drive 1 terawatt of compute hardware per year. Thirdly, orbital AI computing at scale from 2028 using solar power and lasers to link servers. Finally, the mission is to build a base on the Moon and Mars for energy production, manufacturing and passenger plus cargo transport. In terms of cash burn, FCF in 1Q26 was a negative US$9bn. SpaceX generates positive U$1bn operating cash flow. But Capex was a huge S$10bn in 1Q26 due to almost $8bn for AI.

Space X has become a major competitor for several tech companies. It apparently builds data centres faster than other hyperscalers, with already a US$15bn p.a. deal with Anthropic. It also now competes with TSMC by working with Intel and Tesla by building Terafab. With scale and computing power, Grok becomes more competitive against other LLMs. We think the big beneficiary is semiconductor equipment makers, that is, essentially monopolies which SpaceX is buying and not competing.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore stocks ended higher on Friday, even as investors stayed cautious amid ongoing US-Iran peace talks aimed at ending the conflict in the Middle East. The benchmark gained 0.4% or 22.44 points to finish at 5,068.15. Keppel led the gainers on Singapore’s blue-chip index, rising 4.7% to S$10.91. The worst performer among constituents was Singtel, which fell 2.3% to S$4.59.

US stocks rose on Friday, with the Dow reaching a record closing high, as investors cheered signs of progress in talks to end the Middle East conflict and a strong corporate earnings season. The S&P 500 notched its eighth consecutive weekly gain, rose 27.75 points, or 0.37%, to 7,473.47. Semiconductor stocks, which have driven recent Wall Street gains, were mostly higher.

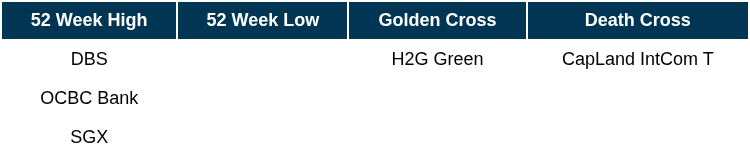

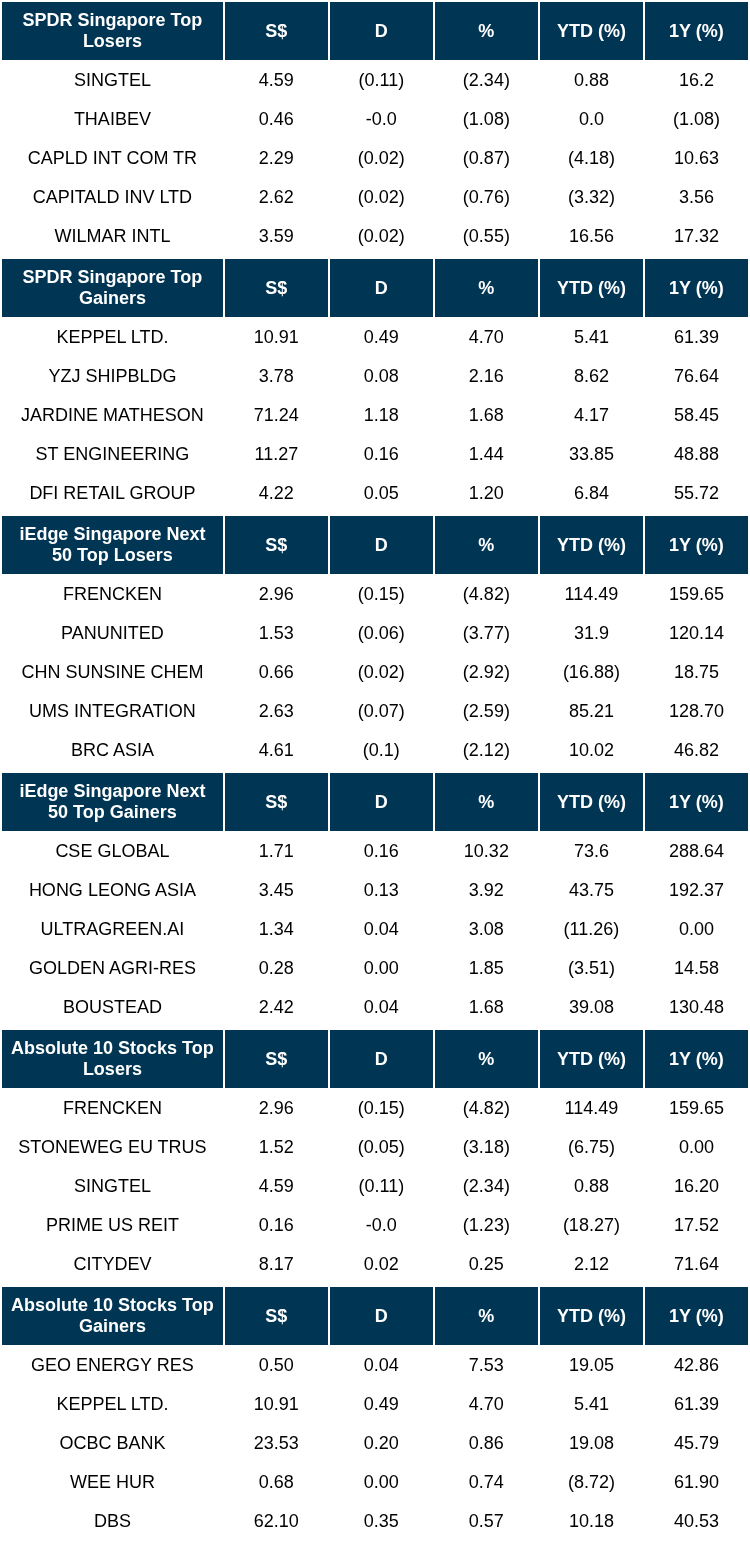

Singapore Technical Highlights

TOP 5 GAINERS & LOSERS

EVENTS OF THE WEEK

SG

Addvalue Technologies has reported earnings of US$4.8 million for FY2026 ended March 31, 147.5% higher YoY. Revenue was up 59.9% y-o-y to US$24.8 million in FY2026.

Metro Holdings recorded a loss after tax of $203.1 million for FY2026 ended Mar 31, compared to a loss after tax of S$224.7 million for the corresponding period a year ago. Revenue for FY2026 fell 6.6% to $97.7mn.

Hour Glass has reported earnings of $179.5 million for the FY2026 ended March 31, up 32% y-o-y. Earnings per share was up 33% to 22.79 cents in the same period. Revenue rose 15% YoY to $1.34bn.

UI Boustead REIT announced that it has entered into various agreements to coinvest in the development of a build-to-suit aerospace facility worth $104mn at the Seletar Aerospace Park in Singapore. It’s expected to be fully leased on a long-term lease of 22.5 years with in-built rental escalations.

Aims Apac Real Estate Investment Trust is zooming in on data centre opportunities as it looks beyond traditional industrial assets for its next phase of growth, to tap rising demand for digital infrastructure. He pointed to two sites in New South Wales, Australia.

Tuas Ltd’s planned US$1.1 billion acquisition of Singapore major telecom operator M1 Ltd has collapsed days after regulators halted their review of the transaction. Tuas said the agreement was terminated after several conditions were not met by a May 21 deadline.

UBS Group AG accused the US lawyer overseeing a six-year-old inquiry into Credit Suisse’s handling of Nazi-linked accounts of bias and exceeding his mandate, deepening a standoff between the Swiss bank and its critics in Washington.

US

The Federal Open Market Committee on Friday unanimously selected Kevin Warsh as its chair. US President Donald Trump stressed that he wants Kevin Warsh to independently lead the Federal Reserve (Fed), as he looked to downplay investor concern that he would pressure the new central bank chief on policy decisions.

The Trump administration continues to weigh US tariffs on imported semiconductors to boost domestic chip manufacturing, though there are no immediate plans to impose any new levies, US Trade Representative Jamieson Greer said.

Anthropic PBC is set to close its latest round of funding, which may top US$30 billion ($38.4 billion) at a valuation above US$900 billion, as soon as next week, vaulting ahead of rival OpenAI to become the world’s most valuable artificial intelligence (AI) start-up.

Space-themed ETFs are blasting off, with asset managers rushing to issue new products ahead of the much-anticipated initial public offering by industry giant SpaceX. Space-related ETFs have attracted US$1.3 billion in new cash in the last month.

