DAILY MORNING NOTE | 4 August 2025

Recent Podcasts:

Netflix Inc.- Tough to surpass high expectations

Centurion Corporation Ltd – A New EPIISOD

Phillip Singapore 3Q25 Strategy: Going local

ETF Monthly: July 2025 – Mostly sideways or down in August

Analyst: Zane Aw

- Review of asset classes performance in July – Most ETFs were in the green except those tracking US Treasury Bonds (IEF) and Gold (GLDM), which were both down slightly by 0.5%. The top gainer was the ETF tracking Bitcoin (BITO), which gained 8%.

- For their current trends, the S&P 500, Bitcoin, Singapore Equities and Hang Seng Index are in an uptrend. Meanwhile, US Treasury Bonds, Gold and Oil are in a range consolidation.

- Heading into August, we expect price consolidation for ETFs tracking the US Treasury Bonds, Gold, and Hang Seng Index. Meanwhile, ETFs tracking the S&P 500, Oil, and Singapore Equities are expected to pull back. On the other hand, the ETF tracking Bitcoin could extend its gains from July.

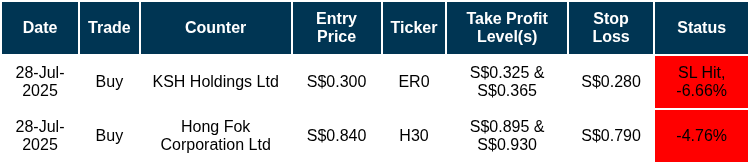

Trades Initiated in Past Week

Week 32 equity strategy : The US markets faced a slew of negative macro data. Whilst US 2Q25 real GDP grew at a headline 3% YoY, 5% points came from lower imports. Both corporate (-3%) and consumer spending (+1%) slowed. Next comes payrolls that only rose 73k against the estimate of 100k. Job losses were seen in manufacturing, government, professionals, and IT. More shocking was the massive 88% revision downwards of the May and June payrolls (or combined 258k). May and June payroll adds now average 16.5k per month. Bond markets immediately reacted with a 20/25bps drop in 10Y/2Y Treasuries to 4.2%/3.7%. The Fed remain steadfast on keeping rates stable. J William said the labour market is still solid. Chris X. J Powell earlier mentioned that slowing job creation is in balance with the slowing supply of workers. Therefore, his focus is on the unemployment rate. Trump’s sacking of the department that collates employment data (or BLS) cannot deny the fact that labour is slowing. The number of unemployed for 27 weeks is 1.8mn, the highest since 2017, excluding the pandemic. A slowing labour market is positive for Singapore REITs as it raises the likelihood of interest rate cuts. We believe any sharp sell down to the equity market due to a softening labour market will be backstopped by Fed rate cuts and quantitative easing.

The tariff results are in, and Singapore appears to be a winner compared to Asian peers. The 10% is the lowest amongst fellow Asian exporters – Taiwan/Vietnam (20%), Malaysia/Thailand/Indonesia/Philippines (19%) and South Korea/Japan (15%). Still pending are the tariffs on semiconductors and pharmaceuticals. Our view of tariffs is a contraction in demand from US consumers as they bear the brunt of higher import prices. We expect US consumer to rely on more debt to maintain their consumption levels.

Singapore equities ended July with a gain of 5.3% (YTD +10.2%). REIT underperformed with a 2.4% rise (YTD +5.0%). Whilst small caps rallied hard with a 9.9% gain (YTD 15.8%). The large-cap index gainers were DFI (+25%), CDL (+19%) and Yangzijiang Shipbuilding (+15%). Meanwhile, the huge mid-cap winners (under our coverage) were Oiltek (+61%), Wee Hur (+36%) and Frencken (+34%).

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Local stocks fell for the sixth consecutive session on Friday (Aug 1). The benchmark fell 0.5 per cent or 19.94 points to 4,153.83. Across the broader market, losers beat gainers 340 to 244, with around 1.3 billion securities worth nearly S$1.7 billion transacted.

Wall Street stocks finished sharply lower Friday (Aug 1) following a weak July jobs report that raised concerns about US economic health. Major US indices fell 1.2 per cent or more after the Department of Labor reported lower than expected jobs data for July and announced downward revisions to the prior two months. The Dow Jones Industrial Average finished down 1.2 per cent at 43,588.58. The broad-based S&P 500 fell 1.6 per cent to 6,238.01, while the tech-rich Nasdaq Composite Index dropped 2.2 per cent to 20,650.13.

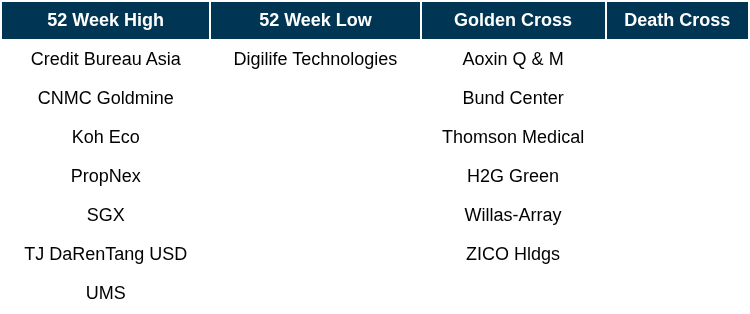

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

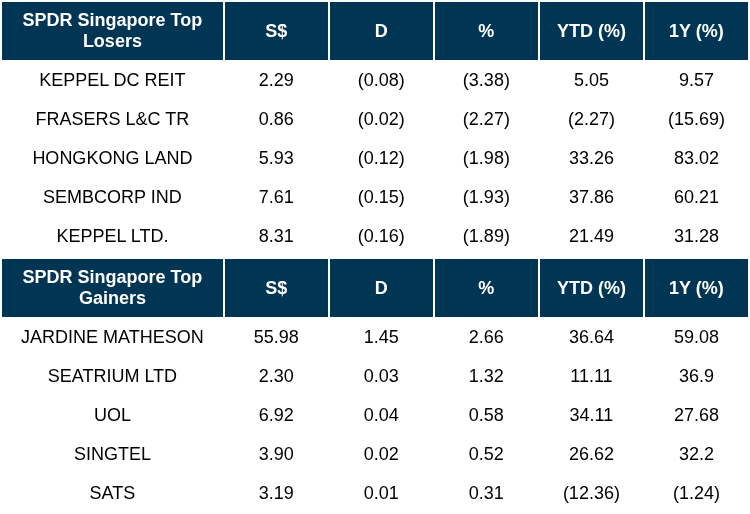

TOP 5 GAINERS & LOSERS

Events Of The Week

SG

The Republic’s manufacturing sector slipped back into contraction in July, even as the key electronics segment continued to expand. The purchasing managers’ index (PMI) fell to 49.9, a 0.1 point dip from June.

CosmoSteel will be suspended and eventually delisted, after the offer by investment holding company 3HA Capital to privatise the group at S$0.25 a share closes on Friday (Aug 1).

Dezign Format is set to raise S$6.5 million in gross proceeds through an Catalist IPO, with a market capitalisation of S$40 million after listing. Since 2022, its financial performance has steadily improved with revenue rising from S$18.3 million in FY2022 to S$33.4 million in FY2024.

Power distribution solutions provider Tai Sin Electric has entered into a share subscription agreement to acquire a 25 per cent stake in charging station contractor EV Mobility on Friday (Aug 1).

UOB is cutting interest rates on its flagship savings account, the One Account, for the second time in 2025. From Sep 1, the maximum effective interest rate on the One Account will decrease to 2.5 per cent per annum on the first S$150,000, down from 3.3 per cent.

UMS Integration expects to see in the next few years the fruits of the S$120 million investment it made over the past three years, as it rides the semiconductor boom.

Shares of Thai Airways International will resume trading on Monday (Aug 4) in Bangkok for the first time in five years, the culmination of the state-controlled airline’s emergence from its US$12 billion debt restructuring.

US

Warren Buffett’s Berkshire Hathaway took a US$3.8 billion impairment on its Kraft Heinz stake, the latest hit to a bet that’s weighed on the billionaire investor’s company in recent years.

Blackstone sold more than £1.5 billion (S$2.6 billion) in bonds backed by UK holiday parks operated by Haven, the largest ever pound-denominated commercial mortgage security since the 2008 financial crisis.

Airbus delivered about 63 aircraft last month, roughly 18 per cent fewer than during the same month a year ago, as a shortage of engines on its best-selling A320neo model hampered handovers to customers.

Chinese chipmaker InnoScience Suzhou Technology Holding closed up 31 per cent in Hong Kong on Friday (Aug 1) after it was identified by Nvidia as a supplier.

ExxonMobil reported a drop in second-quarter profits on Friday (Aug 1) as the hit from lower crude prices more than offset a boost from higher oil and gas production. The petroleum giant reported profits down 23.4 per cent from the year-ago period. Crude prices were under US$65 a barrel, more than US$10 less than the level in the 2024 quarter.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Keppel Ltd – Clarity in “hong bao” draws

Recommendation: BUY; TP S$10.50; Last close: S$8.3100; Analyst Paul Chew

- 1H25 revenue and adjusted PATMI were within our expectations at 44%/43% respectively of our FY25e forecast. Adjusted PATMI (excl. non-core / valuation/divestments) grew 9% YoY to S$374mn primarily due to asset management fees contributed by Aermont.

- Keppel has separated a pool of assets worth S$14.4bn in the balance sheet (with S$4.7bn NAV) deemed non-core that will be monetised. Management is reiterating its target of S$10-12bn asset monetisation by end 2026, of which S$7.8bn has been completed. The management has provided greater clarity on the assets that will be monetised and capital returned to shareholders. A S$500mn share buyback programme was announced whilst the interim dividend was maintained at 15 cents.

- We maintain our FY25e adjusted earnings. Our SOTP-derived TP is raised to S$10.50 (prev. S$8.00) and BUY recommendation is maintained. We raised our valuations for infrastructure and asset management, driven by the expected earnings spurt over the next 2-3 years. We also removed the holding co discount due to the virtuous synergies as asset owner and operator across the key divisions of infrastructure, real estate, asset management, and connectivity. FY26e will be a year of growth from Keppel South Central, Keppel Sakra Cogen power plant, and Bifrost cables completions.

Oiltek International Ltd – Prepare for the next wave

Recommendation: BUY; TP S$1.18; Last close: S$0.9800; Analyst Paul Chew

- 1H25 PATMI was within our expectations at 49% of our FY25e forecast. Underlying net profit (excl. FX translation loss) jumped 92% YoY to RM17mn. Revenue was below expectations at 34% of our FY25e.

- Gross margins expanded almost 13% points to 32.2% from procurement and re-engineering savings. Timing of projects will also impact gross margins. Interim dividend rose 67% YoY to 0.5 cents. The company ended 1H25 with net cash of RM111.7mn (1H24: RM103.9mn).

- We maintain of FY25e earnings and lift FY26e earning by 20% to RM47.6mn. We are raising our valuations to a bull case scenario. Listed peers in Malaysia are trading at 19x PE FY26e but with slower earnings growth of 16%. In contrast, Oiltek’s growth has been compounding at around 50%. With a better earnings growth profile and huge upcoming opportunities in SAF, we believe a premium valuation is warranted. We peg Oiltek to 35x PE FY26e or target price of S$1.18. Historical valuations have already hit 45x, and we see no slowdown in earnings growth. We expect order momentum to expand from SAF pre-treatment units, Latin America, biodiesel regionally, and new refining capacity.

Oversea-Chinese Banking Corp Ltd – NII guidance lowered

Recommendation: NEUTRAL; TP S$16.50; Last close: S$16.7900; Analyst Glenn Thum

- 2Q25 earnings of S$1.82bn were below our estimates as continued NIM compression led to lower NII. 1H25 PATMI was 47% of our FY25e forecast. Interim dividend fell 7% YoY to 41 cents, with dividend payout ratio stable at 50%. OCBC has reiterated its S$2.5bn capital return (special dividend equivalent to 10% dividend payout ratio and ~S$1bn share buyback) previously announced.

- NII dipped 6% YoY as loan growth of 7% was offset by NIM declining 28bps YoY to 1.92%. Total non-interest income rose 5% YoY from fee and trading income, while allowances declined and expenses were stable. OCBC has lowered its FY25e guidance for NIM of 1.90-1.95% (prev. around 2%) with NII to decline by mid-single digit but maintained guidance of mid-single digit loan growth and credit costs of around 20 to 25bps.

- Downgrade to NEUTRAL from Accumulate with a lower target price of S$16.50 (prev. S$17.60). We lower our FY25e earnings estimate by ~6% from lower NII estimates. We assume a 1.25x FY25e P/BV and a 12.5% ROE estimate in our GGM valuation. We expect FY25e earnings to decline by ~2% from the continued compression in NIM and decline in NII, which higher fees and trading income would partially offset. OCBC’s dividend yield is the least predictable amongst the 3 local banks as the dividend policy is fully floating (dividend payout ratio of 50% base and 10% special) and is entirely dependent on the direction of earnings. However, we believe OCBC can go above the minimum dividend payout ratio and to continue the special dividend (an additional 10% dividend payout ratio) for at least two more years (until FY27) as they still have the highest CET1 ratio among the local banks (2Q25 fully phased-in CET1: 15.3%).

First REIT – Facing ongoing FX headwinds

Recommendation: BUY; TP S$0.31; Last close: S$0.2700; Analyst Darren Chan

- 2Q25/1H25 DPU of 0.55/1.13 Singapore cents (-8.3%/-5.8 YoY) was slightly below our estimates, forming 23%/48% of our FY25e forecast. The YoY decline in DPU was due to the depreciation of the IDR and JPY against the SGD, partially offset by higher rental income in local currency terms.

- Rental income from Indonesia and Singapore rose 5.5% and 2% respectively in local currency terms, while income from Japan remained stable. As of 30 June 2025, overdue rent from PT MPU stood at S$7.0mn (1Q25: S$5.8mn), with S$0.9mn received in July 2025.

- Maintain BUY with a lower DDM-derived target price of S$0.31 (prev. S$0.32). We trim our FY25e/26e DPU estimates by 3%/1% due to ongoing FX headwinds, particularly the weaker Rupiah. Despite this, FIRT offers an attractive FY25e DPU yield of 8.4%. It is undergoing a strategic review in response to Siloam’s letter of intent (LOI) to acquire its Indonesian hospital assets, with no material updates as of 2Q25. In the meantime, organic growth will be driven by more Indonesian hospitals transitioning to performance-based rent from the current three.

Grab Holdings- Super-app strategy delivering scale efficiently

Recommendation: BUY; TP US$5.80; Last close: US$; Analyst Helena Wang

- Both 2Q25 revenue and PATMI met our estimates. 1H25 revenue/PATMI were at 47%/17% of our FY25e forecasts. We expect PATMI to be backloaded in 2H25 as the company turns profitable.

- Revenue growth remains strong, +23% YoY to US$819mn. This growth was primarily propelled by strong performances in both its On-Demand services (+22% YoY) and Financial Services arm (+40% YoY).

- We keep our FY25e revenue assumption unchanged. We maintain our BUY recommendation with an unchanged DCF target price of US$5.80, with an unchanged WACC of 6.7% and terminal growth rate of 3.5%. We see Grab as successfully transitioning into a more profitable phase, with its super-app strategy delivering scale efficiently.

Meta Platforms Inc – Ad business continues to pay off AI spending

Recommendation: ACCUMULATE; TP US$830.00; Last close: US$; Analyst Serena Lim Yi Qi

- 2Q25 results were within our expectations. 1H25 revenue/PATMI was at 46%/59% of our FY25e forecasts due to strong ad revenue growth and resilient operating margin.

- AI continues to drive strong ad results, with better user engagement and ad performance leading to a 9% YoY increase in ad prices and 11% YoY growth in impressions. META AI now exceeds 1bn monthly active users (MAUs).

- We increase our FY25e total revenue forecast by ~3.5% due to META’s improved ad capabilities, which we expect to boost ad revenue. We maintain our ACCUMULATE rating, while our DCF target price is raised to US$830 (prev. US$720). We believe META’s ongoing investments in AI infrastructure and LLM development will enhance its core product offerings, further strengthening its ad business. We also expect these efforts to present monetisation potential in untapped segments, such as video, Threads, and business messaging.

Microsoft Corp – Cloud services accelerate

Recommendations: ACCUMULATE; TP US$550.00; Last Close: US$524.11; Analyst: Alif Fahmi

- FY25 revenue and PATMI met our expectations at 101% of our forecasts. 4Q25 revenue rose 18% YoY, driven by strength in the Cloud services business (Azure +39% YoY). PATMI increased by 24% YoY to US$27.2bn due to higher operating leverage.

- For 1Q26e, Microsoft expects revenue to grow by 15% YoY to US$75.3bn, fuelled by a 37% YoY rise in Azure revenue and a 13% YoY increase in Office 365 commercial cloud revenue. Microsoft’s 1Q26e implied operating margin is ~46.6%, flat YoY despite increased CAPEX for AI capacity expansion.

- We maintain our ACCUMULATE recommendation and raise our DCF-based target price to US$550 (from US$480), reflecting a higher terminal growth rate of 4.7% (previously 4.5%) and WACC of 7.2%. We have rolled over to a new year. Microsoft continues to anticipate higher earnings from Azure (+37% YoY), despite facing supply constraints. However, we see upside potential given the backlog of US$368bn (1.3x FY25 revenue).

