Elite UK REIT, a property investment trust focused on UK commercial real estate, has delivered solid first-quarter performance whilst strengthening its financial position through improved capital management and portfolio revaluation.

Strong Financial Performance Drives Growth

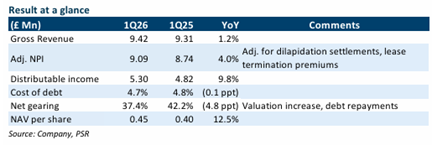

The REIT reported revenue of £9.4 million and adjusted net property income of £9.1 million for 1Q26, representing increases of 1.2% and 4.0% respectively. These figures constitute 25% and 27% of full-year forecasts, indicating steady progress towards annual targets. Distributable income surged 9.8% year-on-year to £5.3 million, driven by positive rental reversions and contributions from three strategic acquisitions completed in FY25: Priory Court, Custom House, and Merlin House.

Capital Management Excellence

The company has demonstrated exceptional capital management capabilities, with net gearing declining significantly by 4.8 percentage points to 37.4% – well within management’s target range of 35-40%. This improvement stems from both portfolio valuation increases and debt reduction through repayment of approximately £14.7 million in revolving credit facilities. Borrowing costs remain stable at 4.7%, with 92% of debt secured at fixed rates, up from 85% in December. The interest coverage ratio maintains a healthy 2.6x, supported by government tenants who typically pay rents three months in advance.

Portfolio Valuation Surge

Portfolio valuation has increased substantially by 9.1% since December to £463.2 million, primarily driven by the Department for Work and Pensions (DWP) lease regear rerating. Notable valuation increases include Peel Park (up £4 million or 10%), Parklands Falkirk (up £2.3 million or 28.3%), and Nutwood House Canterbury (up £1.1 million or 16.2%). The Purpose-Built Student Accommodation conversions have particularly benefited Lindsay House, with valuations rising 41% since December 2024.

Investment Outlook and Recommendation

Phillip Securities Research maintains a BUY recommendation with an unchanged dividend discount model-based target price of S$0.41. The REIT trades at an attractive 9.0% FY26 dividend yield and 0.87x price-to-NAV ratio. With approximately 20% of remaining DWP leases expected to be regeared and potential repositioning or divestment of other assets, Elite UK Reit appears well-positioned for continued value creation.

Frequently Asked Questions

Q: What drove Elite UK REIT's distributable income growth?

A: Distributable income increased 9.8% year-on-year to £5.3 million, driven by positive rental reversions, contributions from three acquisitions (Priory Court, Custom House, Merlin House) completed in FY25, and falling financing costs through debt repayment.

Q: How has the company's gearing position improved?

A: Net gearing declined 4.8 percentage points year-on-year to 37.4%, primarily due to portfolio valuation uplift of £38.6 million since December and repayment of approximately £14.7 million in revolving credit facilities.

Q: What is Phillip Securities Research's recommendation and target price?

A: Phillip Securities Research maintains a BUY rating with an unchanged dividend discount model-based target price of S$0.41.

Q: Which properties showed the strongest valuation increases?

A: Notable increases include Peel Park (up £4 million or 10%), Parklands Falkirk (up £2.3 million or 28.3%), Nutwood House Canterbury (up £1.1 million or 16.2%), and Lindsay House (up 41% since December 2024 due to PBSA conversions).

Q: What is the current dividend yield and trading metrics?

A: Elite UK REIT trades at a 9.0% FY26 dividend yield and a price-to-NAV ratio of 0.87x, with the portfolio asset value exceeding market capitalisation by approximately £252.2 million (119.6%).

Q: How much of the DWP lease portfolio is expected to be regeared?

A: Approximately 20% of the remaining 30% of DWP's leases are expected to be regeared, with remaining assets likely to be repositioned or divested.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.