Nvidia Corp chief executive officer Jensen Huang urged Super Micro Computer Inc to tighten up on compliance after Taiwan detained three people this week for allegedly making fraudulent declarations about artificial intelligence (AI) servers made by its US partner.

US consumer sentiment fell in May to a record low and long-term inflation expectations worsened notably due to the Iran war. The University of Michigan’s final May sentiment index decreased five points to 44.8 from April, weaker than all projections in a Bloomberg survey of 48.2.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

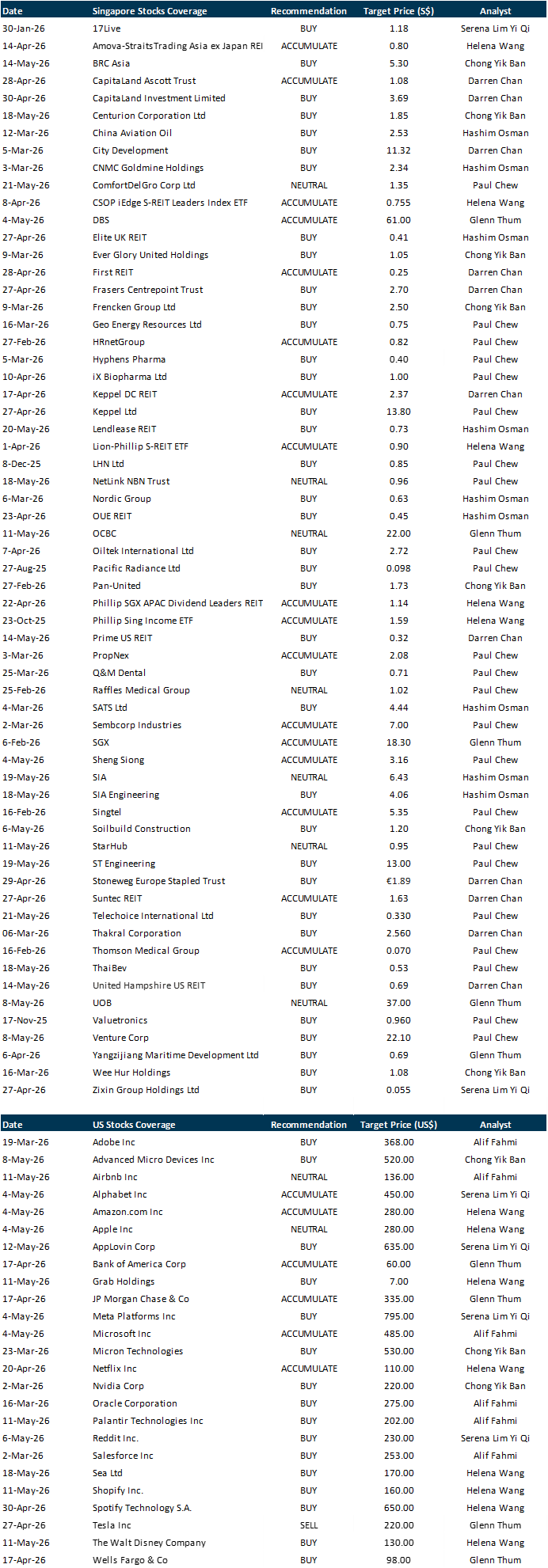

RESEARCH REPORTS

City Developments Limited – Strong start to the year

Recommendation: BUY; TP S$11.32; Last close: S$8.17; Analyst Darren Chan

- No financial information was provided in this operational update. The ultra-luxury freehold Newport Residences, launched in January 2026, is 78% sold to date (57% sold on launch weekend), while other projects, including The Orie, The Myst, Zyon Grand, and Norwood Grand, continue to see strong sales momentum.

- Hotel operations remained strong despite geopolitical tensions, with RevPAR increasing 4.3% YoY to S$144.8. Separately, all 27 strata units previously held by the Group at Fortune Centre in Singapore have been fully sold.

- Maintain BUY with an unchanged RNAV target price of S$11.32, representing a 25% discount to our RNAV of S$15.09. We expect strong residential sales from the Group’s upcoming Singapore launches (1,302 units), supported by resilient demand. We also expect further asset divestments, including a potential exit from its legacy UK portfolio, as part of ongoing portfolio optimisation. An outcome of the strategic review is expected in the coming months and may include fund management initiatives to recycle non-core assets into private funds, thereby enhancing capital efficiency and unlocking embedded asset value.

Elite UK REIT – DWP’s operationally critical landlord

Recommendation: BUY; TP S$0.41; Last close: S$0.34; Analyst Hashim Osman

- We visited six of Elite UK REIT’s assets across London, Kent, and Cardiff that comprised 4 jobcentres (Broadway House Ealing, Peckham Job Centre, Oates House Stratford, Nutwood House Canterbury), one asset leased to Secretary of State for Communities & Local Government (Priory Court Dover), and another vacant asset that is currently being repositioned into a purpose-built student accommodation (Cambria House Cardiff).

- Elite UK REIT’s 148-property portfolio is valued at £463.2mn as of Feb26 valuation, following a 9.1% uplift driven by new CPI-linked DWP lease agreements (floored at 1%, capped at 5% per annum). This has reduced FY28 lease expiry concentration from 95.7% to 32%, and extended WALE from 2.4 years to 7.2 years.

- We maintain BUY with unchanged DDM-based TP of S$0.41. Elite is trading at a 9.0% FY26e dividend yield and a P/NAV of 0.86x. It trades in both GBP (Ticker: MXNU) and SGD (Ticker: MENU). Our site visit across London, Kent, and Cardiff confirmed our views on the following: i) the visited jobcentres are operationally critical to DWP’s daily service delivery, ii) financial support claimant volumes at the jobcentres are at record highs and rising, iii) select assets offer repositioning optionality.

NVIDIA Corporation – New growth drivers signalled

Recommendation: BUY; TP US$285; Last close: US$215; Analyst Yik Ban Chong (Ben)

- 1Q27 revenue/PATMI were within our expectations, at 24%/26% of our FY27e forecasts. Data centre revenue accelerated 92% YoY to US$75bn, the fastest growth in 4 quarters. This was driven by strong demand for Blackwell GB300 NVL 72 racks from hyperscalers and frontier AI model companies.

- NVIDIA broke down data centre revenue into two segments: 1) Hyperscale – includes the world’s largest consumer internet companies (AMZN, GOOG, META, MSFT, ORCL), and 2) AI Cloud, Industrial and Enterprise (ACIE) – including AI native clouds (eg. CRWV, NBIS), sovereign nations, and 250,000 Enterprise companies worldwide. We believe there would be acceleration in ACIE growth over the next 1-2 years, driven by Coreweave and Nebius’ aggressive capex expansion to support sovereign and smaller enterprises’ demand for cloud and AI workloads. NVIDIA guided 2Q27 revenue to accelerate 95% YoY.

- We maintain BUY with a higher target price of US$285 (prev. US$220). We raised our FY27e revenue/PATMI by 11%/17%, due to stronger growth expected from Anthropic as a new customer, and an additional US$20bn revenue visibility from Vera CPU. We increased our WACC assumptions to 7.9% (prev. 7.5%) to reflect lower visibility from the consolidation of gaming, automotive and professional visualisation segments.

SG Bonds – Week 22: yields moved higher WoW

Analyst Phillip Research Team

- UST yields edged higher WoW, and retraced from intra-week highs on Friday. The 30Y Treasury yield rose to 5.18% on Tuesday, extending last week’s move above 5% and marking its highest level since June 2007, before easing to close the week at 5.07%.

- SGS yields moved higher earlier in the week, following the rise in UST yields. The 2Y, 5Y and 10Y SGS yields climbed to 1.67%, 1.88% and 2.23%, respectively, with the 10Y yield reaching its highest level since April.

- Markets are now pricing a 28.1% probability of a Fed rate hike by December, with only a limited chance of tightening as early as June. Nevertheless, we think the policy outlook remains uncertain and will depend on guidance from new Fed Chair Kevin Warsh. Domestically, the Ministry of Trade and Industry will release the final 1Q26 GDP data on 25 May. Market consensus expects GDP growth to be revised higher to 5.2% YoY from the advance estimate of 4.6%, supported by stronger-than-expected manufacturing growth of 7.9% YoY, up from the preliminary estimate of 5.0%.

Singapore REITs Monthly – Global tensions are contained, with a limited impact so far

Recommendation: OVERWEIGHT; Analyst: Darren Chan

- The S-REITs Index rebounded 3.2% in April, after a 6.9% decline in March, as de-escalation in the Middle East supported a rotation into yield instruments. KORE US REIT (KORE SP, non-rated) was the best performer, rising 13%, driven by a strong 1Q26 operational update. First REIT (FIRT SP, non-rated) was the worst performer, falling 5.9% amid the divestment of its Indonesia portfolio. Retail was the best-performing sub-sector for the month, up 6.4%, while hospitality was the weakest, up 1.3%, as geopolitical tensions in the Middle East weighed on sentiment.

- 1Q26 results suggest that the direct impact of recent geopolitical tensions on the S-REIT sector has remained largely contained thus far, with most REITs continuing to report resilient operating metrics, stable portfolio occupancies, and healthy rental reversions.

- We reiterate our OVERWEIGHT stance on S-REITs, while remaining selective amid an increasingly uncertain macroeconomic backdrop. We continue to favour REITs with strong balance sheets, resilient earnings, and visible DPU growth potential. S-REITs attraction is a defensive yield play, given their relative safe-haven characteristics during periods of market volatility and geopolitical uncertainty. Within the sector, we prefer retail REITs, where healthy tenant sales and limited supply should continue to support high single-digit rental reversions in 2026. Our top picks are high-yielding names with resilient portfolios, including Stoneweg Europe Stapled Trust (SERT SP, BUY, TP: €1.89), Elite UK REIT (ELITE SP, BUY, TP: £0.41), and United Hampshire US REIT (UHU SP, BUY, TP: US$0.69). We also like Prime US REIT (PRIME SP, BUY, TP: US$0.32) for its attractive valuation at 0.34x P/NAV and relatively strong cash flow visibility.

Singapore Telecommunications Ltd – Middle East conflict speed bump

Recommendation: ACCUMULATE; TP S$5.20; Last close: S$4.59; Analyst Paul Chew

- FY26 results were within expectations. Revenue/EBITDA was 98% of our FY26e forecast. PATMI exceeded estimates at 107% of FY26e due to lower-than-modelled depreciation. Underlying PATMI grew 14% YoY to S$1.4bn in 2H26. The rise in inflation and energy costs is prompting Singtel to guide to more cautious low- to mid-single-digit FY27e EBIT guidance (FY26 +10%). FY26 dividends improved 9% to 18.5 cents.

- Contribution from associates was the largest driver of growth. Excluding Intouch, PAT jumped 19% to S$1bn in 2H26. Advanced Info earnings surged 42% to S$260mn, whilst Bharti increased 19% to S$434mn despite the 9.7% depreciation of the rupee.

- Our ACCUMULATE recommendation is maintained, but we lower our target price to S$5.20 on lower mark-to-market valuations of the associates. The Middle East conflict has increased energy costs, weakened currencies, slowed economic growth and tightened consumer spending in the countries Singtel operates. Singtel’s next leg of growth lies in its increased exposure to the massive build-out of digital infrastructure and the adoption of AI. The contribution from AI will climb through the acquisition of STT GDX, introduction of GPU-as-a-Service (RE: AI), hyperscaler demand for fibre connectivity and NCS AI solutions for enterprises. There is up to S$1bn of share buyback in FY27e.

Market Journal articles powered by PhillipGPT

Elite UK REIT Shows Strong Capital Management and Portfolio Growth, BUY Rating with S$0.41 Target

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Yoma Strategic Holdings Ltd [NEW]

Date & Time: 3 June 26 | 12PM-1PM

Register: poems-20260603-148171

Corporate Insights by First REIT

Date & Time: 11 June 26 | 12PM-1PM

Register: poems-20260611-146839/a>

Corporate Insights by AIMS APAC REIT

Date & Time: 17 June 26 | 12.30PM-1.30PM

Register: poems-20260528-145702

POEMS Podcast:

Research Videos

Weekly Market Outlook: Sea Ltd, ABNB, AppLovin, CDG, ThaiBev, SIA Engineering, Tech Analysis & More!

Date: 18 May 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials