Uni-Asia Group Ltd - A new and higher plateau

1 Jul 2022- 1Q22 freight rates for Uni-Asia fleet of 10 Handysize dry bulk ships are up 84% YoY to around US$18.4k per day. FY22e PATMI is expected to jump 40% to US$25mn.

- We expect freight rates to remain elevated for the next two years. Supply is constrained by inefficiencies (port congestion and slower speeds), constrained shipyard capacity, and uncertainty on future fuel types due to IMO 2030.

- Initiate coverage on Uni-Asia Group with a BUY rating and a target price of S$1.26. Our target price is pegged to 3x P/E FY22e, in line with industry peers. We believe the tight supply of dry bulkers will keep freight rates elevated for longer. Orders for dry bulkers are at a record low, as a percentage of the order-book. We expect Uni-Asia to pay special dividends from their record earnings.

Company Background

Founded in March 1997, Uni-Asia’s origins were in structured finance and distressed asset investments. The company was listed on the SGX on 17 August 2007. In 2010, the company expanded into ship and property investments. The core businesses of the company are the chartering of bulk carriers, investment properties in Hong Kong and the management and sale of residential projects in Japan. All 10 Uni-Asia bulk carriers are Handysize type vessels.

Investment Merits

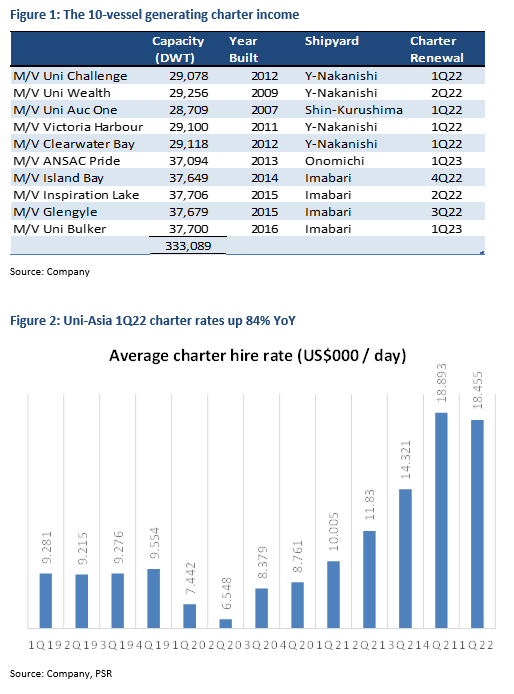

- Record earnings from surging charter rates. Uni-Asia Freight rates in FY21 were averaging US$13k per day. We expect this to jump to around US$18k per day. 1Q22 has seen an 84% spike in freight rates. With a fleet of 10 vessels – 9 of which are due for renewal this year – it can ride on the spike in freight rates. Fuel cost is borne by the shipping operator, and we expect vessel operating costs to rise around US$850 per day or 15% to US$6,000. The increase is due to higher crew costs.

- Supply conditions remain very tight. We believe the current freight rates can sustain for the next two years. The supply of vessels is at record lows of 6.6% of the total fleet. Furthermore, with 11% of the fleet more than 20 years, any new delivery of vessels is likely to replace older ships rather than result in a net expansion in fleet size. Handysize has an even older fleet at 15% above 20 years. The limited number of bulk carriers being ordered is due to uncertainty of the future fuel type for vessels and limited yard capacity due to a surge in container ship orders. Other drivers constraining effective supply are slow steaming of vessels due to high fuel costs and port congestion.

- Stronger balance sheet and higher dividends. With record earnings, we expect Uni-Asia to pay a special dividend of 4 cents, double the amount paid last year. Together with higher interim and final dividend, total dividends in FY22e are expected at 12 cents (FY21: 7 cents) or 11% dividend yield. The payout is around US$13mn, around a 50% payout ratio. Free-cash flow generated totalling US$68mn over the next two years will swing the company into the net cash position by FY23e. The company is trading at a 50% discount to book value.

Phillip Securities Research has received monetary compensation for the production of the report from the entity mentioned in the report.

Revenue

In FY21, 70% of Uni-Asia revenue was charter income. We expect it to jump to 90% in FY22e. The 2nd largest revenue contributor is the sale of properties at 13%. Fee income and investment returns contribute 8% of revenue each.

(i) Charter income: Around 80% of Uni-Asia FY21 PBT comes from charter income. It is the rental of the company’s 10 bulk carriers (Figure 1) to shipping lines. The charters for a fixed period (called time charters) on a fixed daily rate. The smaller vessels are typically chartered out for six months and larger vessels for around a year. New vessels upon delivery tend to be chartered for five years to match the loan tenure. Around nine of the 10 vessels are due for renewal this year (Figure 1) and charter rates have been surging since 1Q21 (Figure 2). The key minor bulk cargo is grains, cement, steel, fertiliser, forest products and coal.

(ii) Sale of properties under development: Revenue is generated from the sale of Alero properties. Gains from the sale of Alero projects were previously recognised as investment gains.

(iii) Fee income: Fee income comes from multiple sources: i) Ship brokerage fee from securing charters for the vessels under management and other third-party customers and sale and purchase of ships.; ii) Project arrangement fees from the arrangement of finance, acquisition, and disposal of properties in Hong Kong and Japan and shipping joint ventures; iii) Asset management fee of Alero property projects in Japan.

(iv) Investment returns: The source of returns are from sales of vessels, fair value gains and gains from the sale of Hong Kong property investments. For FY22e, we expect the bulk of the gains to come from Alero property projects. Sales of Hong Kong properties are expected to be weaker due to the lockdowns still underway.

Expenses

The largest operating cost is voyage expenses to operate the bulk carrier vessels. Around 1/3 of voyage expenses are crew and crew-related costs. Other costs include lubricant oil, consumables, cables, ropes, repairs and maintenance. Fuel cost is not borne by the vessel operator but by the shipping operator. After voyage expenses, the next largest cost is depreciation and amortisation of the vessels. The depreciation period of vessels is around 20 years. Fair valuation above book is implemented for assets in the joint venture.

Margins

Margins are volatile depending on the cycle of the three key businesses. Charter income margins (revenue less voyage expense) have swung from -18% to 57% over the past three years. Maritime services income is stable at around US$0.5mn PBT p.a. Maritime asset management margin is also volatile depending on investment and fair value gains.

Balance Sheet

Assets: Most of the assets in the balance sheet are shipping vessels (59%), which are the 10 bulk tankers. The next largest is cash (16%), investments (14%) and investment properties and properties under development (7%). Investments are predominantly Hong Kong commercial properties. Properties under development are the residential projects in Japan (Alero).

Liabilities: Of the US$98mn in total liabilities, US$84mn or 85% are bank borrowings. The bank borrowings are secured against the vessels and properties. The effective interest rate of the loans ranges from 0.6% to 2.45%, as per FY21. Net borrowings are currently USS$78mn, which is expected to decline to U$47mn with free cash flows (FCF) of US$34mn expected in FY22e.

Cash Flow

FCF generated over the past three years has been strong. Cumulative FCF is US$67mn. Reasons for cash-flows above net profits is due to low CAPEX of only US$2mn p.a. versus depreciation of around US$10mn p.a. We believe there are no plans to purchase vessels in the next two years until there is clarity of the engine type that can meet IMO 2030 regulations. Working capital needs have also been minimal as charters are paid one month in advance.

Business Model

Un-Asia is essentially in 4 core businesses – bulk ship owner, investment properties and management of shipping and property assets for 3rd party. Uni-Asia splits the business into

- Ship owning and chartering: Established in 2010 as Uni-Asia Shipping Ltd, this division build up a portfolio of 10 wholly-owned dry bulk carriers. These 10 sit on the balance sheet of Uni-Asia and property plant and equipment. Revenue is dependent on charter rates and hire days. In FY21, this division enjoyed a major turnaround in earnings from a PBT loss of US$11.2mn to a PBT of US$18.9mn.

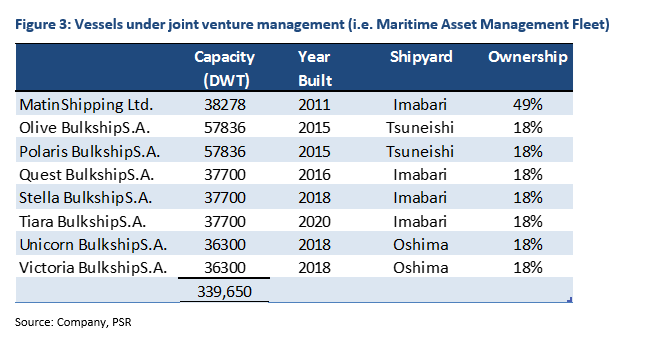

- Maritime asset management: Manage a portfolio of 8 dry bulk carriers with shareholdings of 18% to 49% (Figure 3). The assets are held on the balance sheet as investments. Uni-Asia will charge the joint venture various fees – administration fees (e.g. operating and accounting), acquisition and disposal fees, loan arrangement fees and brokerage fees when leasing out vessels. The equity stake will also allow the company to enjoy dividend income, disposal and fair value gains. Over its 25-year history, this division has arranged more than 140 deals with a total value exceeding US$8bn. The average profit before tax over the past three years has been US$1.5mn per annum.

- Maritime services: The division is operated through subsidiaries Uni Ships and Management Ltd (100%) and Wealth Ocean Ship Management (Shanghai) Co. Ltd (51%). Services provided include commercial/technical management of ships and brokerage services for chartering, sale and purchase of ships. The average profit before tax over the past three years has been US$0.5mn per annum. The appeal of hiring Chinese shipping crew may wane due to rising wages compared to other countries such as the Philippines.

- Property (ex-Japan): Uni-Asia will invest in office buildings in Hong Kong with varying stakes of between 2.5% to 8.3%. It has invested in 8 Hong Kong property projects to date. The first project was in 2010 by partnering developer First Group Holdings Limited in a project at 35 Hung Tung Road. First Group has been the partner in all 8 projects. First Group Holdings will manage and market these projects. The first 3 projects had been completed and generated returns of more than US$20mn. The 4th and 5th projects are ready for sale and the 6th will be ready for sale in 2022. The sale of units in projects have been slow especially due to the lockdown and movement restrictions in Hong Kong.

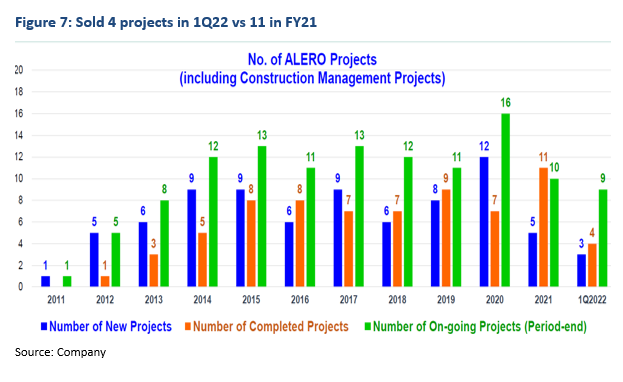

- Property (Japan): Uni-Asia will invest in and develop small residential property projects in Tokyo, named “Alero” Series (Figure 6). The land is purchased and developed into 4-5 storey buildings with 10-30 units of studio or maisonette type flats. Once tenanted the completed projects are typically sold en-bloc. In FY21, 11 Alero projects were sold (Figure 7, number of completed projects) with another 4 sold in 1Q22. The pipeline of new projects of only 3 is the weakest since 2013.

Industry

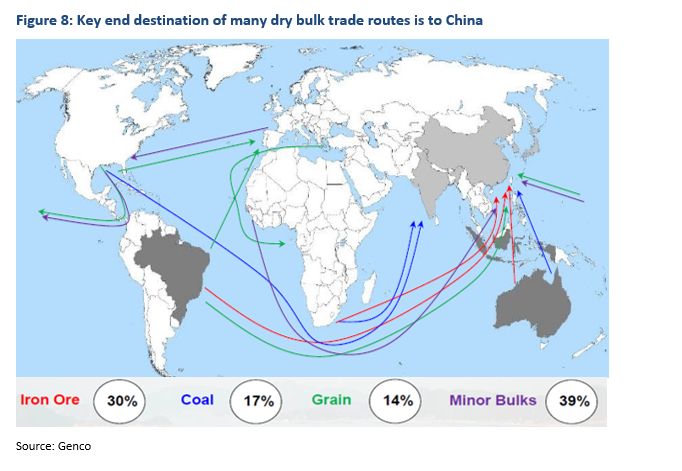

In shipping, dry bulk cargo is almost half of seaborne trade volume (Figure 8). There are around 12,700 dry bulk vessels globally. Dry bulk carriers transport unpackaged bulk cargo, major bulks (iron ore, coal, grains) and minor bulks (fertilizer, cement, sulphur, forest products). Major bulks are around 60% of cargo shipped by tonne-miles. The end destination of many key routes is to China. The key cargo includes the transport of iron ore and grains from Brazil to China and from Australia to China (Figure 8). Dy bulk ship can be separated by DWT capacity (Appendix 1). Uni-Asia 10 vessels are all Handysize, or less than 40k DWT. Above Handysize is the Supramax, Handymax and Ultramax category. We designate all three as Supramax. The 2nd largest category is the Panamax. It refers to the maximum size of a vessel than can transit the Panama Canal. The largest sized bulk carriers are the Capesize. Because they are too large to transit the Panama Canal and need to travel around Cape Horn, South Africa.

The Baltic Dry Index (BDI) enjoyed two major upcycles. The first was in 2004 after China entered the WTO. Then came the super cycle in 2008 following the surge in infrastructure and property projects in China. From 2010, the BDI has been languishing below 2000 to (monthly) lows of 487 in January 2020. Excess supply and slowdown in China were major drivers of the weakness. A significant pick-up in the index occurred in June 2020 due to major supply chain bottlenecks, especially at the ports. The BDI almost quadrupled over five months from 487 in January to 1800 in June 2020.

About the author

Phillip Research Team

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

- recipients of the analyses or reports are to contact Phillip Securities Research (and not the relevant foreign research house) in Singapore at 250 North Bridge Road, #06-00 Raffles City Tower, Singapore 179101, telephone number +65 6533 6001, in respect of any matters arising from, or in connection with, the analyses or reports; and

- to the extent that the analyses or reports are delivered to and intended to be received by any person in Singapore who is not an accredited investor, expert investor or institutional investor, Phillip Securities Research accepts legal responsibility for the contents of the analyses or reports.

About the author

Phillip Research Team

Latest Reports

A-Sonic Aerospace Ltd - Trades below cash with buy backs underway

A-Sonic Aerospace Ltd - Trades below cash with buy backs underway Software Quarterly Update 4Q25 - Fundamentals remain intact

Software Quarterly Update 4Q25 - Fundamentals remain intact 名創優品 (9896.HK) 1-2 月同店超預期高增,有望驅動全年戴維斯雙擊

名創優品 (9896.HK) 1-2 月同店超預期高增,有望驅動全年戴維斯雙擊- MINISO (9896.HK) The strong same-store sales growth in Jan and Feb exceeded expectations, potentially driving a Davis Double Play for the full year