DAILY MORNING NOTE | 7 November 2025

Recent Podcasts:

Semiconductor 2Q25 Update

Shopify Inc. – Growth momentum to continue, but stock overvalued

Grab Holdings – Super-app strategy delivering scale efficiently

Local shares ended Thursday higher, lifted by record gains in DBS and Singtel. The benchmark rose 1.5% or 67.87 points to close at an all-time high of 4,484.99. Singtel was the day’s top blue-chip gainer, rising 5.4% or S$0.23 to close at a record S$4.50. This followed media reports that the local telco and global investment firm KKR & Co are in talks to buy more than 80% of ST Telemedia Global Data Centre.

US stocks closed in negative territory on Thursday, with a resumption of Tuesday’s tech selloff as investors contended with mounting economic uncertainty and stretched valuations. The Dow Jones Industrial Average fell 397.35 points, or 0.84%, to 46,913.65, the S&P 500 lost 75.91 points, or 1.12%, to 6,720.38 and the Nasdaq Composite lost 445.80 points, or 1.90%, to 23,053.99.

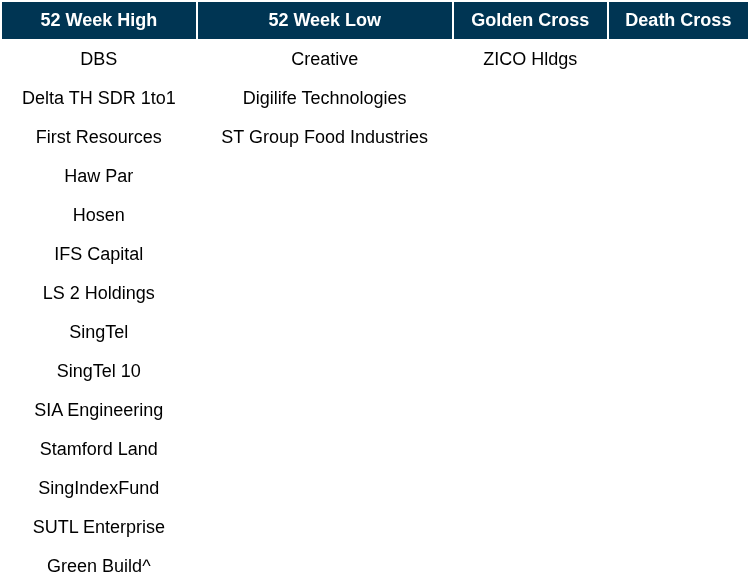

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

TOP 5 GAINERS & LOSERS

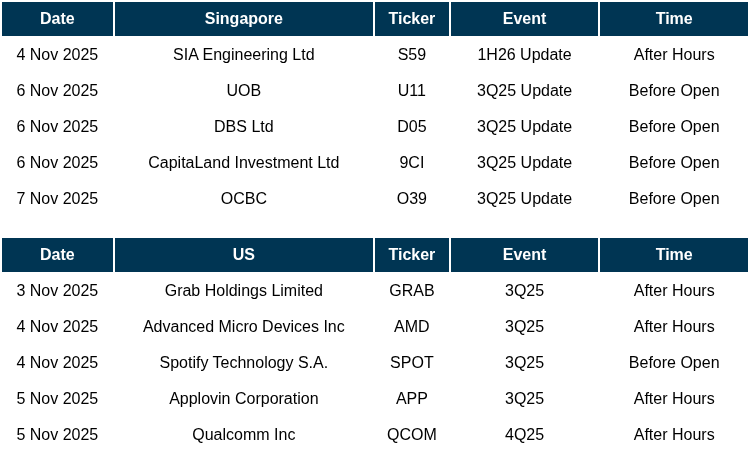

Events Of The Week

SG

OCBC’s 3Q25 earnings of S$1.98bn were slightly above our estimates, with 9M25 earnings at 77% of our FY25e forecast. Net interest income fell 9% YoY to S$2.23bn as NIM contracted by 34bps YoY to 1.84%. Fee income rose 34% YoY from broad based growth on the back of higher customer activities, while trading income inched up 2% YoY. Total allowances declined 18% YoY from lower GPs, and expenses rose 4% resulting in cost-to-income ratio rising to 40% (3Q24: 38.5%). OCBC has lowered their FY25e NIM guidance to 1.90% (prev. 1.90-1.95%) but maintained the remaining guidance of mid-single digit loan growth, CIR in the low 40% and credit costs around 20bps. They have also reiterated their S$2.5bn capital return plan of 60% total dividend payout ratio, combined with share buybacks over a 2-year period.

Glenn Thum

Research Manager

glennthunjc@phillip.com.sg

Oversea-Chinese Banking Corporation (OCBC) has reported group net profit of $1.98 billion for the 3QFY2025 ended Sept 30, 0.2% higher y-o-y. The steady y-o-y performance was supported by higher non-interest income, which grew by 15% y-o-y to $1.57 billion and lower allowances, which fell by 18% y-o-y to $139 million.

CapitaLand Investment (CLI) has reported a 7% y-o-y increase in total revenue for the 9MFY2025 ended Sept 30 of $1,568 million, in its 3QFY2025 business update.

Genting Singapore has reported a net profit of $94.6 million for the 3QFY2025 ended Sept 30, up 19% y-o-y. On a q-o-q basis, net profit grew 5% to $89.8 million.

Far East Orchard has reported net profit after tax of $37.2 million for the 9MFY2025 ended Sept 30, an over 100% y-o-y increase.

Thakral Corporation has reported earnings of $19.5 million for the 3QFY2025 ended Sept 30, a more than fourfold increase from the same period a year ago. Earnings for the 9MFY2025 similarly surged by 767% y-o-y to $128.8 million.

Beng Kuang Marine has reported a profit before tax of $4.52 million for the 3QFY2025 ended Sept 30, up 19.3% y-o-y. For the 9MFY2025, profit before tax declined 11.3% y-o-y to $13.58 million. Beng Kuang Marine awarded new projects worth $15.9 mil, boosting aggregate contract value awarded to $22.1 mil to date.

Investment firm KKR & Co and Singapore Telecommunications (Singtel) are reportedly in advanced talks to buy more than 80% of ST Telemedia Global Data Centres. The S$5 billion deal will give Singtel and KKR full ownership of the Singapore data Centre.

A Singapore Telecommunications Ltd unit offered to sell shares in Indian mobile carrier Bharti Airtel Ltd in a deal that may fetch 103.5 billion rupees (US$1.2 billion), terms of the offering show.

Lendlease Global Commercial REIT (Lendlease REIT) has raised approximately $280 million from a private placement of its units. The exercise was approximately three times covered with strong participation from new and existing unit holders, long-only funds, real estate specialists, private wealth and multi-strategy investors.

Yangzijiang Financial said the plans to pump one billion yuan (S$S$183.1 million) in Ningbo Shanshan’s restructuring will not proceed after creditors of the lithium battery producer rejected the proposed investment.

King Wan Corporation has secured mechanical and electrical (M&E) contracts worth $36.5 million during July to September.

Metro Holdings is divesting its stake in a retail property in Western Australia through its holdings in a portfolio of property holdings, and is set to gain $4.1 million.

Coliwoo Holdings, the coliving business spun off from LHN Group, closed at 58.5 cents on its first day of trading on Nov 6. The company debuted on the mainboard of the Singapore Exchange (SGX) at 61.5 cents, 2.5% above its initial public offering price (IPO) of 60 cents.

Companies such as Bumitama Agri, Genting Singapore, Hong Leong Asia, NTT DC REIT and PropNex have been added to the MSCI Singapore Small Cap Index following MSCI’s review on Nov 5. There were no additions to the MSCI Singapore index, while Genting Singapore was removed.

US

Airbnb issued a better-than-expected outlook for the holiday quarter, citing strong demand as US travelers used its recently launched “reserve now, pay later” feature to book trips in advance.

Apple Inc is planning to pay about US$1 billion a year for an ultrapowerful 1.2 trillion parameter artificial intelligence (AI) model developed by Alphabet Inc’s Google that would help run its long-promised overhaul of the Siri voice assistant.

Tesla Inc. shareholders approved a $1 trillion compensation package for Chief Executive Officer Elon Musk, the largest payout ever awarded to a corporate leader.

Microsoft is forming a new team that wants to build artificial intelligence that is vastly more capable than humans in certain domains, starting with medical diagnostics, the executive leading the effort told.

Amazon.com recovered for most users in the United States on Wednesday. At the peak, more than 6,000 incidents were flagged for Amazon. That number has since dropped below 1,000, indicating a broad restoration of access.

SoftBank Group Corp explored a potential takeover of US chipmaker Marvell Technology Inc earlier this year, in what would have been the semiconductor industry’s largest-ever deal.

OpenAI CEO Sam Altman called on world governments on Thursday to invest in AI infrastructure, as questions grow about whether the ChatGPT-maker, the world’s most valuable private company, can absorb artificial intelligence’s massive costs.

Strong evidence of a cooling labour market rippled through Wall Street, spurring a rally in bonds on bets the Federal Reserve (Fed) will cut rates. Those wagers weren’t enough to lift stocks as megacaps sold off.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

United Overseas Bank Limited – Provisions stockpiling hits earnings

Recommendation: NEUTRAL; TP S$30.40; Last close: S$33.9000; Analyst Glenn Thum

- 3Q25 earnings of S$443mn were below our estimates from higher-than-expected specific provisions and a S$615mn pre-emptive GP. 9M25 PATMI was 56% of our FY25e forecast.

- NII fell 8% YoY from NIM compression of 23bps, while fee income dipped 2% YoY. Allowances surged 348% from higher SPs and pre-emptive GP of S$615mn, which will be a one-off to increase NPA coverage. Credit costs are expected to normalise in 4Q25 and FY26e. UOB has provided FY26e guidance of NIM at 1.75-1.80%, low-single-digit loan growth, high single to double-digit fee income, and credit costs at around 25-30bps. We expect FY25e earnings to decline by ~22%, mainly due to the surge in allowances.

- Maintain NEUTRAL with a lower target price of S$30.40 (prev. S$34.60) as we lower FY25e earnings by ~18% from higher provisions estimate. We assume a 1.08x FY25e P/BV as we lower our ROE estimate to 11.1% (prev. 12.3%) in our GGM valuation. We expect UOB’s FY25e earnings to decline by ~22% YoY from the pre-emptive S$615mn GP set aside. NIM compression to ease in 2H25 as funding costs improve from deposit rate cuts. Fee income will be the most significant driver from the successful integration of Citi portfolios, which will accelerate UOB’s expansion into ASEAN. UOB reaffirmed its capital return plan and will maintain its S$2bn share buyback over three years. The dividend payout will exclude the S$615mn pre-emptive GP, and we estimate a FY25e payout ratio of ~74% (including the 50 cents special dividend), while maintaining their 50% dividend payout ratio guidance in FY26e even if absolute DPS declines YoY.

Phillip Singapore Monthly: November 2025 – No pin for a bubble

Analyst: Paul Chew

- Singapore equities rose 3.0% in October, marking the 6th consecutive month of gains. Banks registered gains of 3.6%. The best performing sector was utilities, led by Keppel Ltd and Sembcorp Industries. News of a major 700MW data centre in Jurong raised optimism over power demand. Company-specific events dragged down the weakest performers. We expect the upcoming deployment of more EQDP funds to drive up small mid-cap valuations.

- Economic indicators are robust in Singapore. Banking liquidity is ample, with bank deposit growth almost tripling from S$60bn to S$171bn over the past 12 months. Loan growth continues to accelerate with a 6.8% increase in September. Property sales are robust, with new home sales jumping 183% YoY in 3Q25. Industrial production bounced back strongly in September, rising 16% YoY.

- Sentiment in global equities remains fragile amid growing concerns that an AI-driven bubble is forming. Future demand from AI applications to justify the capex is hard to pinpoint. However, we believe there is no pin even if there is a possible bubble. Hyperscaler capex is well covered by its operating cash flow, interest rate cuts will further ease funding into AI spending, and Gen AI is a nascent three-year-old technology that is beginning its widespread adoption.

Advanced Micro Devices Inc. – Rising interest from leading AI firms

Recommendation: ACCUMULATE; TP US$280.00; Last close: US$256.33; Analyst Yik Ban Chong (Ben)

- 3Q25 revenue was within our expectations. 3Q25 PATMI exceeded our expectations. 9M25 revenue/PATMI were 70%/88%, respectively, of our FY25e forecasts. PATMI exceeded our expectations due to MI350 GPU’s ramp, and higher ASPs from EPYC CPUs (we estimate ~10% higher).

- MI350 GPUs’ ramp drove data centre (DC) 3Q25 revenue to increase by 22% YoY (2Q25: 14%), despite having no MI308 revenue to China. Adoption of EPYC CPUs is accelerating, gaining market share from Intel (Intel’s DC CPU 3Q25 revenue: -1% YoY).

- We maintain ACCUMULATE with a higher target price of US$280 (prev. US$255). We raised our FY25e PATMI forecasts by 21% due to 3Q25 PATMI outperformance, and an expected margin expansion in 4Q25e from higher ASPs from EPYC CPUs. Our FY25e revenue forecast is unchanged. We lowered WACC to 7.1% (prev. 7.2%) due to lower risk-free rate in the lower interest rate environment. AMD trades at a one-year forward P/E of 53x, compared to its peers’ average of 47x.

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Prime US REIT [NEW]

Date & Time: 12 November 25 | 12.30PM-1.30PM

Register: poems-20251112-132944

Corporate Insights by Wee Hur Holdings [NEW]

Date & Time: 10 December 25 | 12PM-1PM

Register: poems-20251210-133186

Corporate Insights by Marco Polo Marine [NEW]

Date & Time: 11 December 25 | 12PM-1PM

Register: poems-20251211-133188

POEMS Podcast:

Research Videos

Weekly Market Outlook: Tesla, META, Alphabet, AMZN, SSG, Keppel Ltd, Tech Analysis, SG Weekly & More

Date: 3 Nov 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials