DAILY MORNING NOTE | 9 March 2026

Recent Podcasts:

Advanced Micro Devices Inc. – Clear Instinct GPU roadmap, strong CPU demand

Netflix Inc. – Content, ads, and scale drive the next leg of growth

The Walt Disney Company – Streaming Turns Profitable

Week 11 equity strategy – The worst-case scenario is panning out in the Iran war or “major combat operation”. The Straits of Hormuz is closed, evidently not by Iranian direct strikes but insurance companies. Energy markets are rattled with Brent crude up 28%, US gasoline 21% and jet fuel 71% this week. Tanker shipping rates have also jumped 54%. Asian economies will be negatively impact with a crude oil reliance from the Gulf as much as 90% for Japan. Even semiconductors face production issues, as 30% of global helium comes from the Gulf. President Trump has not shown concern about rising oil prices. The likely path is that the situation will get worse as more countries will slow or shut production, like Iraq, due to insufficient storage space. The next phase of the war could be further destruction of Saudi Arabian production facilities and regional desalination plants. This will make the Middle East energy disruption more permanent.

The tactical trades or hedges of a worsening tail risk include oil and gas service providers (Pacific Radiance, Marco Polo Marine), shipyards (Seatrium, Yangzijiang Shipping), equipment makers (Nordic Group), rig owners (Keppel), tanker owners (Yangzijiang Maritime), gas trading (Sembcorp Ind) and commodity producers (Geo Energy, CNMC Goldmine). Even SGX can ride on the spike in volatility as daily volume surges past S$3bn. The structural winner will be defence contractors such as ST Engineering, where the Middle East is its key international market. Finally, we think it will be precarious to be excessively bearish. The US administration could declare a victory overnight with a single tweet saying it has destroyed the Iranian missile, navy and nuclear programme. Thank you for your attention to this matter.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore stocks finished flattish despite ongoing Middle East conflict. The Benchmark Index edged up 0.03% to close at 4,848.25, still down 2.9% for the week. The iEdge Singapore Next 50 Index outperformed, gaining 0.7% to 1,450.97.

US market slid as weak jobs data and a 12% surge in oil prices rattled markets. The Dow dropped 0.95% to 47,501.55, its worst weekly fall since April 2025. The S&P 500 shed 1.33% to 6,740, while the Nasdaq lost 1.59% to 22,387.68.

Singapore Technical Highlights

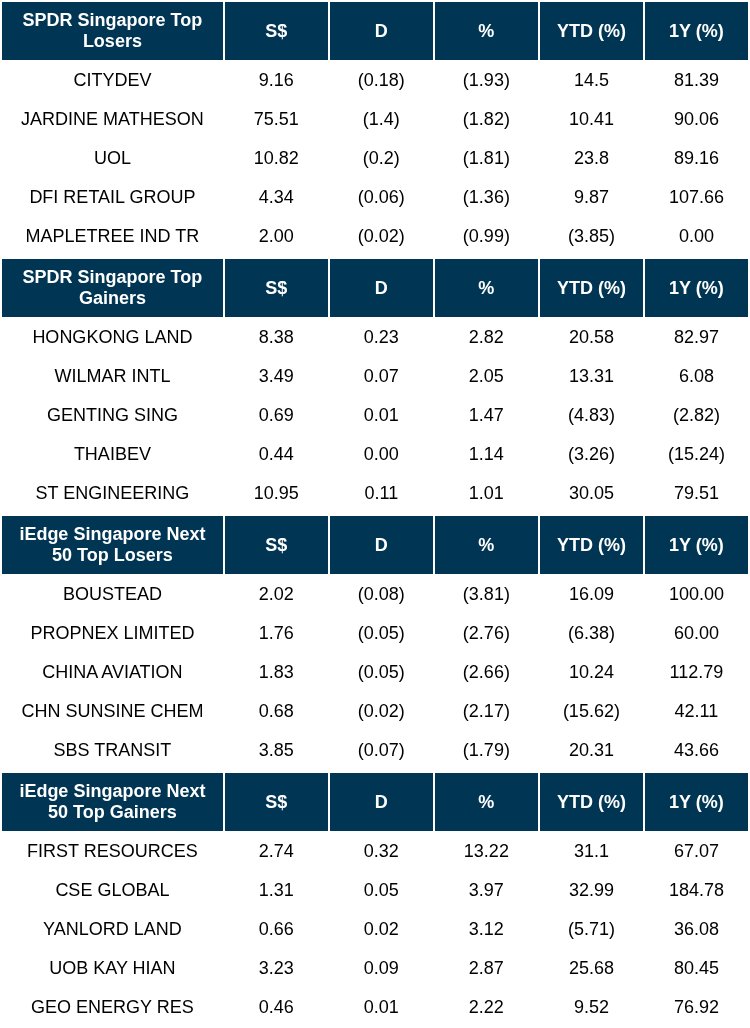

TOP 5 GAINERS & LOSERS

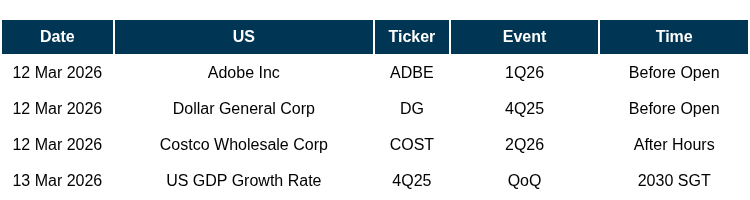

Events Of The Week

SG

Beng Kuang Marine has received in-principle approval from SGX-ST to list up to 15.6 million new shares at S$0.32 apiece, raising up to S$5 million. The placement remains subject to SGX listing requirements and is not yet completed.

OKP Holdings has secured an S$87.3 million contract from the Land Transport Authority to design and build covered linkways, cycling paths, footpaths and roadworks around upcoming Jurong Region Line stations.

Mapletree Investments has acquired Park 15, a 30,817 sq m logistics facility in the Netherlands’ Arnhem-Nijmegen region, following a forward purchase agreement with VDG Real Estate signed in January 2025.

OxPay Financial has partnered with Liquid Group to integrate its RoamQR framework into OxPay’s platform, broadening QR wallet acceptance for merchants.

GuocoLand’s River Modern sold 90% of its 455 units on launch weekend at an average S$3,266 psf, with prices ranging from S$1.5M to S$6.7M.

UI Boustead Real Estate Investment Trust has launched 2026’s largest IPO to date, raising S$973.6 million at 88 cents per unit. The SGX mainboard listing,the first REIT IPO this year, opens March 5 and closes March 10. Trading begins from 12 March.

US

SoftBank is exploring a 12-month, $40 billion bridge loan, potentially its largest-ever US dollar facility, to finance its growing OpenAI investment. JPMorgan is among four banks set to underwrite the deal.

Blue Owl carries £36 million in exposure to Century Capital Partners, a London bridging lender that became insolvent last month. The US private credit firm, which manages $307 billion in assets, had financed the riskiest tranche of Century’s loans.

Oracle and OpenAI have walked away from plans to expand a flagship AI data centre in Texas, citing financing disputes and OpenAI’s shifting requirements. The site was part of the Stargate initiative, a $500 billion, 10-gigawatt project announced by Trump in January 2025.

Oracle is planning broad-based layoffs as early as this month to manage cash pressures from its AI data centre buildout. The cuts span multiple divisions, including cloud hiring, and are expected to exceed the company’s typical rolling reductions.

Robinhood has debuted its RVI-listed venture fund on the NYSE, giving retail investors access to stakes in private companies including Databricks, Ramp and Revolut. This was previously dominated by institutional venture capital.

US retail sales fell 0.2% in January, dragged by weaker auto dealer activity and winter weather disruptions. Excluding autos, sales were flat.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

17LIVE Group Limited – Total dividend of 2.0 Singapore cents

Recommendation: BUY; TP S$1.18; Last close: S$0.8500; Analyst Serena Lim Yi Qi

- 2H25 earnings came in below our expectations, with revenue declining 13.4% YoY to US$77.6mn, mainly due to FX headwinds and flat growth in the live-streaming market. PATMI turnaround to US$3.7mn from a loss of US$5.2mn in 2H24, supported by ongoing cost-optimisation efforts. FY25 revenue met 91% of our forecast, while PATMI missed expectations with a net loss of US$0.9mn, compared with our US$5.48mn profit forecast.

- The company plans to monetise existing assets and diversify revenue streams through initiatives including V-Liver IP, sports collaborations, and short-form drama, which are expected to gradually drive user engagement and revenue growth.

- We maintain our BUY rating but have reduced the target price from S$1.45 to S$1.18. We reduced our FY26e revenue and PATMI forecasts by 25% and 37.5%, respectively, reflecting softer growth assumptions for the live-streaming market, slower monetisation trends, and a longer ramp-up period for new initiatives to contribute meaningfully to earnings. We continue to expect a consistent dividend policy and management’s ongoing share buyback programme. At the current level, 17LIVE trades at an FY26e P/E of 33x.

Ever Glory United Holdings Ltd – Guthrie drives new growth trajectory

Recommendation: BUY; TP S$1.05; Last close: S$0.4000; Analyst Yik Ban Chong (Ben)

- 2H25 revenue/adj. PATMI exceeded our expectations. FY25 revenue/adj. PATMI were at 128%/122% of our FY25 forecasts. Ever Glory realised a S$5.5mn bargain purchase, the excess of net assets’ fair value over the acquisition amount, from the acquisition of Guthrie in 2H25. Excluding the bargain purchase amount, adjusted PATMI spiked 98% YoY, driven by the consolidation of Guthrie’s results.

- Order book surged 135% YoY to S$733mn in 2H25. This was driven by S$508mn in contracts secured in 2025, including a ~S$200mn electrical contract for Alexandra Integrated Hospital redevelopment, maintenance of street lighting, and bus depot facility upgrades. We believe Ever Glory is one of the largest M&E players in Singapore following its acquisition of Guthrie. Guthrie has a strong track record of landmark projects in Singapore, such as runway lightings in Changi Airport. We believe Ever Glory can secure more high-value contracts in the future, such as Changi Airport T5 building and airfield electrical contracts, LTA MRT tunnel lightings, and hospital contracts.

- We upgrade to BUY (prev. ACCUMULATE) with a higher TP of S$1.05 (prev. S$0.81). We raised our TP by rolling forward our model to 18x FY27e PE (prev. blended FY26-27e PE), a 10% discount to its peers’ two-year forward PE of 20x. We forecast Ever Glory’s revenue/adj. PATMI to grow at a CAGR of 25%/36% respectively for the next two years, supported by its record S$733mn order book.

Frencken Group Ltd – Position for the rebound in semiconductor

Recommendation: BUY; TP S$2.50; Last close: S$2.0100; Analyst Yik Ban Chong (Ben)

- 2H25 revenue/PATMI were within our expectations, at 103%/99% of our FY25 forecasts. 2H25 PATMI was stable at +1% YoY to S$19.2mn, driven by a 76% spike in industrial automation revenue but offset by a 12% YoY decline in analytical life science revenue. Demand is sluggish amidst lower research funding in the US.

- We believe the semiconductor segment (2H25 revenue: +1% YoY) will be Frencken’s main growth driver in FY26-27e. We expect orders to pick up gradually and ramp in 2H26e, when its key customer ramps the most advanced lithography machine. TSMC sees increasing demand for AI/HPC and guided a 32% YoY increase in 2026e capex to S$54bn midpoint, with 70-80% of it spent on advanced process technologies. We believe this will drive demand for Frencken’s key semiconductor customers who are high-end equipment makers.

- We maintain BUY with a higher TP of S$2.50 (prev. S$1.87). We roll forward our model, increasing our FY26e revenue/PATMI by 4%/1%. We raised our PE assumptions to 24x FY26e PE (prev. 18x), to be in-line to its peers’ average one-year forward PE of 24x. Frencken trades at an attractive valuation of 20x FY26e PE, an 18% discount to its peers’ average of 24x PE.

Phillip Singapore Monthly: March 2026 – Asymmetric force, Symmetric pain

Analyst: Paul Chew

- The winning streak for Singapore equities continued with a record tenth consecutive month of gains. Equities rose 1.8% in February. Shipyards rebounded on stronger-than-expected results. REITs were the laggards as expectations of interest rate cuts were pushed forward.

- The worst-case scenario from the war or “major combat operation” in Iran is panning out. Straits of Hormuz closure will mean the price of goods globally will rise. Transportation, power, food and even semiconductors are impacted. Emerging markets will bear the larger burden from the surge in inflation.

- The US may have an asymmetric force in the war, but the pain is felt on both sides. An oil price spike and inflation will be a poor backdrop for the upcoming mid-term elections. It is precarious to be excessively bearish. The US administration could overnight declare a victory by damaging the missile, navy and nuclear programme. To hedge any further tail risk, SGX industries that benefit from the current dislocation in markets are oil and gas services, energy producers, power, shipping and exchanges. The longer-term impact is greater self-sufficiency in military capabilities supporting international demand for ST Engineering defence services.

SG Bonds – Week 11 : SGS yields rose WoW

Recommendation: REDUCE; TP S$; Last close: S$; Analyst Phillip Research Team

- UST yields rose across the curve over the week. The 2Y increased 6 bps to 5.60%, the 10Y climbed 22 bps to 4.14%, while the 30Y rose 18 bps to 4.76%. The selloff was driven by the surge in oil prices following the escalation in the Middle East.

- SGS yields were broadly higher over the week, with the 2Y remaining flat WoW, while the 5Y and 10Y rose by around 5 bps each.

- Looking ahead, we expect the Fed to keep rates unchanged at the upcoming March FOMC meeting as labour market conditions remain broadly stable. In the near term, UST yields could remain biased higher as the recent surge in oil prices following the Iran–Israel escalation revives inflation concerns and prompts markets to scale back expectations for Fed easing. Domestically, SGS yields are likely to track movements in global rates but with a smaller movement.

Sea Ltd.- Investment strengthens Shopee’s competitiveness

Recommendation: BUY; TP US$170.00; Last close: US$91.98; Analyst Helena Wang

- 4Q25 revenue was in line with expectations, while PATMI underperformed due to elevated logistics, fulfilment, and user-engagement investments at Shopee. FY25 revenue/PATMI was at 103%/89% of our estimates.

- Revenue grew 38% YoY while PATMI grew 73% YoY, supported by strong Shopee momentum (GMV +29% YoY) with higher ad take rates, rapid loan-book expansion at Monee (+80% YoY), and continued strength at Garena (bookings +24% YoY).

- We maintain our BUY recommendation. We roll forward our valuations to FY26e and reduce our FY26e PATMI by 1% to account for increased investment in e-commerce. Our DCF target price remains unchanged at US$170, with a terminal growth rate of 4.0% and a WACC of 7.6%. Increased investment should further strengthen Shopee’s competitive positioning, supporting GMV growth and higher monetization through ads and commissions.

Market Journal articles powered by PhillipGPT

SIA Engineering Posts Strong Q3 Results on Associate Earnings Growth

Raffles Medical Group Faces Sluggish Growth on Mixed Results

Grab Holdings Achieves First Full Year of Net Profit with Strong Revenue Growth

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Lendlease REIT

Date & Time: 10 March 26 | 12:30PM-1:30PM

Register: poems-20260310-138683

Corporate Insights by Ever Glory

Date & Time: 13 March 26 | 12PM-1PM

Register: poems-20260313-140475

POEMS Podcast:

Research Videos

Weekly Market Outlook: Salesforce, NVDA, UOB, OCBC,REITs monthly,Technical Pulse, SG Weekly & More!

Date: 2 March 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials