ComfortDelGro Corp Ltd - Bottomed out

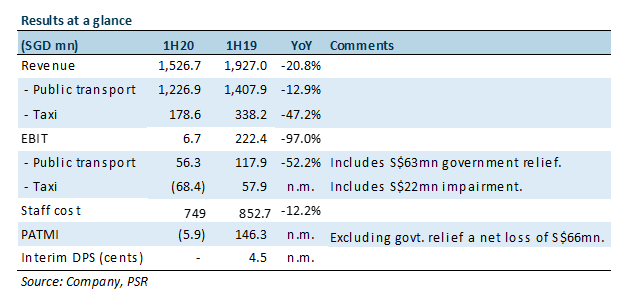

17 Aug 2020- Revenue and PATMI were below expectations. The company suffered a net loss of S$6mn in 1H20 (1H19: +$146.3mn). No interim dividend for 1H20.

- Worst hit segment was taxi operations that swung into S$68mn loss in 1H20 (1H19: +S$57.9mn). Rental rebates and a $22.8mn provision of the diesel taxi fleet were some of the reasons for the loss.

- We were surprised by the large decline in public transport earnings caused by bus operations that do not assume ridership risk and schedules were not severely cut.

- A year to forget but a bottom has likely formed and a recovery is underway, albeit tepid. We are upgrading to ACCUMULATE with a higher target price of S$1.60 (prev: $1.50). Our PATMI for FY20e is slashed by 24% but FY21e forecast is raised 12%. Comfort is our preferred proxy to the easing of lockdown measures compared to the air transport sector. Comfort has a 60% market share of bus and taxi services in Singapore plus a 36% share in the rail network. The high fixed cost of the business can also lead to steeper operating leverage as activity improves.

The Positive

+ Positive operating cash-flows. Despite the net loss, Comfort generated S$214mn of operating cash-flow in 1H20. It reflects the high fixed cost of the business, where annual depreciation is S$450mn per annum and another S$1.7bn staff cost. Government relief of almost S$73mn compensated for some of the loss in revenue.

The Negatives

– Public transport profits also collapsed. As Comfort assumes rail ridership risk, the drop in revenues and profits was expected. We were surprised that bus services profits similarly plunged despite schedules not as severely curtailed as a rail. Bus schedule cut in Singapore was for cross border services into Johor and CDB routes. Bus does not bear ridership risk but the decline in fuel prices affected profits as we believe Comfort earns some margins from the fuel too. Excluding the government relief of S$63mn, 1H20 would be a loss of S$7mn.

– Taxi operations swung to losses. Taxi division incurred a loss of S$68mn in 1H20. We estimate the rental rebates provided by Comfort to its Singapore taxi drivers in 1H20 was around S$80mn. A further hit to the results was an impairment of S$22.8mn for scrapped diesel taxis.

– Interim dividend cancelled. Comfort will not pay an interim dividend due to the losses suffered (1H19: 4.5 cents). We are forecasting a full-year dividend of 2.8 cents, as we expect profitability in 2H20 and cash-flows of the company remain healthy.

Outlook

We believe transport activity has bottomed but recovery will be tepid especially for taxis.

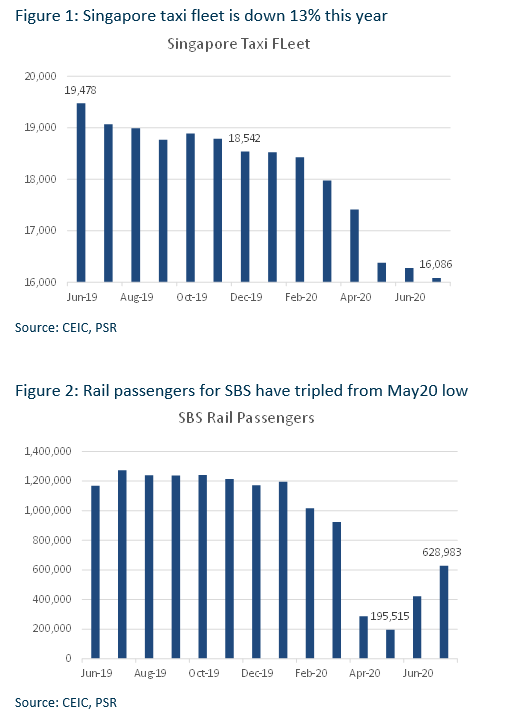

Taxi – Taxi driver earnings are held up currently relief measures from both Comfort and the government. Around 1/3 of taxi driver takings is due to government support measures. Comfort taxi fleet size was around 11,000 in Dec19 (or 60% share). The fleet has declined to 9,000 plus currently. The Singapore taxi fleet is down around 2,456 units (or 13%) this year to 16,086. Whilst details are lacking, Comfort share of taxis is likely maintained around 60%, however, Comfort typically experiences the lowest unhired or utilization rate amongst its peers.

Rail / Bus – Rail traffic is starting to climb back up sharply from the low in May (Figure 2). There are two tenders pending award in Singapore (Bulim by Tower Transit and Sembawang-Yishun by SMRT) that are currently not run by SBS. This will be an opportunity to further grow its current 61% market share in public bus services.

Upgrade to ACCUMULATE with a higher target price of S$1.60 (prev. S$1.50)

We lowered PATMI for FY20e by 24% but this was offset by FY21e forecast being raised by 12%. Comfort enjoys a large market share in rail, taxi and bus services in Singapore. It is our preferred transport proxy as the lockdown eases in Singapore.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Apr 25th - Things to Know Before the Opening Bell

Apr 25th - Things to Know Before the Opening Bell JPMorgan Chase & Co - NII continues to rise, guidance maintained

JPMorgan Chase & Co - NII continues to rise, guidance maintained Trade of the Day - NVIDIA Corporation (NASDAQ: NVDA)

Trade of the Day - NVIDIA Corporation (NASDAQ: NVDA) Trade of the Day - Applied Materials, Inc. (NASDAQ: AMAT)

Trade of the Day - Applied Materials, Inc. (NASDAQ: AMAT)