DAILY MORNING NOTE | 7 July 2025

Recent Podcasts:

Semiconductor 1Q25 Update – AI demand offsets impact from US export controls

Sea Ltd. – Outperformance likely to continue, but valuations stretched

BRC Asia Ltd – Still record order book

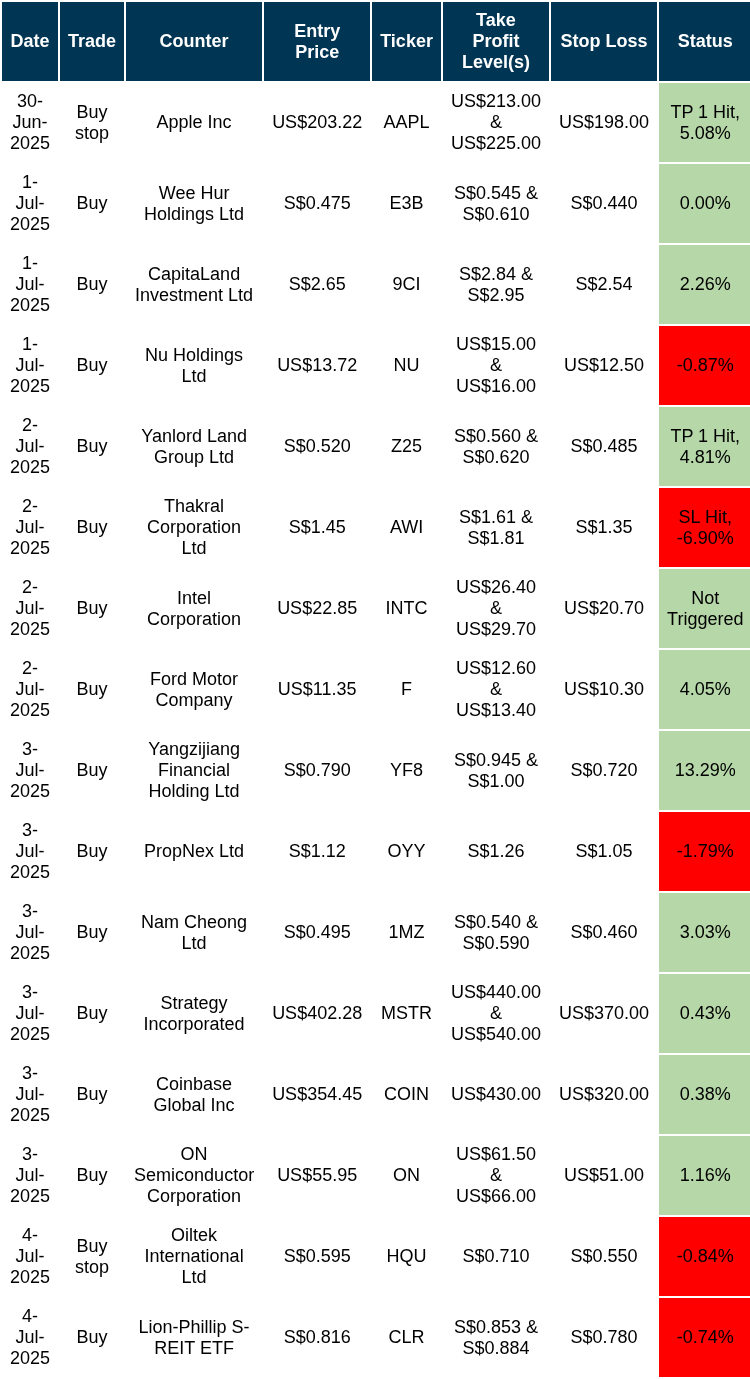

Trades Initiated in Past Week

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

Week 28 equity strategy: We believe the impact from the additional 4% in seller stamp duty (SSD) for sales of residential property within 4 years (i.e. sub-sales) will be marginal. Sub-sales account for 4-5% of total private residential transactions (resale and new). Assuming a 50% impact, it would be 2-3% of total sales. The past three times SSD were introduced (2010) or tighten (2010, 2017), there was immaterial impact to volumes. For new launches sold within four years, sub-sales are around 13%. It is changes to additional buyer stamp duty (ABSD) that materially impacts transactions. We were surprised with this cooling measure. 2Q25 flash only saw a 0.5% rise in property prices. Even on a 12-month basis it is only up 3%, the weakest in 4.5 years. Over 3 years, property prices are up 17%. It is sufficient profit to cover the 4% SSD (now 8%) for properties held between 2 to 3 years. This tweak is to avoid unnecessary speculation, especially ahead of the expected six new launches (2611 units) expected in July. The real gauge of demand will be the new upcoming launched W Residences and Lyndenwoods.

We do not expect this tightening to be a start of more cooling measures. Firstly, as mentioned, prices have not reached double-digit levels where the authorities typically will react. Secondly, we believe property measures cannot be too restrictive and risk hurting developer demand for land sales. Confirmed land sales over the past three years is around 9,800 units. This is double the pre-pandemic average of 4,600 units per year. In 2H25, there are 4,725 units on confirmed GLS. Third, housing demand is driven by a resident population increasing by about 30,000 annually.

There is no change in our BUY recommendations for PropNex and City Developments. Rising HDB prices, falling interest rates and increased population are the foundation for private residential demand. We think City Developments will benefit from loosening of ABSD on foreigners. Lowering foreign ABSD on high-end properties that is outside the usual reach of Singaporean e.g. S$5mn and above looks sensible. We also believe City Developments will undertake more aggressive asset monetisation and narrow its discount to asset value, as reflected by its recent S$834 million sale of South Beach.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore equities retreated along with some regional indexes on Friday (Jul 4) as Asia’s export-driven economies brace for the impact of the upcoming lifting of the pause in implementing the United States’ reciprocal tariffs. The Singapore local benchmark was 0.2% or 5.95 points lower at 4,013.62 as decliners beat gainers 282 to 192 across the broader market, amid transactions of 1.3 billion securities worth S$1.1 billion.

U.S. stock markets were closed on Friday (July 4) in observance of Independence Day.

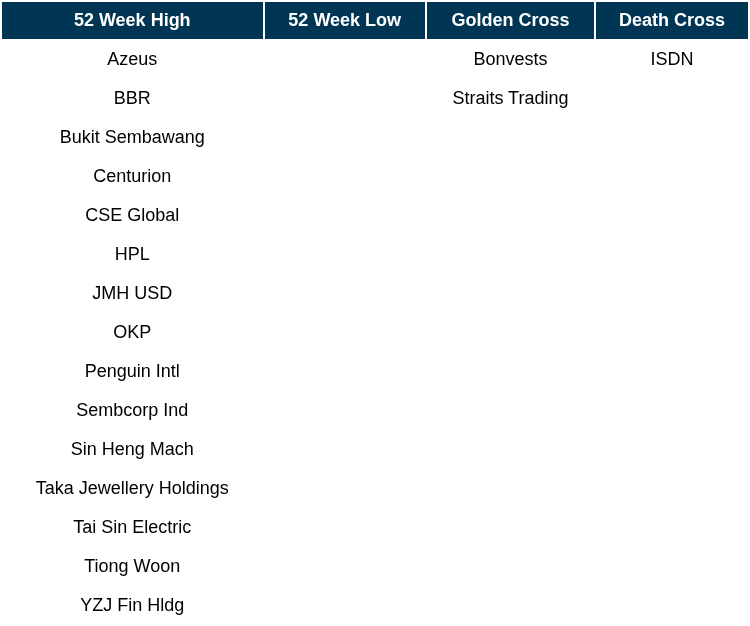

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

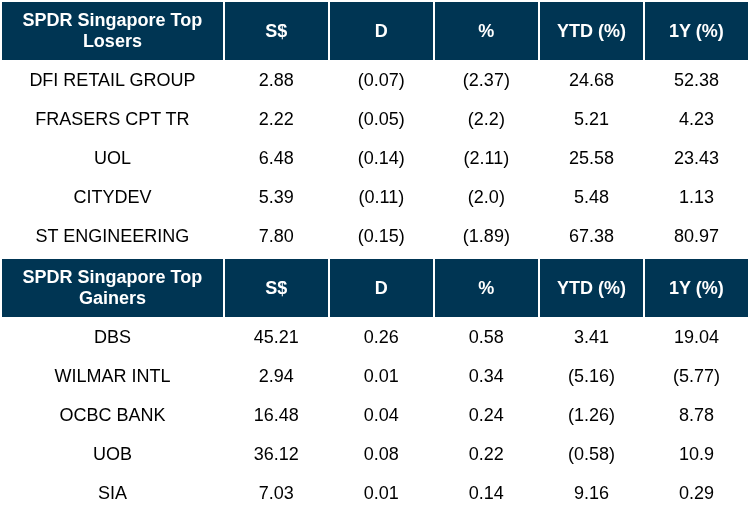

TOP 5 GAINERS & LOSERS

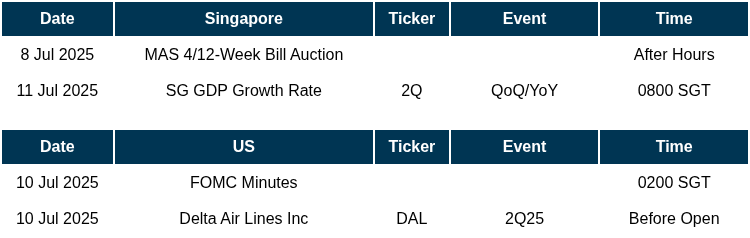

Events Of The Week

SG

Thakral Corporation’s investee company in Australia, GemLife Communities Group, on Thursday (Jul 3) debuted on the Australian Securities Exchange on a conditional and deferred settlement basis. On its first day of trading, GemLife rose 4.1% to A$4.33, logging a market capitalisation of A$1.65 billion (S$1.4 billion), with 9.12 million stapled securities transacted.

Info-Tech Systems, software services provider ended its first trading day at S$0.91 on Friday (Jul 4), 4.6% above its initial public offering (IPO) price. The counter opened at S$0.95 with the stock code ITS, reaching as high as S$0.98 in Singapore’s second listing for 2025 and first mainboard listing in close to two years.

LHN, Real estate player has proposed a voluntary delisting from the mainboard of the Stock Exchange of Hong Kong (HKEX) due to concerns over trading volume and costs. The decision was approved unanimously by its board of directors on Jun 30, the company disclosed in a bourse filing on Friday (Jul 4).

mm2 Asia, the media company which operates the Cathay Cineplexes cinema chain, has proposed the placement of 1,875 million shares at a minimum of S$0.008 per share, to raise funds for debt repayment and working capital. If all the shares are subscribed to at the minimum price, mm2 will raise S$14 million in net proceeds.

Addvalue Technologies has won new orders worth some US$2.1 million from two customers, including one which is new, according to a market filing on July 6. This follows a US$1.46 million order just announced on July 3.

The manager of Keppel REIT has announced the completion of the update of the multicurrency debt issuance programme established on Jan 19, 2009 to increase the limit to $2 billion from $1 billion previously.

Singapore Technologies Engineering (ST Engineering) is supporting small-and medium-sized enterprises (SME) with the launch of its AI-enabled threat elimination and response (AETHER) service at the group’s fourth Cybersecurity Summit on July 4.

The Monetary Authority of Singapore (MAS) has imposed composition penalties amounting to $27.45 million to nine financial institutions (FIs) for breaching the central bank’s anti-money laundering and countering the financing of terrorism (AML/CFT) requirements. United Overseas Bank (UOB) says that it accepts the Monetary Authority of Singapore (MAS)’s decision to impose a penalty of $5.6 million on the bank for its anti-money laundering related breaches.

Top S-Reits with lowest gearing ratios average 33.5% as investors await rate cuts. The sector maintains an average gearing ratio of 40%, reflecting prudent capital management and well below the regulatory limit of 50%.

Nanofilm Technologies International plans to pay $15 million to buy out the 35% stake held by partner Temasek Holdings in a hydrogen-focused joint venture. Sydrogen Energy, as this joint venture is called, was formed in July 2021. Temsaek holds its stake via an entity called Venezio Investments.

US

Treasury Secretary Scott Bessent said President Donald Trump will send letters to some trading partners saying tariffs will boomerang back to April 2 levels on Aug. 1 if there is no progress.

Alphabet’s Google has been hit by an EU antitrust complaint over its AI Overviews from a group of independent publishers, which has also asked for an interim measure to prevent allegedly irreparable harm to them. Google’s AI Overviews are AI-generated summaries that appear above traditional hyperlinks to relevant webpages and are shown to users in more than 100 countries.

Apple, Nvidia supplier Foxconn reports record Q2 revenue on AI demand. Foxconn, which serves as Apple’s biggest iPhone assembler, attributed the strong results to robust demand for AI products, which boosted revenue growth in its cloud and networking products division. The company counts AI chip firm NVIDIA Corporation among its customers.

Deutsche Bank and SeaTown Holdings International are among the lenders providing a US$510 million private credit loan to VinFast Auto. The facility for VinFast, an electric vehicle maker owned by Vietnamese conglomerate Vingroup, pays high-single digit returns.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Singapore Banking Monthly – Loan growth at a 3-year high

Analyst: Glenn Thum

- June’s 3M-SORA was down 14bps MoM to 2.17%, the lowest since Sep 2022 and fell by 150bps YoY. We expect the 3M-SORA to continue declining as Fed rate cuts are expected.

- Singapore loans growth is at a 3-year high (May25: 5.8%), but we expect a slight slowdown due to the trade war. The CASA ratio has continued to rise (May25: 19.2%), which will provide a tailwind for the banks from lowered funding costs.

- Maintain OVERWEIGHT. Despite rate cuts expected at the end of 2025, we believe the banks can maintain NIMs from the steepening yield curve and higher CASA levels. We continue to expect mid-single digit loan growth for FY25e, as the first-order impact from tariffs is minimal (~1-3% of total loans) and the trade war does not directly impact the majority of their customers. The banks’ dividend yield of ~6.5% is attractive, as capital return initiatives are expected to continue in FY25, and share buybacks will improve ROE and EPS. A beneficiary of the trade war has been trading volumes, with YTD 2025 volumes up ~22% YoY.

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by ProsperCap Corporation Limited

Date & Time: 10 July 25 | 12PM-1PM

Register: poems-20250710-123926

Corporate Insights by MoneyHero Group [NEW]

Date & Time: 24 July 25 | 12PM-1PM

Register: poems-20250724-124047

Corporate Insights by Combine Will International Holdings Limited [NEW]

Date & Time: 30 July 25 | 12PM-1PM

Register: poems-20250730-124045

POEMS Podcast:

Research Videos

Weekly Market Outlook: SG & US 2025 Equity Strategy

Date: 30 June 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials