Exchange-traded funds (ETFs) experienced a challenging March, with most asset classes posting negative returns as market volatility persisted across global markets. However, oil and Bitcoin emerged as notable exceptions, demonstrating resilience amid broader market weakness.

Mixed Performance Across Asset Classes in March

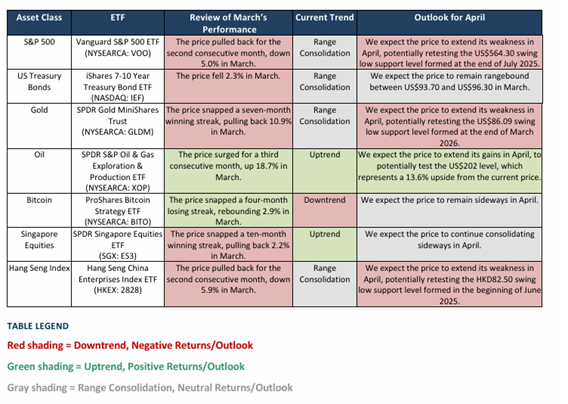

The commodity sector provided the standout performance in March, with the SPDR S&P Oil & Gas Exploration & Production ETF (XOP) surging 18.7% for its third consecutive monthly gain. This impressive rally maintained oil’s uptrend trajectory, positioning it as the clear winner amongst major asset classes.

Bitcoin also bucked the broader negative trend, with the ProShares Bitcoin Strategy ETF (BITO) gaining 2.9% during the month. This positive performance helped snap a four-month losing streak, though the cryptocurrency remains in a broader downtrend pattern.

Conversely, precious metals faced significant headwinds, with the SPDR Gold MiniShares Trust (GLDM) tumbling 10.9% in March. This sharp decline snapped a seven-month winning streak for gold, marking it as the month’s worst performer.

Traditional equity markets also struggled, with the Vanguard S&P 500 ETF (VOO) declining 5.0% for its second consecutive monthly retreat. Similarly, the Hang Seng China Enterprises Index ETF fell 5.9%, extending its weakness into a second consecutive month.

Outlook for April Points to Continued Oil Strength

Looking ahead to April, technical analysis suggests oil is positioned to extend its outperformance relative to other asset classes. The oil ETF is expected to continue its upward momentum, with potential to test the US$202 level, representing a 13.6% upside from current prices.

Meanwhile, several asset classes are expected to face continued pressure. Both the S&P 500 and gold ETFs are anticipated to extend their March weakness, with potential retests of key support levels. The S&P 500 ETF may challenge the US$464.30 swing low established in July 2025, whilst gold could retest the US$86.09 support level formed in March 2026.

Other asset classes, including US Treasury bonds, Bitcoin, and Singapore equities, are expected to remain rangebound in April, trading within established consolidation patterns as markets await clearer directional catalysts.

Frequently Asked Questions

Q: Which ETF performed best in March?

A: The SPDR S&P Oil & Gas Exploration & Production ETF (XOP) was the top performer, surging 18.7% for its third consecutive monthly gain.

Q: What was the worst-performing asset class in March?

A: Gold was the worst performer, with the SPDR Gold MiniShares Trust (GLDM) tumbling 10.9%, snapping a seven-month winning streak.

Q: Which asset class is expected to continue outperforming in April?

A: Oil is expected to continue outperforming other asset classes in April, with potential to test the US$202 level representing a 13.6% upside.

Q: What is the outlook for Bitcoin in April?

A: Bitcoin is expected to remain rangebound in April despite gaining 2.9% in March and snapping a four-month losing streak.

Q: How did US equities perform in March?

A: US equities struggled, with the S&P 500 ETF declining 5.0% for its second consecutive monthly retreat and entering a range consolidation pattern.

Q: What support levels are being watched for major indices?

A: The S&P 500 ETF may test the US$464.30 swing low from July 2025, while gold could retest the $86.09 support level formed in March 2026.

Q: Which asset classes are expected to remain sideways in April?

A: US Treasury bonds, Bitcoin, and Singapore equities are all expected to remain rangebound in April, trading within established consolidation patterns.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.