Apple Inc - Supply constraints, but demand strong

1 Nov 2021- Full year revenue and PATMI in line at 100%/101% of our FY21 forecasts.

- Elevated freight costs and component shortages guided for the holiday season.

- Maintain BUY with an unchanged target price of US$187.00. Valuations based on DCF with a WACC of 5.8% and terminal growth of 3%. Demand for iPhone, iPad and Mac remain robust. iPhone 13 pre-orders were 20% above the iPhone 12 launched last year. We are estimating 2.8% iPhone sales growth in FY22e. We see potential near-term upside if Apple succeeds in its appeal to delay the App Store ruling coming into effect on 9 December. The ruling allows users in the US to pay outside the App Store, which could negatively impact revenue by 2% or gross profits by 4%.

The Positives

+ Robust iPhone demand. Apple sees strong orders for the iPhone 12 and 13 line up from online and retail stores, carrier channels, and other channels. Upgraders and switchers grew double digits in the quarter. Lead times, a common indicator of demand, are at four weeks for the iPhone 13 Pro and Max, compared to three days for the iPhone 12 Pro Max launched last year, however, this may be skewed by supply constraints. Continued global investments in 5G and aggressive promotions by carriers support the smartphone super cycle story.

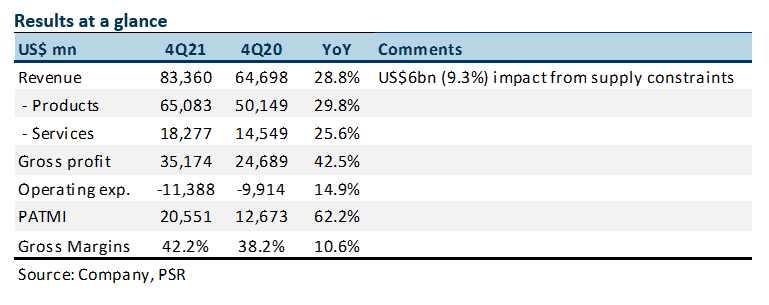

+ Services growth exceeded expectations. 4Q21 services revenue grew 26% YoY to US$18.3bn vs our forecast of 18%. FY21 growth was 27% vs 25% forecast. Growth was broad-based across all services. Higher margins from services of 70% (vs 35% for products) helped push FY21 gross margins to a 7-year high of 41.8%.

The Negatives

– Larger-than-expected supply constraints. US$6bn (9%) impact on 4Q21 revenue from silicon shortages and COVID-19 manufacturing disruptions affecting iPhone, iPad and Mac. COVID-19 disruptions have since eased as Vietnam reopened in late September. The impact from chip shortage will become more acute come holiday season as sales volume spike. Unclear if lost sales during holiday season can be recaptured.

Outlook

1Q22 revenue impact from supply constraints is expected to be higher than US$6bn due to larger product volumes during the holiday season. Despite this, gross margins guidance for 1Q22 is still a material increase YoY from 39.8% to 41.5%-42.5%. The historical five-year average margin is 39%. The margin guidance already factors in significantly higher freight costs and higher cost structures from new product launches.

Keppel DC REIT - DXC settlement offers partial relief from uncollected rents

Keppel DC REIT - DXC settlement offers partial relief from uncollected rents Apr 19th - Things to Know Before the Opening Bell

Apr 19th - Things to Know Before the Opening Bell