DAILY MORNING NOTE | 3 November 2025

Recent Podcasts:

Semiconductor 2Q25 Update

Shopify Inc. – Growth momentum to continue, but stock overvalued

Grab Holdings – Super-app strategy delivering scale efficiently

ETF Monthly: October 2025 – Muted performance for most asset classes in November

Analyst: Zane Aw

- Review of asset classes performance in October – It was a mixed bag. The ETFs tracking the S&P 500, US Treasury Bonds, Gold and Singapore Equities were in the green while those tracking Oil, Bitcoin and the Hang Seng Index fell. The top gainer was the ETF tracking Gold (GLDM), which was up 3.5%.

- For their current trends, the S&P 500, US Treasury Bonds and Singapore Equities are in an uptrend. Meanwhile, Gold, Oil, Bitcoin and the Hang Seng Index are in a range consolidation.

- Heading into November, we expect ETFs tracking the S&P 500, US Treasury Bonds, and Gold to consolidate sideways. On the other hand, ETFs tracking Oil, Bitcoin, and the Hang Seng Index are likely to extend their weakness into November. Singapore equities could remain a bright spot, with the uptrend expected to continue.

Week 45 equity strategy: The meeting between President Trump and President Xi was essentially a trade ceasefire. Tensions will flare up again, and “U-turns” will happen. But importantly, there is dialogue between both sides. Trump is expected to travel to Beijing in April, followed by Xi visiting the US later in the year. Any permanent end to trade tensions is the removal of semiconductor and rare earth export controls, which remain in place.

As expected, the Federal Reserve cut rates by 25 basis points to 3.75-4.00% last week. However, Fed chair Powell expressed uncertainty in cutting rates for December due to the lack of data. It is hard to guess rate cuts in every Fed meeting, but directionally, interest rates are heading downwards, in our opinion. Firstly, Powell did reiterate current monetary policy (or interest rates) is still modestly restrictive. Secondly, we will have a more dovish Fed chair by May next year, looking to cut interest rates more aggressively. Steve Miran’s dissenting vote, preferring to cut rates by 50 basis points, serves as a blueprint for the new Chairman. Thirdly, the current government shutdown will only slow the economy more than Fed projections. There is also a mini quantitative easing as the Fed reinvests maturing mortgages into shorter-dated Treasury bills.

It was mega tech reporting season. Based on our estimates, the 5 large Mag 7 reported an underlying net profit of US$128bn, rising by 19% YoY in 3Q25. Alphabet registered the fastest growth at 33% to US$34.9bn. Investors’ focus was on picking the AI winners. That baton was passed from Meta to Alphabet and, to a certain extent Amazon. For us, the strength of the underlying business and cash flow supports the ability to still fund their AI capex or arms race. For 2026 capex, all hyperscalers are guiding higher capex. A big winner of AI capex has been South Korea, with the market rallying 20% in October, supported in part by the surge in semiconductor memory demand.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore stocks ended lower on Oct 31, as the regional market closed mixed. The benchmark lost 0.2%, or 8.82 points, to finish at 4,428.62. Across the broader market, losers outnumbered gainers 299 to 268, after two billion securities worth $1.4 billion changed hands. The local banks all ended lower. DBS Bank lost 0.1% to finish at $53.93, OCBC Bank fell 0.1% to $17.03 and UOB was down 0.1% at $34.67.

Wall Street’s main stock indexes closed higher on Friday (Oct 31), with their biggest boost coming from Amazon’s upbeat earnings forecast, but sentiment was dampened by worries that the Federal Reserve is becoming more cautious about cutting rates. The Dow Jones Industrial Average rose 40.75 points, or 0.09%, to 47,562.87, the S&P 500 gained 17.86 points, or 0.26%, to 6,840.20 and the Nasdaq Composite gained 143.81 points, or 0.61%, to 23,724.96.

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

TOP 5 GAINERS & LOSERS

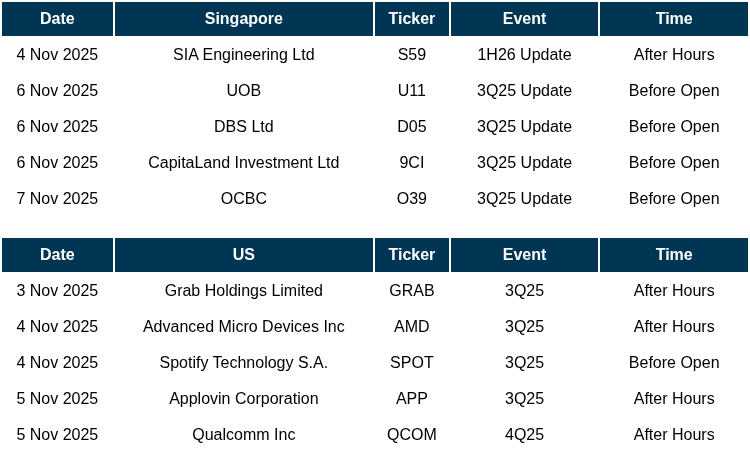

Events Of The Week

SG

CapitaLand India Trust (CLINT) announced 10% y-o-y growth in total property income and net property income (NPI) to $225.2 million and $172.1 million respectively, for the nine months to end-Sept (9MFY2025). 3QFY2026’s total property income and NPI also rose by 10% y-o-y to $76 million and $58.6 million respectively.

CapitaLand Ascendas REIT (CLAR) has reported portfolio occupancy of 91.3% for the 3QFY2025 ended Sept 30, 0.5 percentage points lower than the occupancy rate of 91.8% in the quarter before. All of CLAR’s markets, except Australia, saw q-o-q dips. Weighted average lease expiry (WALE) as at Sept 30 stood stable at 3.6 years.

Keppel Infrastructure Trust (KIT) is deepening its push into the digital infrastructure segment, identifying this industry as an area it wants more exposure to. The comments came as KIT marked its first foray into the segment with its proposed S$119 million acquisition of Global Marine Group (GMG), a subsea cable maintenance and installation vessel operator.

Wee Hur has taken a stake in a new fund managed by Singapore-based asset management firm Aravest that has bought the former Hotel Miramar Singapore in Havelock Road for S$160 million.

The price works out to about S$465,100 per room.

Shares in Yangzijiang Maritime, the spin-off listing of Yangzijiang Financial Holding, is expected to list on the Mainboard of the Singapore Exchange (SGX) at 9am on Nov 18. On Oct 31, the maritime investment business also announced its intention to raise $5.2 million via a private placement of 8.64 million shares at a placement price of 60 cents per share.

Chinese electric vehicle (EV) manufacturer Nio announced on Sunday (Nov 2) that it delivered 40,397 vehicles in October this year, up 92.6 per cent year on year.

US

A clutch of Federal Reserve bank presidents on Friday (Oct 31) aired their discomfort with the US central bank’s decision to cut interest rates this week, even as influential Fed Governor Christopher Waller made the case for more policy easing to shore up a weakening labour market.

US President Donald Trump said he didn’t discuss approving sales of Nvidia Corp’s Blackwell chips to China with his counterpart Xi Jinping, dampening speculation that Washington will allow exports of the powerful AI accelerators to the world’s largest semiconductor market.

Alphabet and Amazon were rewarded by investors for reporting better-than-expected third-quarter profits. At both companies, earnings were boosted by the increased value of their stakes in Anthropic PBC, maker of the popular Claude chatbot.

Meta Platforms Inc found record-shattering demand for its bond sale on Thursday even as its shares plunged, in a sign that bond investors are looking past any concerns about its artificial-intelligence (AI) spending plans.

Netflix Inc is actively exploring a bid for Warner Bros Discovery Inc’s studio and streaming businesses. The streaming company has hired Moelis & Co as its financial adviser and has gained access to financial data needed to evaluate whether to make a bid.

Intel Corp is in preliminary talks to buy artificial intelligence (AI) chip startup SambaNova Systems Inc. Intel is discussing the terms of an acquisition with SambaNova, which has been working with bankers to gauge interest from potential suitors.

Nvidia Corp forged a landmark deal to supply its technology to South Korea’s biggest companies, part of an aggressive push to expand AI infrastructure around the world.

Nvidia Corp chief executive officer Jensen Huang has sold more than US$1 billion worth of the chipmaker’s shares since June, completing a massive pre-planned stock sale.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Keppel Ltd – Asset management franchise building momentum

Recommendation: BUY; TP S$12.20; Last close: S$10.1900; Analyst Paul Chew

- Limited financials were provided, except that the 9M25 core net profit rose over 25% YoY. The growth rate is in line with 1H25 core net profit that climbed 29% YoY to S$444mn (excluding connectivity). More importantly, 9M25 recurring net profit (asset management and operating income excl. corporate) rose 15% YoY, faster than the 7% in 1H25.

- Asset management fees rose an estimated 8% YoY to S$104mn in 3Q25. The asset management franchise continues to build momentum. Equity raised 9M25 was S$2.7bn, a massive jump from 9M24 S$0.7bn. 3Q25 equity raised was S$0.8bn. Assets monetised jumped by S$1.47bn (M1 S$1.28bn/800 Super S$0.18bn) in 3Q25 (1H25 S$915mn).

- Our FY25e forecast is unchanged. We raised our SOTP-derived TP from S$10.70 to S$12.20 as we roll over our valuations to FY26e earnings. We maintain our BUY recommendation. FY26e will register stronger recurring earnings growth driven by the operations and maintenance income from Bifrost subsea fibre and waste to energy projects, Keppel Sakra Cogen Plant becomes operational 1H26, and rising funds under management. Other drivers of the share price include higher dividends from the planned S$14bn asset monetisation and the outstanding S$407mn share buyback programme. A loss from the M1 disposal will not affect dividends.

SG Bonds – Week 45: SGS Curve Steepens

Recommendation: REDUCE; TP S$; Last close: S$; Analyst Phillip Research Team

- The Fed cut interest rates by 25 bps to 3.75-4.00% and announced it will halt balance-sheet reduction from 1 December, marking the end of quantitative tightening that began in 2022.Despite this, Treasury yields continued to edge higher as markets reassessed the likelihood of another December rate cut.

- SGS yields rose across the curve in late October, with the 5Y up ~5 bps to 1.62% and the 10Y up to 1.90%, marking a mild bear-steepening as investors pared back expectations for near-term Fed easing following Chair Powell’s comments that additional rate cuts are “not a foregone conclusion.”

- The near-term macro backdrop remains cautiously constructive. The Fed’s decision to end quantitative tightening signals a gradual pivot toward policy normalization, though officials remain non-committal on the timing of further rate cuts.

- 3Q25 results were within expectations. 9M25 revenue and adjusted PATMI were 75%/76%, respectively, of our FY25e forecast. Adjusted PATMI (excluding gain on lease) rose 6.3% YoY to S$41.5mn. Pressuring net margins were higher wages, lower finance income, and a decline in wage grants.

- Sheng Siong (SSG) has grown its store footprint by 13% YoY (or 11 new stores) to 84. Two new stores will open in 4Q25. 2025 will record 10 new stores or an 11% rise in footprint to 736k sft. It will be the largest number of store openings since 2018 and support revenue growth for FY26e.

- We maintain our FY25e forecast. Our target price is raised from S$2.30 to S$2.55 as we roll over valuations to FY26e earnings. We peg SSG to 23x PE, valuations the company enjoyed during its growth years. Our ACCUMULATE recommendation is maintained. The pipeline for new stores remains robust, with opportunities in HDB and private-market locations. However, net margins will be under pressure in the near term from the new S$520mn Sungei Kadut distribution centre and extension of the progressive wage model.

- 3Q25 DPU of 1.778 Singapore cents rose 12.5% YoY, beating our expectations and forming 28% of our FY25e forecast (9M25: 78%). This outperformance was driven by lower finance costs (-44bps YoY), stronger operating performance from the Singapore portfolio, and a S$2mn reversal of withholding tax provisions for the Australia portfolio. Excluding the tax reversal, 3Q25 DPU was still 8% higher YoY.

- In 3Q25, SUN achieved strong rental reversion rates of +8.5% and +8.6% for its Singapore office and retail segments, respectively. The Australia portfolio underperformed due to a weaker AUD against the SGD and lower occupancy, leading to an 11.3% YoY decline in NPI. Interest costs fell 44bps YoY to 3.62% and are expected to stay around this level in 4Q25.

- We downgrade SUN from BUY to ACCUMULATE with a higher DDM-TP of S$1.40 (prev: S$1.36) due to the recent share price performance. We raise our FY25e DPU estimate by 6% on lower interest costs and the reversal of tax provisions (another S$2mn expected in 4Q25). SUN’s portfolio resilience is anchored by its Singapore assets, which contribute c.70% of income. We expect low-teens rental reversions for the Singapore retail segment and high-single-digit reversions for the office segment in FY25e. SUN is currently trading at an FY25e dividend yield of 5.7% and P/NAV of 0.58x.

- 3Q25 revenue and PATMI were within our expectations, with revenue surpassing US$100bn for the first time (+16% YoY), and PATMI increased 33% YoY. 9M25 revenue/PATMI were at 71% of our FY25e forecast.

- Strong revenue growth across all core business segments due to 1) resilient Search & YouTube ads growth (+15% YoY) with Gemini integration in Search and increasing Shorts monetisation, and 2) continuing strong Cloud demand (+34% YoY).

- We upgraded our rating to BUY and raised DCF target price to US$340 (prev. US$265) due to GOOGL’s expanding monetisation potentials as a full-stake AI provider. We increased our FY25e revenue forecast by ~2%, reflecting strength in advertising and Cloud business. WACC remains unchanged at 7.4% but we raised the terminal growth rate to 5.5% from 5% due to GOOGL’s strong fundamentals and product differentiation. We expect the company to continue benefiting from AI-driven improvements, particularly in enhancing cloud capacity and ad targeting capabilities.

- 3Q25 revenue/Adjusted PATMI grew 13%/4% and were in line with expectations. 9M25 Revenue/Adjusted PATMI were at 70%/79% of our FY25e forecasts.

- The primary revenue driver was AWS (+20% YoY) and advertising (+24% YoY). AWS’s operating margin compressed 3.5% YoY to 34.6%, due to heavy AI investment. Retail margin compressed 1.4% due to US$1.8bn severance cost and US$2.5bn legal settlement charge.

- We increase our FY25e revenue by 1% and PATMI by 6% to account for the growing demand in AWS as well as continued cost discipline efforts in the retail segment. We increase our DCF target price to US$290 (prev. US$260). We downgrade our recommendation from BUY to ACCUMULATE due to recent price rally. WACC of 6.4% and a terminal growth rate of 5% remaining unchanged. AMZN’s outlook remains strong with AWS reaccelerating.

- 3Q25 results exceeded our expectations, with revenue up 26% YoY to US$51.2bn and adj. PATMI increased 19% YoY to US$18.6bn from strong ad revenue growth. 9M25 revenue/PATMI was at 70%/87% of our FY25e forecasts.

- AI continues to deliver strong ad results, with better user engagement and ad performance leading to a 10% YoY increase in ad prices and 14% YoY growth in impressions. Instagram now has 3bn monthly active users (MAUs).

- We maintained ACCUMULATE rating but reduce the DCF target price to US$770 (prev. US$830). We raise our FY25e PATMI forecast by 14%, driven by lower-than-expected non-research and development (non-R&D) expenses. Our WACC remains at 7.5%, but we have reduced the terminal growth rate to 5.4% (from 6.0%) to reflect the impact of META’s significant CAPEX commitments in growing Superintelligent Lab. However, we think the investment size remains reasonable given the intense competition and the fact that META still has strong monetisation power through its product offerings.

- We value Lion-Phillip S-REIT ETF (SREITS) using a combination of historical dividend yield spread and price-to-book ratios. The prices are S$1.03 and S$0.90, respectively, using these two valuation methods. We maintain our ACCUMULATE recommendation by assigning equal weight to both valuations; we increase our target price to S$0.965 (previously S$0.86).

- CDL Hospitality Trusts and Digital Core REIT Management were taken out of the constituents since our last update on the ETF. SREITS remains well-diversified across eight sectors, with industrial at 41.1% as the largest.

- DPU remains stable between 4-6 cents. We expected an improvement in DPU following the Federal Reserve’s rate cut.

Sheng Siong Group Ltd – More stores, more growth ahead

Recommendation: ACCUMULATE; TP S$2.55; Last close: S$2.3200; Analyst Paul Chew

Suntec REIT – Low interest hedge ratio supports DPU growth

Recommendation: ACCUMULATE; TP S$1.40; Last close: S$1.3400; Analyst Darren Chan

Alphabet Inc – Revenue surpasses US$100bn on AI growth

Recommendation: BUY; TP US$340.00; Last close: US$; Analyst Serena Lim Yi Qi

Amazon.com Inc.- AWS growth accelerating

Recommendation: ACCUMULATE; TP US$290.00; Last close: US$; Analyst Helena Wang

Meta Platform Inc. – Higher CAPEX overshadows strong ad performance

Recommendation: ACCUMULATE; TP US$770.00; Last close: US$; Analyst Serena Lim Yi Qi

Lion-Phillip S-REIT ETF – Rate cuts should support dividends

Recommendation: ACCUMULATE; TP S$0.965; Last close: S$0.8780; Analyst Helena Wang

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by AA REIT [NEW]

Date & Time: 5 November 25 | 12PM-1PM

Register: poems-20251105-132684

Corporate Insights by Keppel Infrastructure Trust (KIT)

Date & Time: 6 November 25 | 12PM-1PM

Register: poems-20251106-132232

Corporate Insights by Prime US REIT [NEW]

Date & Time: 12 November 25 | 12.30PM-1.30PM

Register: poems-20251112-132944

POEMS Podcast:

Research Videos

Weekly Market Outlook: JPM, Wells Fargo, BAC, Netflix, Oracle, Keppel DC REIT, Tech Analysis & More!

Date: 27 Oct 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials