DAILY MORNING NOTE | 6 October 2025

Recent Podcasts:

Semiconductor 2Q25 Update

Shopify Inc. – Growth momentum to continue, but stock overvalued

Grab Holdings – Super-app strategy delivering scale efficiently

Trade of The Day

ETF Monthly: September 2025 – Most asset classes to extend gains in October

Analyst: Zane Aw

- Review of asset classes performance in September – Most ETFs were in the green except that of tracking Oil (XOP), which was flat. The top gainer was the ETF tracking Gold (GLDM), which surged 11.7%.

- For their current trends, the S&P 500, US Treasury Bonds, Gold, Singapore Equities and Hang Seng Index are in an uptrend. Meanwhile, Oil and Bitcoin are in a range consolidation.

- Heading into October, we expect ETFs tracking the S&P 500, US Treasury Bonds, Bitcoin, Singapore Equities, and the Hang Seng Index to extend their gains from September. Meanwhile, the ETF tracking Oil is expected to continue a sideways consolidation. On the other hand, the ETF tracking Gold could pull back slightly following the recent strong rally.

Trades Initiated in Past Week

Week 41 equity strategy: Our outlook for Singapore equities in 4Q25 is positive. We expect the Singapore market to undergo a meaningful re-rating (of valuations). A telling indicator of its underlying value was the 15-plus privatisations this year alone. Stocks can remain undervalued for extended periods. Crucially is how the value will be realised. We think the ongoing injection of liquidity is a catalyst. There will flows from the initial S$5bn EQDP, EQDP+ involving additional third-party capital to be raised and EQDP plus T (I made this up), to describe the S$5bn or more share buyback from DBS, Singtel and Keppel.

Despite the market reaching record highs, we think it must be viewed in context. From the 2007 peak to current levels, the market has gained only 13% over 17 years. We don’t think such gains suggest speculative excess. Other valuation measures of Singapore equities are at historical averages. We cannot value stocks without taking into account interest rates. The earnings yield (or inverse of P/E ratio) of the market is 7% or 5% points higher than the 2% 10-year bond yield. It is within historical averages. On a forward P/E ratio basis, it is now 14x, which also sits within the historical average of 13.7x. A 1 standard deviation move is 15.7x PE or 13% gain.

In our model portfolio – Phillip Absolute 10 – we added Singtel as we believe the underlying fundamentals of rising mobile prices in key markets such as India and Thailand are intact. Other share price drivers will be the asset monetisation and growth from new data centres and the rollout of GPU-as-a-service. We also added Prime US REIT. We are making the high beta bet of an office market recovery. We expect their occupancy to climb to 90% by 2026. This creates a virtuous snowballing of better cash-flows, higher dividends and rising valuations. We removed PropNex as share prices surpassed our target price. SembCorp was another removal as electricity margins may be weaker than expected.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore stocks wrapped up the week with a series of gains, without a single trading day ending in the red. The local benchmark extended its rally on Oct 3 with an increase of 0.4 per cent or 16.74 points to 4,411.95 – another record high, in tandem with Wall Street’s rally overnight. For the week, the Singapore stocks clocked a 3.4 per cent improvement.

U.S. stocks retreated from a record on Friday but held on to solid weekly gains despite a U.S. government shutdown dragging on for a third day. The broad market index closed little changed, ticking up just 0.01% at 6,715.79, while the Nasdaq Composite declined 0.28% to settle at 22,780.51. The Dow Jones Industrial Average outperformed, trading higher by 238.56 points, or 0.51%, to finish at 46,758.28. The Russell 2000 also popped 0.72% to close at 2,476.18. All four benchmarks had hit all-time highs earlier in the session.

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

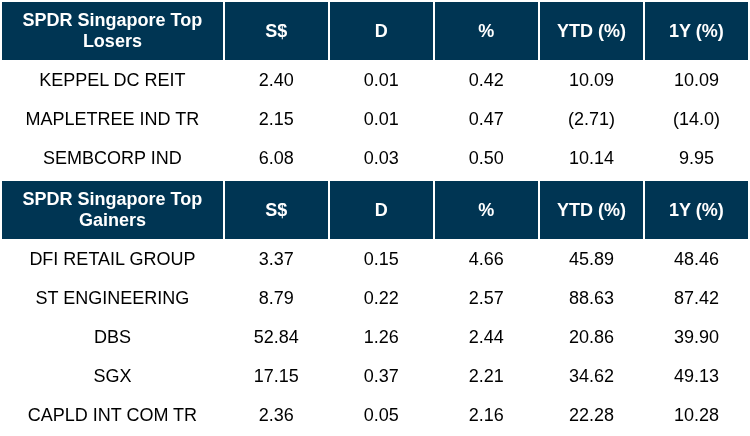

TOP 5 GAINERS & LOSERS

Events Of The Week

SG

Palm oil producer First Resources has disposed of two subsidiaries in Indonesia as it exits the oil palm plantation business in the country’s West Papua province. Following the sale of Permata Putera Mandiri (PPM) and Putera Manunggal Perkasa (PMP) for total cash proceeds of around 405.6 million rupiah (S$31,455), the two have ceased to be subsidiaries of First Resources. The disposals follow the completion of First Resources’ acquisition of Austindo Nusantara Jaya and its decision to streamline its plantation footprint by exiting the oil palm plantation business in West Papua.

The Republic has appointed a consortium led by global asset manager Keppel for the next phase of a project exploring the use of ammonia for clean power generation and bunkering on Jurong Island. Keppel and its partners will conduct a front-end engineering design (Feed) study to advance a proposal using ammonia to generate power. The project aims to develop an end-to-end solution that generates 55 to 65 megawatts of electricity from imported low or zero-carbon ammonia, via direct combustion in a gas turbine plant. It also aims to facilitate ammonia bunkering at a capacity of at least 100,000 tons per annum.

Amid widespread concern over a September emergency hotline outage at Optus which has been linked to three fatalities, Singtel has expressed its commitment to tackling the underlying problems at its wholly-owned Australian subsidiary. A key step is the appointment of global consulting firm Kearney to provide independent additional oversight of the Optus mobile network.

GKE Corporation has completed the share placement of 88.12 million new ordinary shares for 9.68 cents per share, raising gross proceeds of $8.53 million. The share placement of 88.12 million new shares represents about 11.44% of the existing issued share capital of 770.48 million shares and will represent approximately 10.26% of the enlarged issued share capital of 858.60 million shares, excluding 24.22 million treasury shares. The share placement was fully subscribed and attracted interest from institutional investors including ICH Capital, Asdew Acquisitions, and Astral Value Fund VCC, as well as accredited investors.

Fitch Ratings has upgraded Stoneweg European REIT’s long-term issuer default rating to ‘BBB’ from ‘BBB-’, and assigned a stable outlook. Fitch has also upgraded the trusts’ EUR500 million unsecured and unsubordinated six-year notes due Jan 2031 and the EUR1.5 billion medium term note programme to ‘BBB’ from ‘BBB-’.

US

Tesla and General Motors are leading the U.S. automotive industry this year in record domestic sales of all-electric vehicles, as consumers hurried to buy EVs before up to $7,500 in federal incentives for each purchase ended in September. U.S. sales of electric vehicles, excluding hybrids, topped 1 million units through the first nine months of the year. EVs also set a new quarterly record of more than 438,000 units sold during the third quarter — achieving market share of 10.5% for the period.

Applied Materials, the largest US maker of machinery used to manufacture semiconductors, said that an expansion of rules that restrict the export of its products to China will take another chunk out of its revenue. The US Commerce Department’s Bureau of Industry and Security has issued a new rule this week that widens the range of companies subject to export restrictions. The company expects that to cost it US$600 million in lost revenue in fiscal 2026, which runs to next October.

OPEC+ will increase oil production by 137,000 barrels a day in November, matching October’s increase, to regain market share. Brent crude and West Texas Intermediate prices have fallen over 13% this year due to increased production and global supply glut concerns.

Starbucks closed hundreds of stores and laid off thousands of employees following “Project Bloom,” an evaluation of North American profitability and performance. CEO Brian Niccol said the changes were necessary to rebound from six consecutive quarters of declining same-store sales and build toward growth. Signs were posted in closing Starbucks cafes directing customers to other stores. Some company alumni offered assistance to laid-off employees.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

CNMC – Marco tailwind continues to support PATMI

Recommendation: BUY; TP S$1.34; Last close: S$1.1700; Analyst Liu Miaomiao

- Gold prices have rallied c.45% YTD, surpassing USD3,800/oz, supported by sustained central bank purchases, expectations of monetary easing, heightened geopolitical risks, and demand for inflation hedges. We forecast average gold prices of USD 3,500/oz in FY25e (+42% YoY) and USD 3,600/oz in FY26e (+16.6% vs. the previous forecast).

- We expect 2H25 gold production to outperform 1H25 level as CIL facility capacity expanded by 60% since Mar25 and increase the production forecast by 19ppts to +45%YoY. Meanwhile, production of non-gold metals, including zinc, silver, and lead, is anticipated to rise by at least 50% YoY in FY25e. However, selling prices are discounted relative to spot due to the need for further refining. Silver prices have been on an upward trend since the start of the year.

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by UHREIT

Date & Time: 7 October 25 | 12PM-1PM

Register: poems-20251007-130228

Corporate Insights by IREIT Global [NEW]

Date & Time: 22 October 25 | 12PM-1PM

Register: poems-20251022-131424

POEMS Podcast:

Research Videos

Weekly Market Outlook: AppLovin Corp, Micron Tech, TeleChoice, Prime US REIT, Tech Analysis & More!

Date: 29 Sep 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials