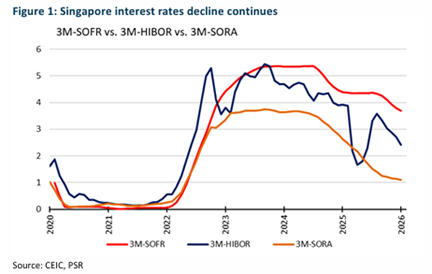

Interest Rates Hit 45-Month Low

Singapore’s banking sector faces a mixed outlook as interest rates continue their downward trajectory whilst geopolitical tensions create market volatility. March’s 3M-SORA declined 5 basis points month-on-month to 1.09%, marking the lowest level since July 2022. This represents a significant 153 basis points year-on-year decline, though notably, the decline is also the smallest yearly decrease in nine months.

The interest rate environment reflects Singapore’s status as a “safe haven” destination, with capital inflows driving FX reserves up 10% year-on-year in February 2026. However, analysts expect the 3M-SORA decline to moderate for the remainder of the year as Middle East conflict concerns reduce expectations for Federal Reserve rate cuts.

Banking Fundamentals Show Resilience

Despite the challenging rate environment, Singapore banks demonstrate solid underlying fundamentals. Loan growth continues its upward trajectory, with February 2026 figures showing 6.3% growth, whilst banks guide for low to mid-single digit expansion. Current Account and Savings Account (CASA) deposits rose 11% year-on-year, with the CASA ratio improving to 20% from 19.8% in January 2025. This improvement provides a crucial tailwind for banks by lowering funding costs and cushioning net interest margin compression.

The sector’s exposure to potential regional risks appears well-contained. Trade, Services and Commodities loans, including Oil & Gas exposure, represent only approximately 7% of total gross loans across the three major banks. Sector non-performing loan ratios remain benign at 0.3-2.0%, whilst ASEAN loan growth averages low-to-mid single digits year-on-year, suggesting limited risk from Middle East conflicts.

Market Outlook and Investment Preference

The escalation of Iran conflict and oil prices surging past US$100 per barrel have prompted the Federal Reserve to raise its 2026 PCE inflation forecast to 2.7%. Markets now price in zero rate cuts for the remainder of 2026, creating a higher-for-longer rate backdrop that supports net interest margins. Quarter-on-quarter NIM stabilisation is already evident at OCBC and UOB in Q4 2025.

Heightened market volatility continues benefiting capital markets income and wealth management fees, providing meaningful offset to net interest income headwinds. Banks maintain attractive dividend yields at 4.9%, with ongoing buybacks improving return on equity. The research maintains a NEUTRAL sector rating, expressing preference for DBS due to its fixed-dividend policy and OCBC for wealth management growth and excess capital.

Frequently Asked Questions

Q: What is the current level of Singapore’s 3M-SORA and how does it compare historically?

A: March’s 3M-SORA stands at 1.09%, representing the lowest level in 45 months since July 2022. It declined 5 basis points month-on-month and 153 basis points year-on-year.

Q: How are Singapore banks performing in terms of loan growth?

A: Singapore loan growth continues climbing, with February 2026 showing 6.3% growth. Banks are guiding for low to mid-single digit growth going forward.

Q: What is the banks’ exposure to potential Middle East conflict risks?

A: Singapore banks’ TSC loans, including O&G exposure, represent only approximately 7% of total gross loans in aggregate, with sector NPL ratios remaining benign at 0.3-2.0% across the three banks.

Q: How are deposit trends affecting the banking sector?

A: CASA deposits rose 11% year-on-year with the CASA ratio improving to 20% from 19.8% in January 2025, providing a tailwind by lowering funding costs and cushioning NIM compression.

Q: What is the research recommendation for Singapore banks?

A: The research maintains a NEUTRAL rating on the sector, with preference for DBS due to its fixed-dividend policy and OCBC for wealth management growth and excess capital.

Q: How are current market conditions affecting bank revenues?

A: Heightened market volatility benefits capital markets income and wealth management fees, providing meaningful offset to net interest income headwinds from the rate environment.

Q: What are the dividend prospects for Singapore banks?

A: Banks maintain attractive dividend yields at 4.9%, with ongoing buybacks improving return on equity, making them appealing for income-focused investors.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.