DAILY MORNING NOTE | 31 July 2025

Recent Podcasts:

Centurion Corporation Ltd – A New EPIISOD

Phillip Singapore 3Q25 Strategy: Going local

Semiconductor 1Q25 Update – AI demand offsets impact from US export controls

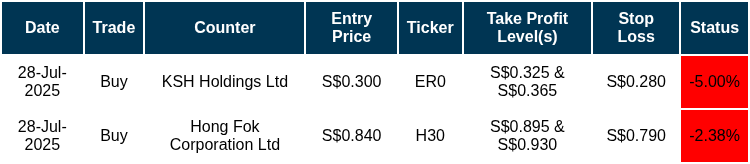

Trades Initiated in Past Week

Singapore stocks slipped for the fourth straight session on Wednesday, logging their longest losing streak in five weeks, as second-quarter employment growth slowed from the same period a year ago. The local benchmark index fell 0.2% or 10 points to end at 4,219.41. Across the broader market, losers outnumbered gainers 342 to 222, with around 1.8 billion securities worth S$2.1 billion changing hands.

The S&P 500 gave up earlier gains and closed lower on Wednesday after Federal Reserve Chair Jerome Powell signaled the central bank isn’t ready to cut rates, as it assesses the impact of President Donald Trump’s higher tariffs on the inflation picture. The broad market index slipped 0.12% and closed at 6,362.90. The Dow Jones Industrial Average fell 171.71 points, or 0.38%, closing at 44,461.28. The Nasdaq Composite gained 0.15% and ended at 21,129.67. At their session highs, the S&P 500 was up by as much as 0.4%, while the Dow was up 0.2%.

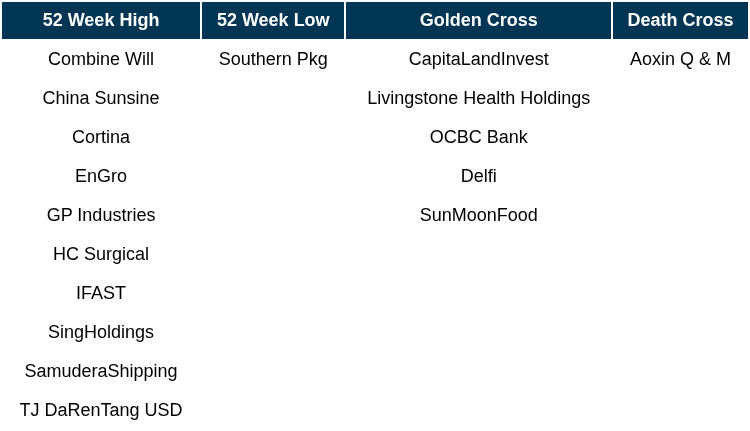

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

TOP 5 GAINERS & LOSERS

Events Of The Week

SG

Seatrium will pay financial penalties to both Singapore and Brazilian authorities totalling some $241.7 million to settle a long-drawn corruption case in Brazil, when the company was known as Sembcorp Marine. With this payment as part of a deferred prosecution agreement, or DPA, the authorities have concluded joint investigations on Seatrium, and no further action will be taken.

Seatrium has reported earnings of $144 million for 1HFY2025, up 301% y-o-y. Revenue in the same period ended June 30 was up 34% to $5.4 billion. Due to a more favourable mix of projects and better efficiencies, Seatrium was able to improve its gross margin from 3.7% in 1HFY2024 to 7.4% in 1HFY2025. As at end-June 2025, Seatrium’s net order book stood at $18.6 billion, of which $6.3 billion are renewables and cleaner/green solutions.

Over 2,000 retail tenants across 11 of Frasers Property’s malls like Northpoint City, Waterway Point, Causeway Point and Tiong Bahru Plaza will enjoy financial solutions and preferential rates from DBS Bank under a new partnership between the two companies. This is in addition to DBS’s SG60 Heartland Merchant Banking package, which provides financing support for small businesses. Each merchant can save up to $1,880 through waivers and cashback benefits.

Keppel Limited has divested about $477 million worth of real estate assets as part of its accelerated monetisation programme. The latest set of divestments has brought the group’s latest monetisation figure to $915 million year to date. The transactions include the divestment of Keppel’s entire stakes in a commercial building in India for $379 million and its stakes in Vietnamese developer Nam Long for some $58 million. The group also divested a partial 2.5% stake in Smartworks Coworking Spaces after the latter’s initial public offering (IPO) in India in July.

Jardine Cycle & Carriage has reported an underlying profit of US$529 million ($682.14 million), up 6% y-o-y for 1HFY2025 ended June 30. After accounting for non-trading items that are unrealised gains/losses arising from the revaluation of the group’s non-current investments, the group reported a profit attributable to shareholders of US$371 million, down 23% y-o-y for 1HFY2025.

Grab Holdings beat Wall Street expectations for second-quarter revenue on Wednesday, as consumers boosted spending on its ride-hailing and food delivery platform despite global economic uncertainty. The Singapore-based company reported revenue of $819 million, above analysts’ expectations of $811.3 million, according to LSEG data.

The Monetary Authority of Singapore (MAS) will maintain the rate of appreciation of the Singapore dollar nominal effective exchange rate (S$NEER) policy band in July after easing its monetary policy in January and April this year. There will be no change to the band’s width and the level at which it is centred.

The Monetary Authority of Singapore (MAS) projects Singapore’s economy to be “relatively subdued” for the rest of the year.The forecast follows the nation avoiding a technical recession in the 2Q2025. Based on advance estimates, Singapore’s economy expanded by 1.4% q-o-q seasonally-adjusted, reversing from the 0.5% contraction in the first quarter. On a y-o-y basis, gross domestic product (GDP) growth stayed firm at 4.3%, extending the 4.1% growth in the previous quarter.

US

President Donald Trump said he would impose a 25% tariff on India’s exports to the US starting Friday and threatened an additional penalty over the country’s energy purchases from Russia. Trump on Wednesday said he made the decision because India has tariffs that are “among the highest in the World, and they have the most strenuous and obnoxious non-monetary Trade Barriers of any Country.”

President Donald Trump said he reached a trade deal with South Korea that would impose a 15% tariff on its exports to the US and see Seoul agree to US$350 billion in US investments. “We have agreed to a Tariff for South Korea of 15%. America will not be charged a Tariff,” Trump said in a post to his social media platform on Wednesday.

Meta reported robust second-quarter financial results on Wednesday, with revenue jumping 22 per cent year-over-year to US$47.5 billion as the social media giant continues investing heavily in artificial intelligence. The Facebook and Instagram owner’s share price soared as much as 12 per cent in after-hours trading, with investors buoyed by the company’s growing advertising business and a rise in users across its family of platforms.

Microsoft reported better-than-expected growth in its cloud business and said spending on artificial intelligence (AI) infrastructure hit a record. The closely watched Azure cloud-computing unit posted a 39 per cent rise in sales during Microsoft’s fiscal fourth quarter, the company said on Wednesday. Analysts projected 34 per cent revenue growth.

Federal Reserve Chair Jerome Powell said interest rates are in the right place to manage continued uncertainty around tariffs and inflation, tempering expectations for a rate cut in September. “There are many, many uncertainties left to resolve,” Powell told reporters Wednesday following the central bank’s decision to once again keep rates unchanged. “It doesn’t feel like we are very close to the end of that process.” The Federal Open Market Committee voted 9-2 to hold its benchmark federal funds rate in a range of 4.25%-4.5%, as it has at each of its meetings this year. Governors Christopher Waller and Michelle Bowman voted against the decision in favour of a quarter-point cut.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Astrea 9 PE Bonds – Balancing yield, risk, and private equity exposure

Recommendation: REDUCE; TP S$; Last close: S$; Analyst Darren Chan

- Astrea 9 is the latest issuance in the Astrea bond series. The bonds are backed by the cash flows from a diversified portfolio of private equity funds, providing exposure to this asset class.

- Class A-1 (SGD-denominated) and Class A-2 (USD-denominated) bonds are expected to be investment grade rated by Fitch at A+sf and Asf, respectively, while the Class B PIK (Paid-in-kind) bonds are expected to be rated BBBsf. Class A-1 and A-2 bonds are available to retail investors through ATMs, mobile banking, and internet banking, whereas Class B PIK bonds are not.

- Astrea 9 includes multiple structural safeguards such as cash reserves, priority of payments, and leverage limits to enhance stability and protect bondholders’ interests.

Far East Hospitality Trust – DPU upside from lower finance cost

Recommendation: BUY; TP S$0.70; Last close: S$0.6100; Analyst Liu Miaomiao

- 1H25 DPU declined 9.2% YoY to 1.78 cents, in line with our expectations and forming 47% of FY25e estimates. The drop was mainly due to lower contributions from the hospitality segment, in the absence of large-scale events.

- Revenue from the commercial segment rose 6.4% YoY to S$9.2mn in 1H25, while the new Sheraton Nagoya contributed positively with S$1.6mn, partially offsetting the weakness in the Singapore hospitality segment (-9.8%YoY). Hotel RevPAR declined 5.3% YoY to S$131 in 2Q25, driven by a 4.6% YoY drop in ADR and a 0.6ppt decline in occupancy rate.

- FEHT will distribute the final S$2.5mn of proceeds from the Central Square divestment in 2H25, bringing the total distribution for the year to S$8.0mn. There will be no capital top-ups from FY26e onwards. We lower our FY25e–26e DPU forecasts by 3% to 3.62–3.58 cents, reflecting softer leisure demand and a subdued event calendar. FY25e DPU is expected to be supported by lower finance costs, which declined 15.8% in 1H25, and the cost of borrowing is expected to trend down further in 2H25 (2Q25: 3.4%). We maintain our BUY rating with an unchanged DDM-TP of S$0.70. The REIT is trading at a FY25e dividend yield of 6.0% and 0.67x P/NAV.

Raffles Medical Group Ltd – Returning capital while waiting for China

Recommendation: NEUTRAL; TP S$1.02; Last close: S$1.0200; Analyst Paul Chew

- 1H25 revenue and PATMI were within our expectations at 48%/45% of our FY25e estimates respectively. Revenue growth was softer, largely driven by insurance services.

- We believe patient volumes were weak but supported by higher revenue intensity, especially in oncology and orthopaedics. Turnover in China contracted 2% YoY in 1H25 to S$29.9mn, in part due to a 2.3% weaker renminbi. The turnaround in China is progressing. Collaboration with public hospitals will help raise the number of visiting specialists to Raffles Hospital in China.

- Our FY25e PATMI and DCF target price of S$1.02 is maintained. We downgrade our ACCUMULATE recommendation to NEUTRAL due to the recent share price performance. Growth in Singapore will be tepid with upside from a turnaround in insurance profitability as loss ratios and claims are tightened. Cost pressures will rise with a salary increase for public healthcare workers on 1st July. Raffles is reiterating its dividend policy of at least 50% and share buyback up to 100mn shares over the next 2 years (30Jun25: Treasury shares 33.594mn).

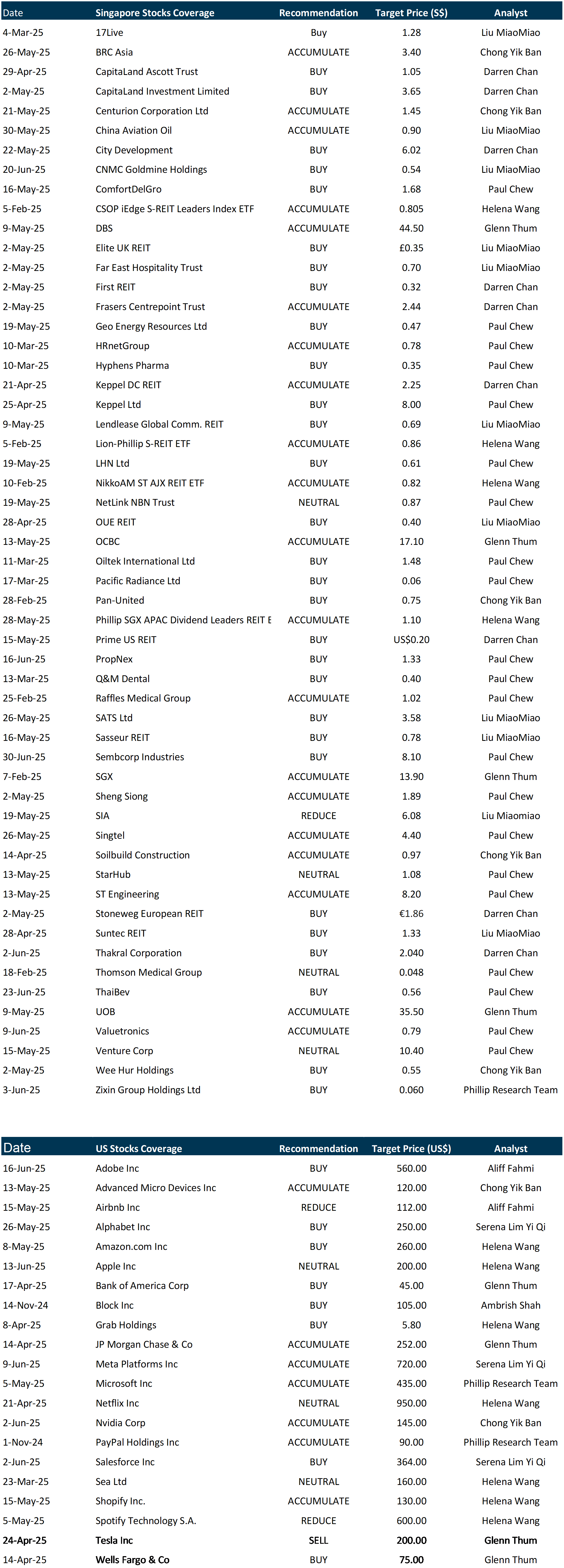

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by AA REIT

Date & Time: 31 July 25 | 12PM-1PM

Register: poems-20250731-125608

Corporate Insights by Keppel DC REIT

Date & Time: 1 August 25 | 12PM-1PM

Register: poems-20250801-125512

Corporate Insights by BHG Retail REIT

Date & Time: 12 August 25 | 12PM-1PM

Register: poems-20250812-125487

Corporate Insights by Prime US REIT

Date & Time: 13 August 25 | 12PM-1PM

Register: poems-20250813-126111

Corporate Insights by Manulife US REIT

Date & Time: 19 August 25 | 12PM-1PM

Register: poems-20250819-125582

Corporate Insights by Daiwa House Logistic Trust(DHLT) [NEW]

Date & Time: 26 August 25 | 12PM-1PM

Register: poems-20250826-126300

POEMS Podcast:

Research Videos

Weekly Market Outlook: BAC, Tesla, Netflix, OCBC, OUE REIT, Suntec REIT, SG Weekly & More!

Date: 28 July 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials