DAILY MORNING NOTE | 3 June 2026

Recent Podcasts:

Sea Ltd.-2026 an investment year

Airbnb Inc – Modest booking and ADR growth

Wee Hur Holdings Ltd – Construction and worker dorm anchor growth

Trade of The Day

ETF Monthly: May 2026 – Singapore equities to outperform in June

Analyst: Zane Aw

- Review of asset classes performance in May – It was a mixed performance for the ETFs. The top gainer was the ETF tracking the S&P 500 (VOO), which surged 5.2%. On the other hand, the top loser was the ETF tracking Oil (XOP), which tumbled 7.9%.

- For their current trends, the S&P 500 and Singapore equities are in an uptrend. Meanwhile, US Treasury Bonds, Gold, Oil, and the Hang Seng Index are in a range consolidation. Bitcoin is in a downtrend.

- Heading into June, we expect the ETF tracking Singapore equities to extend its gains. The ETFs tracking the S&P 500, US Treasury Bonds, Gold, and the Hang Seng Index are expected to consolidate sideways. On the other hand, the ETFs tracking Oil and Bitcoin are likely to extend their weakness.

Singapore stocks ended higher on Tuesday (Jun 2). The Benchmark Index (STI) gained 1.2%, or 59.56 points to finish at 5,097.42. The STI gains, led by the local banks, follow recent announcements by DBS and OCBC of plans to boost their wealth offerings.

The S&P 500 and the Dow closed modestly higher on Tuesday (Jun 2) as risk appetite driven by artificial intelligence fervour was counterbalanced by tensions arising from US-Iran talks to reopen the Strait of Hormuz and end the months-long war. The Dow Jones Industrial Average rose 228.91 points, or 0.45%, to 51,307.79, the S&P 500 gained 9.82 points, or 0.13%, to 7,609.78 and the Nasdaq Composite gained 7.09 points, or 0.03%, to 27,093.90.

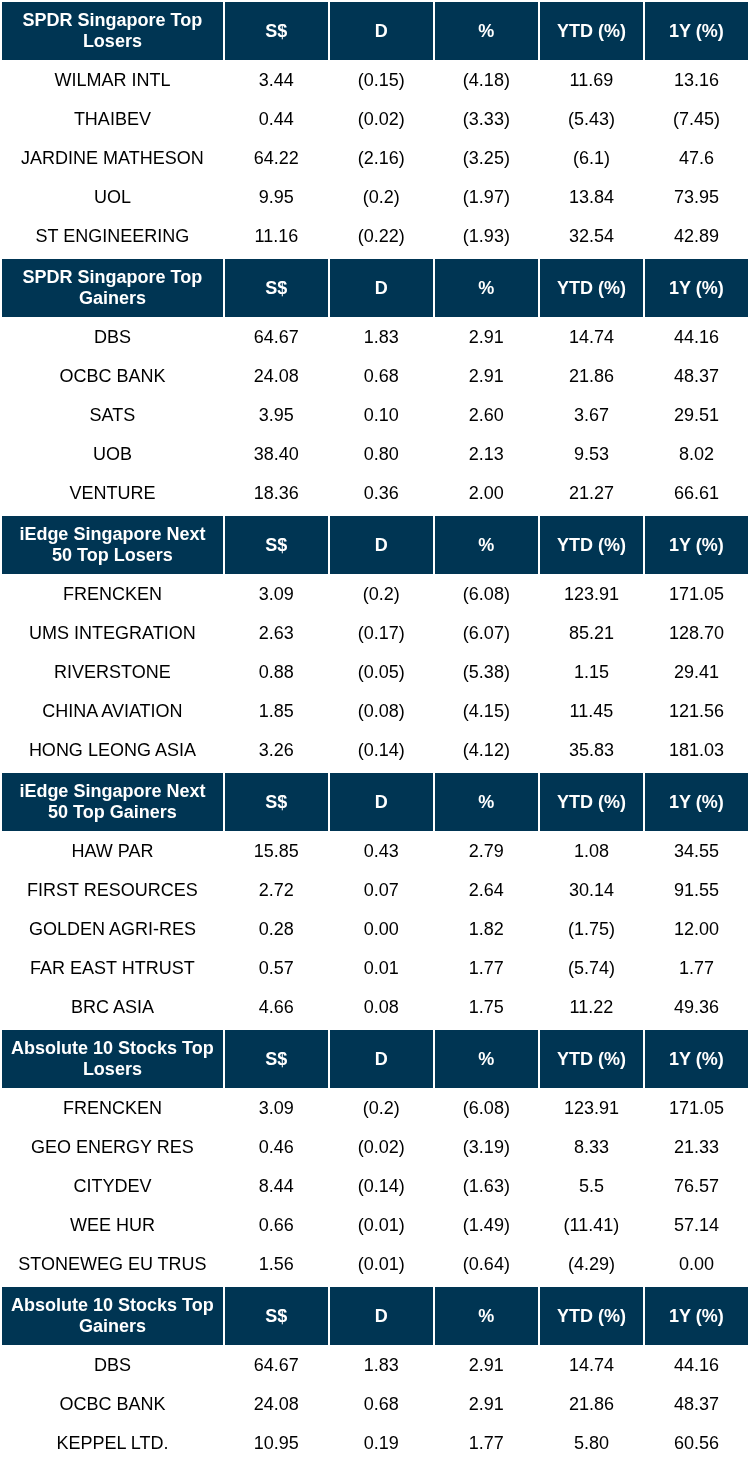

Singapore Technical Highlights

TOP 5 GAINERS & LOSERS

EVENTS OF THE WEEK

SG

ESR-REIT has established a S$2bn Euro Medium Term Securities Programme, with OCBC appointed as arranger. Proceeds will be used for refinancing existing borrowings, funding acquisitions and asset enhancement works, and general working capital.

AMTD IDEA Group has agreed to acquire a London office tower at 40 Furnival Street in Midtown for US$17mn, funded without external financing. The roughly 9,650 sq ft Grade A building will serve as a global headquarters for AMTD, The Art Newspaper and L’Officiel.

Del Monte Pacific has submitted a US$1.2bn debt restructuring plan, triggered by a negative stockholders’ equity position stemming from a US$703.5mn impairment tied to its former US subsidiary Del Monte Foods, which filed for Chapter 11 bankruptcy in July 2025.

US

Blackstone Inc raised $13.1bn for its third Asia private equity fund, more than double its 2021 fund and above its $10bn target.

Alphabet plans to raise $80bn in equity to fund AI compute infrastructure, citing customer demand outpacing supply. The raise includes a $10bn investment by Berkshire Hathaway, $30bn in underwritten offerings and $40bn through an at-the-market programme starting third quarter.

Microsoft unveiled Majorana 2, a new quantum computing chip redesigned with AI assistance, and set a 2029 target for commercially useful quantum systems, putting it level with rival IBM.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Yoma Strategic Holdings Ltd – Recovery broadening for this conglomerate

Recommendation: NON-RATED; TP S$; Last close: S$0.0840; Analyst Paul Chew

- FY26 EBITDA grew 18% YoY to US$45.9mn despite the 5% depreciation in currency. Property development remained the core earnings driver, rising 22% to US$38mn. The motor and financial divisions have returned to growth. F&B continue its steady rise in earnings with strong 20% same-store sales growth and store expansion.

- Demand for residential property is resilient due to urbanisation, migration and acts as a store of wealth. Property development has an unrecognised revenue backlog of US$90.3mn (FY25: US$92.5mn). The estimated pipeline of launches in FY27e is robust at US$110-120mn.

- The recovery in operating earnings is broadening. The momentum in residential property development is backed by a healthy backlog and pipeline of launches. Motor distribution sales are rebounding strongly as passenger cars and trucks are restocked. Finance (or Wave Money) is transitioning away from remittance fees toward interest income float that jumped ~80% in FY26. F&B is growing through store expansion and price increases. We expect cost pressures to rise due to the M East conflict. But the company’s strength lies in its ability to raise prices across all products. The company’s book value is currently S$0.193 per share. Net debt (excl. cash in trust) has declined to US$132mn (FY25: US$136mn).

Salesforce Inc – Share buyback cuts outstanding shares by 11%

Recommendation: BUY; TP US$270.00; Last close: US$191.00; Analyst Alif Fahmi

- 1Q27 revenue/PATMI met our expectations at 23%/26% of our FY27e forecasts. Revenue grew 13% YoY to US$11.1bn, driven by higher subscription sales. PATMI spiked 37% YoY, driven by higher operating leverage.

- We expect FY27e growth of 11% YoY, led by Platform Cloud (+30%) and supported by early Agentic AI adoption, where token usage is already growing rapidly. Expected reacceleration in 2H27e is driven by larger AI-led deal wins and strong monetisation across premium SKUs, seat expansion, and usage-based credits, while margins improve from AI-driven efficiency and disciplined headcount growth.