Spotify Technology S.A.- Strong user growth, but soft guidance

Recommendation: NEUTRAL; TP US$600.00; Last close: US$; Analyst Helena Wang

- Both 2Q25 revenue and adj. PATMI fell short due to execution delays in scaling ad capabilities. 1H25 revenue/adj. PATMI were at 45%/30% of our FY25e forecasts.

- User metrics ramp up to 696mn MAUs (+11% YoY), in line with guidance. Premium subscribers grew in healthy double digits to 276mn (+12% YoY). Margins are improving across both premium and ad-supported. Guidance for 3Q25e, however, remains soft (revenue +5% YoY) due to near-term investments.

- We keep our FY25e revenue assumption unchanged. We decrease FY25e PATMI by 12% to account for the extra social charges after share price strength. Our DCF target price remains unchanged at US$600. We upgraded our recommendation from REDUCE to NEUTRAL due to the recent share price performance. While user and subscriber growth remain robust, lower 3Q25e guidance due to near-term investments —combined with high operating costs and currency drag—has tempered near-term expectations.

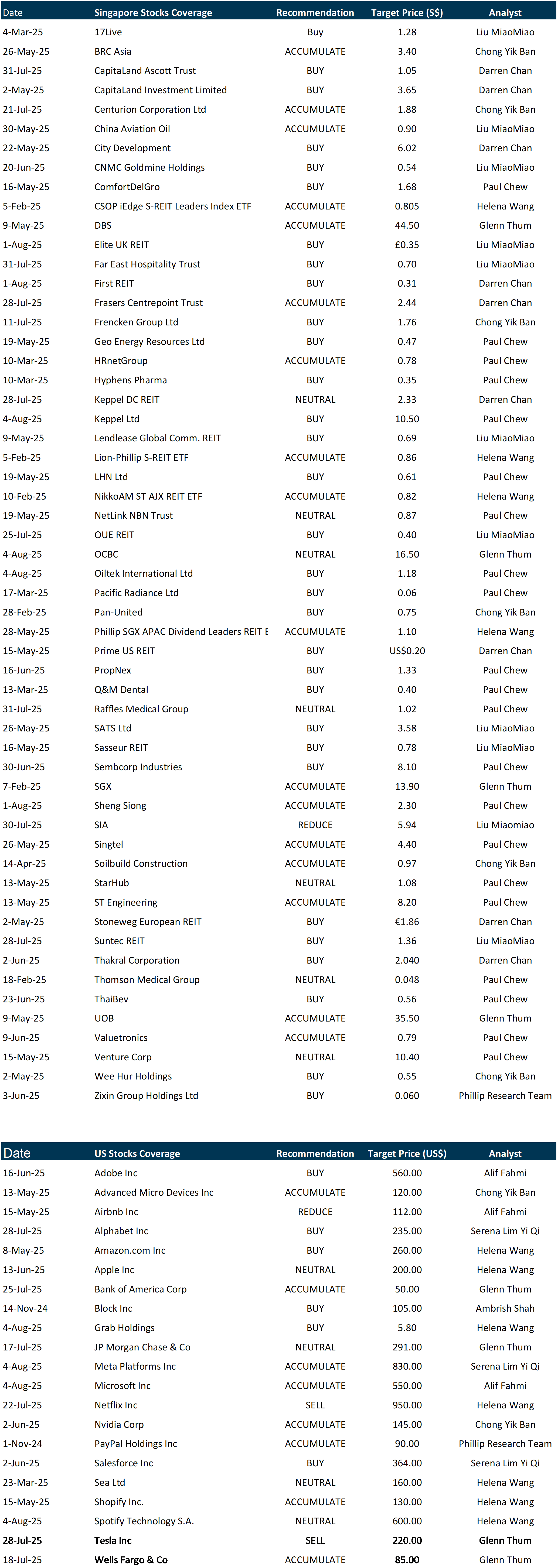

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by BHG Retail REIT

Date & Time: 12 August 25 | 12PM-1PM

Register: poems-20250812-125487

Corporate Insights by Prime US REIT

Date & Time: 13 August 25 | 12PM-1PM

Register: poems-20250813-126111

Corporate Insights by Manulife US REIT

Date & Time: 19 August 25 | 12PM-1PM

Register: poems-20250819-125582

Corporate Insights by Daiwa House Logistic Trust(DHLT) [NEW]

Date & Time: 26 August 25 | 12PM-1PM

Register: poems-20250826-126300

POEMS Podcast:

Research Videos

Weekly Market Outlook: BAC, Tesla, Netflix, OCBC, OUE REIT, Suntec REIT, SG Weekly & More!

Date: 28 July 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials