DAILY MORNING NOTE | 8 February 2023

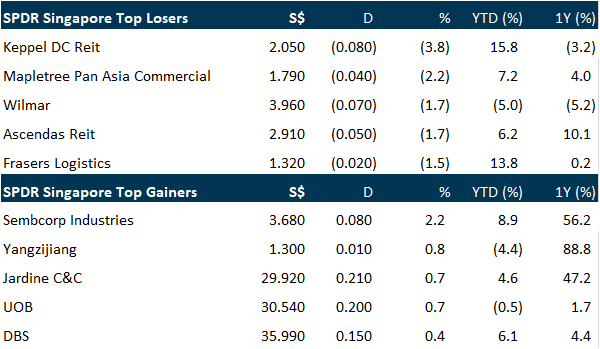

Local shares pulled back on Tuesday (Feb 7) as investor sentiment took a hit from the usual suspects – possible interest-rate hikes by the US Federal Reserve, inflation and worsening US-China ties. The benchmark Straits Times Index fell 0.2 per cent or 5.09 points to end the trading session at 3,380.84. Haw Par Corp was the biggest gainer by value on the Singapore Exchange on Tuesday, rising 2.3 per cent or S$0.23 to S$10.16. Palm oil player First Resources was also among the top advancers, adding 6.6 per cent or S$0.10 to S$1.62. Two of the three local lenders also came in among Tuesday’s top gainers. UOB added 0.7 per cent or S$0.20 to S$30.54, while DBS rose 0.4 per cent or S$0.15 to S$35.99. OCBC inched up 0.2 per cent or S$0.02 to S$13.02. Jardine Matheson Holdings was the biggest loser for the day, shedding 1.2 per cent or US$0.67 to US$53.24.

Product announcements by Google and Microsoft helped lift tech shares on Tuesday, while stocks finished a volatile session decisively higher after fresh Federal Reserve comments viewed as muted on inflation. The Dow Jones Industrial Average rose 0.8 per cent to 34,156.69. The broad-based S&P 500 climbed 1.3 per cent to 4,164.00, while the tech-rich Nasdaq Composite Index gained 1.9 per cent to 12,113.79. The rally comes ahead of President Joe Biden’s annual State of the Union address, at which he is expected to highlight the robust jobs market and progress in mitigating inflation.

Top gainers & losers

SG

Hutchison Port Holdings Trust (HPH Trust) reported on Tuesday (Feb 7) a distribution per unit of HK$0.08 for its second half ended Dec 31, 2022, unchanged from the same period a year ago. This takes its DPU for the full year to HK$0.145, also unchanged from the previous financial year, HPH Trust said in a bourse filing. Revenue and other income for the full financial year fell 8.1 per cent to HK$12.2 billion (S$2.1 billion), while total operating expenses climbed 0.3 per cent to HK$7.9 billion. This resulted in operating profit falling 20.4 per cent to HK$4.3 billion. Net profit for the full year dropped 37.1 per cent on year to HK$1.1 billion, from HK$1.7 billion in FY21. On a per-unit basis, earnings fell to HK$0.1262 in FY22, from HK$0.2006 in FY21. HPH Trust noted that 2022 full-year throughput of its ports was 7 per cent below the previous year. It also said it experienced “challenging business conditions” in the second half of 2022.

Comment: FY22 dividend is unchanged at 14.50 HK cents (1.9 US cents), or a yield of 9%. The yield is attractive and likely sustainable. Firstly, the trust is guiding 14-15 HK cents dividend for FY23. Secondly, the current 14.5 cents dividend (or around HK$1.3bn payout) is well covered from free-cash flows (FCF) of HK$5.5bn. The balance FCF is to repay debt by HK$2bn and HK$1-2bn dividend to non-controlling interests. Net debt has shrunk to HK$17bn, as HK$1bn-2bn annual repayment is underway. Thirdly, the outlook in 1H23 is challenging due to higher volumes a year ago, storage income and government grants. 2H23 is expected to recover strongly as US retail replenishes inventory and the China re-opening is in full swing.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Starhub posted a 98.4 per cent fall in net profit to S$1.3 million for the second half of the year ended Dec 31, 2022, from S$81.4 million a year earlier. This was despite a rise in revenue of 18.7 per cent to S$1.3 billion, from S$1.1 billion the year before. At its earnings briefing on Tuesday (Feb 7), the telco said this came on the back of lower profit from operations, including provisions for the company’s Dare+ transformation initiatives. Dare+ is a five-year transformation plan that includes the establishment of StarHub’s 5G network and other IT expenditures.

The manager of Lendlease Global Commercial Reit (L-Reit) posted distribution per unit (DPU) of S$0.0245 for the first half FY2023 ended December 2022, up 2.1 per cent from S$0.024 in the corresponding period a year ago. Distributable income rose 95.9 per cent to S$56 million, from S$28.6 million in the previous year. Gross revenue more than doubled to S$101.7 million in H1 FY2023, from S$39.2 million in H1 FY2022. Net property income surged to S$76.4 million, from S$29.6 million. The DPU for H1 will be paid out on Mar 30. Committed occupancy rate at L-Reit’s retail portfolio stood at 99.5 per cent as at Dec 31, 2022, with a positive retail rental reversion of about 2 per cent for the period.

Catalist-listed Oiltek International has secured a new contract worth RM19.4 million (S$6 million) from Indonesia. The new contract involves a turnkey project for the construction, fabrication and installation of inside-battery-limits for a new downstream processing plant. With the new contract, the company’s current order book is approximately RM229.3 million and is expected to be fulfilled over the next 18 to 24 months. The new contract is expected to have a positive impact on the financial performance of the company for the financial year ending Dec 31.

Yanlord Land Group Limited announced the unaudited key operating figures for January 2023. In January 2023 and for the month ended 31 January 2023, the Group together with its joint ventures and associates’ total contracted pre-sales from residential and commercial units, and car parks amounted to approximately RMB905 million on contracted gross floor area (“GFA”) of 31,402 square metres (“sqm”), a decrease of 90.8% and 81.6% respectively compared to the corresponding period of 2022. In addition, a total of approximately RMB2.779 billion of subscription sales of the Group together with its joint ventures and associates was recorded as at 31 January 2023 and is expected to be subsequently turned into property contracted pre-sales in the following months. Total contracted pre-sales of other property development projects under the Group’s project management business bearing the “Yanlord” brand name was approximately RMB53 million on contracted GFA of 10,075 sqm.

United Overseas Insurance (UOI), the general insurance arm of UOB, on Tuesday (Feb 7) posted a 36.9 per cent drop in net profit to S$16.7 million for the financial year ended Dec 31, 2022. This follows a 19.4 per cent decrease in net profit for the second half of FY2022 to S$12.1 million, according to its financial statement. Gross premium for the full year rose 1.6 per cent to S$99 million on the back of employers’ liability, marine classes of insurance and inward reinsurance, UOI said. H2 gross premium also grew at the same rate of 1.6 per cent to S$40.8 million. Underwriting profit grew 2 per cent to S$21.2 million for the full year, while H2 saw a 2.3 per cent decrease. Both gross premium and underwriting profit are below pre-Covid-19 levels. Non-underwriting income plunged 94.9 per cent to S$618,000 for the full year, while H2 posted a 39.1 per cent drop to S$3.9 million.

Mainboard-listed drinks maker Fraser and Neave (F&N) reported on Tuesday (Feb 7) a 28.8 per cent year-on-year decline in net profit for its first quarter despite higher revenue. Net profit for the three months ended Dec 31, 2022 fell to S$28.6 million from S$40.2 million in the corresponding period a year earlier, the company said in a business update filing on the Singapore Exchange. On a per-share basis, earnings fell to S$0.02 in Q1 FY23 from S$0.028 in Q1 FY22.

US

BP reported on Tuesday (Feb 7) a record profit of US$28 billion in 2022, lifted by a surge in energy prices since Russia’s invasion of Ukraine, as the company increased its dividend by 10 per cent in a sign of confidence in the market’s continued strength. BP’s fourth-quarter underlying replacement cost profit, the company’s definition of net income, reached US$4.8 billion, compared with forecasts of a US$5 billion profit in a company-provided survey of analysts. The results were impacted by weaker gas trading activity after an “exceptional” third quarter, higher refinery maintenance and lower oil and gas prices. The company also announced plans to repurchase US$2.75 billion of shares over the next three months after buying US$11.7 billion in 2022.

Google said on Monday it will release a conversational chatbot named Bard, launching a rivalry with Microsoft that has invested billions of dollars in the creators of ChatGPT, a language AI app that convincingly mimics human writing. In his blog post on Monday, Google CEO Sundar Pichai said that Google’s Bard conversational AI was to go out for testing with a plan to make it more widely available to the public “in the coming weeks.” Google’s Bard is based on LaMDA, the firm’s Language Model for Dialogue Applications system, and has been in development for several years. “Bard seeks to combine the breadth of the world’s knowledge with the power, intelligence, and creativity of our large language models,” Pichai said, referring to the technology behind ChatGPT-like AI. “It draws on information from the web to provide fresh, high-quality responses,” he added.

Goldman Sachs Group raised US$5.2 billion for a private equity fund that will buy early-stage companies that are typically small, a sign of confidence in an industry that’s confronting strong headwinds. Goldman Asset Management’s West Street Global Growth Partners I exceeded its initial target and received US$3.7 billion from institutional and high net worth investors, according to a statement on Tuesday (Feb 7). It also got a significant commitment from the firm and its staff, it said. The fund targets enterprise and financial technology, as well as the healthcare and consumer sectors, where the pace of innovation “shows no sign of abating,” Julian Salisbury, Goldman’s chief investment officer for asset & wealth management, said in the statement.

Bed Bath & Beyond is making a last-ditch effort to avoid bankruptcy by turning to the public markets for new cash. The retailer, which has been preparing for a Chapter 11 bankruptcy filing, will issue convertible preferred securities and warrants, it said in a statement on Monday (Feb 6). The company plans to raise more than US$1 billion from the offerings. It will use proceeds from the sale, along with a draw on a credit line, to repay debt due under its asset-based loan, according to the statement. It will also make overdue interest payments on some of its debt.

Boeing expects to slash about 2,000 white-collar jobs this year in finance and human resources through a combination of attrition and layoffs, the planemaker confirmed to Seattle Times newspaper on Monday. Last month, the Virginia-based company announced it would hire 10,000 workers in 2023, but some support positions would be cut. Back then Boeing acknowledged it will “lower staffing within some support functions” – a move meant to enable it to better align resources to support current products and technology development.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, PSR

RESEARCH REPORTS

Alphabet Inc. – Focusing on reducing expense base

Recommendation : BUY (Maintained); TP: US$131.00, Last Close: US$107.64

Analyst: Jonathan Woo

– 4Q22 results was within expectations on both revenue and earnings. FY22 revenue/PATMI is at 99%/95% of our FY22e forecasts. Adj. PATMI (excl. unrealised losses) is at 100% of our forecasts. Revenue was dragged by 2% YoY decline in ad revenue, and 6% FX headwinds.

– Cloud momentum is still strong with 32% YoY growth for 4Q22. But there was a -US$480mn operating loss. Cloud accounts for only 10% of total revenue.

– Slowing FY23e expenses growth with 12,000 job cuts in 1Q23e, reducing office facilities, and more prudent investments. Guidance for FY23e CAPEX is roughly in line with FY22

– We cut our FY23e revenue forecast by 9% to account for continued weakness in digital advertising demand, while reducing CAPEX spend by 20% to reflect a general slowdown in expenses. Our FY23e EBITDA forecasts are also cut by 17% to reflect slower-than- anticipated margin expansion due to expected US$2.3bn severance-related charges. We maintain BUY with a raised DCF target price of US$131.00 (prev. US$124.00) due to potential upside from increasing YouTube Shorts monetisation, continued strength in Cloud, and margin expansion in FY24e from the slowing pace of expense growth as a % of revenue, with a WACC of 7.3% and terminal growth of 3.5%.

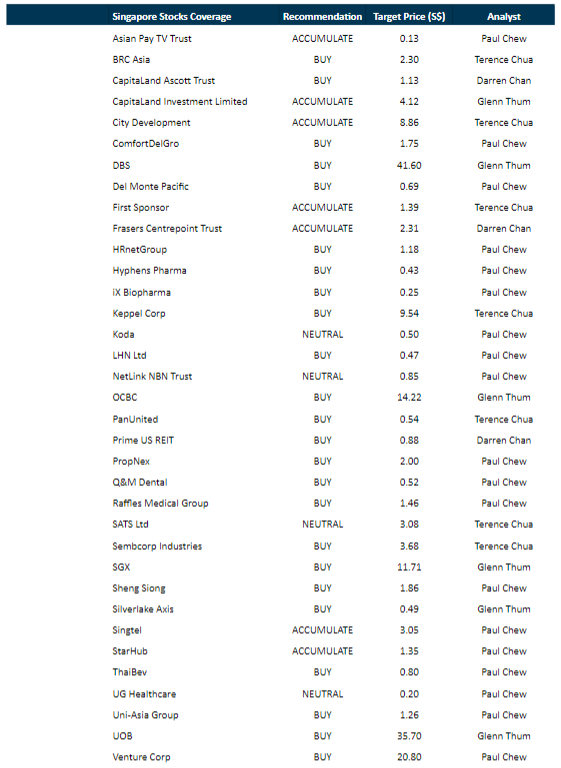

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Guest Presentation by LMS Compliance [NEW]

Date: 8 February 2023

Time: 12pm – 1pm

Register: https://bit.ly/3IX0pAr

Guest Presentation by Prime US REIT [NEW]

Date: 9 February 2023

Time: 1pm – 2pm

Register: http://bit.ly/3HmEzUI

Guest Presentation by Paragon REIT [NEW]

Date: 17 February 2023

Time: 12pm – 1pm

Register: https://bit.ly/3ZNn4W0

Guest Presentation by Keppel DC REIT [NEW]

Date: 17 February 2023

Time: 3pm – 4pm

Register: https://bit.ly/3CYgrGr

Guest Presentation by First REIT Management Limited [NEW]

Date: 23 February 2023

Time: 12pm – 1pm

Register: https://bit.ly/3GY2tp8

POEMS Podcast:

Research Videos

Weekly Market Outlook: Spotify, Apple Inc, SG Banking Monthly, Technical Analysis, SG Weekly & More

Date: 6 February 2023

Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Phillip Research in 3 minutes: #29 Keppel Corporation; Initiation

Click here for more on Phillip in 3 mins.

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials