Sector Performance Driven by Memory Boom and AI Infrastructure Demand

The semiconductor sector continues to demonstrate robust growth momentum, with the Semiconductor ETF surging 39.9% over the past three months, significantly outperforming the S&P 500’s 11.4% gain. Memory companies have emerged as the standout performers, posting exceptional gains of 95% driven by extraordinary first-quarter 2026 earnings growth exceeding 900% year-on-year. This remarkable performance stems from a substantial surge in DRAM and NAND prices amid widespread memory chip shortages.

Extended Supply Contracts Signal Long-Term Industry Stability

A notable shift in industry dynamics has emerged through the establishment of longer-term supply agreements. Hyperscalers and high-end chipmakers are now committing to multi-year contracts extending until 2030, representing a significant departure from previous agreements that typically lasted only one year with flexible financing terms. These new arrangements require approximately 20% cash deposits to secure supply, demonstrating the critical importance of memory chips in AI data centre buildouts. Equipment manufacturers report that these extended memory contracts provide enhanced supply chain visibility extending through the end of 2027.

Processor Segment Shows Accelerating Growth Trajectory

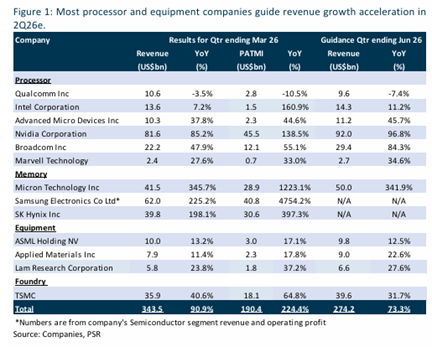

The processor segment continues its growth acceleration, with first-quarter 2026 revenue surging 53% year-on-year, up from 40% growth in the fourth quarter of 2025. This momentum is expected to continue, with second-quarter 2026 revenue guidance indicating a substantial 67% year-on-year increase to US$159 billion. The growth is underpinned by robust hyperscaler demand for data centre GPUs, CPUs, and ASICs.

NVIDIA leads the sector with first-quarter revenue spiking 85% year-on-year to US$81.6 billion, marking the third consecutive quarter of accelerating growth. AMD demonstrated its strongest year-on-year growth since 2022, with revenue increasing 38% to US$10.3 billion, driven by MI350 GPU and fifth-generation EPYC CPU adoption. Broadcom achieved its strongest growth since 2016, with revenue rising 48% year-on-year to US$22.2 billion, supported by AI semiconductor revenue that grew 143% year-on-year to a record US$10.8 billion.

The sector maintains strong forward momentum, supported by hyperscalers’ combined 2026 capital expenditure guidance of US$710 billion, representing an 89% year-on-year increase. Equipment players continue to benefit from strong services demand as memory customers seek performance upgrades on existing tools due to limited cleanroom space.

Frequently Asked Questions

Q: What drove the exceptional performance of memory companies in the semiconductor sector?

A: Memory companies achieved remarkable gains of 95% due to first-quarter 2026 earnings growth exceeding 900% year-on-year, primarily driven by a surge in DRAM and NAND prices resulting from memory chip shortages.

Q: How have supply contracts changed in the semiconductor industry?

A: Hyperscalers and high-end chipmakers are now signing longer-term multi-year supply contracts lasting until 2030, requiring approximately 20% cash deposits. This represents a significant change from previous agreements that lasted only about one year with looser financing terms.

Q: Which processor companies showed the strongest growth performance?

A: NVIDIA led with 85% year-on-year revenue growth to US$81.6 billion, followed by Broadcom with 48% growth to US$22.2 billion, and AMD with 38% growth to US$10.3 billion, marking AMD's largest year-on-year growth since 2022.

Q: What is driving the acceleration in processor segment revenue?

A: The acceleration is driven by strong demand from hyperscalers for data centre GPUs, CPUs, and ASICs, supported by hyperscalers' guidance for combined 2026 capital expenditure to surge 89% year-on-year to US$710 billion.

Q: How are equipment companies benefiting from current market conditions?

A: Equipment players are experiencing strong services demand as memory customers seek performance upgrades on existing tools due to limited cleanroom space,. Extended memory contracts providing supply chain visibility through the end of 2027.

Q: What is the outlook for second-quarter 2026 processor revenue?

A: Processor revenue for second-quarter 2026 is guided to surge 67% year-on-year to US$159 billion, with all processor companies except Qualcomm providing guidance for accelerated growth.

Q: Which company faced challenges in the processor segment?

A: Qualcomm experienced difficulties with revenue declining 3.5% year-on-year to US$10.6 billion, weighed down by rising memory prices that reduced inventory demand from Chinese OEM customers. A further decline of 7% year-on-year guided for second-quarter 2026.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.