- We maintain a BUY recommendation with a higher DCF target price of US$270 (prev. US$253). We raised FY26e revenue estimates by 1% on stronger Platform Cloud growth, but cut PATMI by 6% due to higher expected interest expense (US$793mn finance cost at 3% rate) from the recently increased US$25bn debt, with LT debt rising to US$39bn from US$10bn QoQ. The higher TP reflects an 11% reduction in the share count due to the ASR, while WACC and terminal growth assumptions remain unchanged. Salesforce remains a leading enterprise CRM with a recurring subscription base and deep customer integration, expanding into AI-driven workflows via Data Cloud and Agentforce.

Market Journal articles powered by PhillipGPT

NetLink NBN Trust Maintains Steady Cash Flow Despite Rising Costs, Target Price Raised to S$0.96

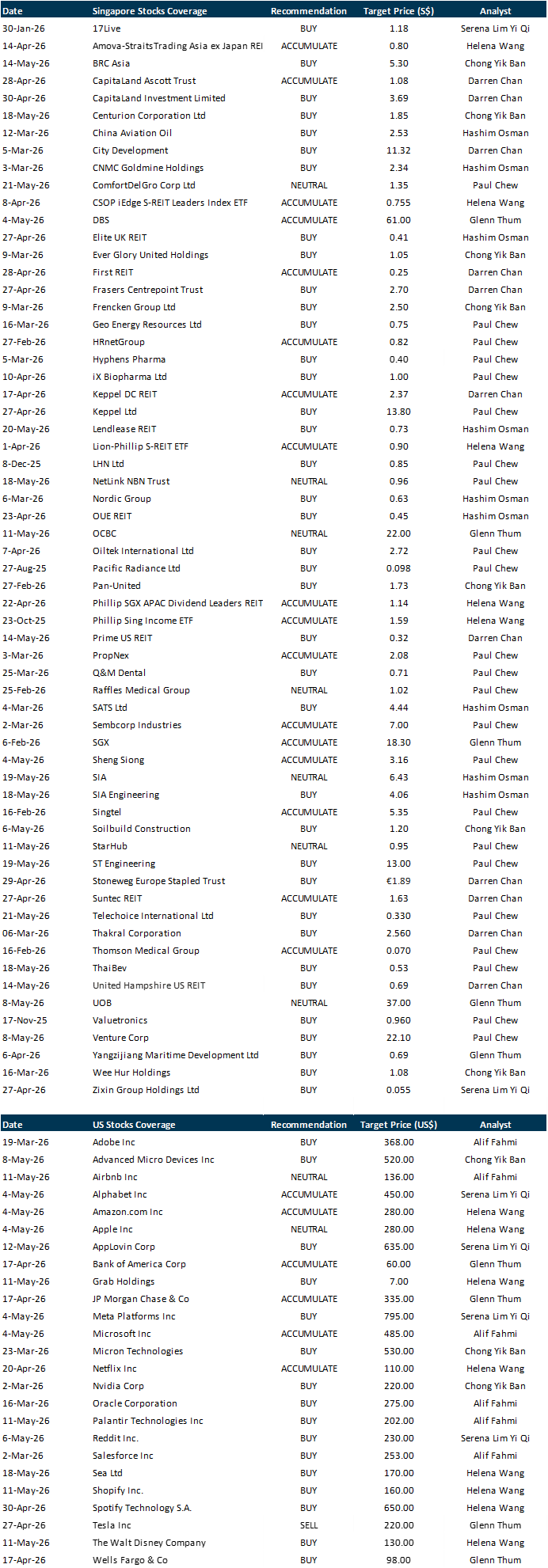

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Yoma Strategic Holdings Ltd [NEW]

Date & Time: 3 June 26 | 12PM-1PM

Register: poems-20260603-148171

Corporate Insights by AvePoint [NEW]

Date & Time: 3 June 26 | 7PM-8PM

Register: poems-20260603-149098

Corporate Insights by First REIT

Date & Time: 11 June 26 | 12PM-1PM

Register: poems-20260611-146839

Corporate Insights by AIMS APAC REIT

Date & Time: 17 June 26 | 12.30PM-1.30PM

Register: poems-20260528-145702

POEMS Podcast:

Research Videos

Weekly Market Outlook: NVDA, SIA, Micron, ST Engineering, Singtel & More!

Date: 25 May 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials