Strong Government Pipeline Drives Sector Optimism

Singapore’s construction sector presents a compelling investment opportunity despite recent margin pressures from Middle East conflict-related cost inflation. Construction-related companies have delivered solid returns, rising an average of 7% over the three months to May 2026, though moderating from the previous quarter’s 26% gain. Phillip Securities Research maintains an OVERWEIGHT rating on construction-related companies, citing strong government project visibility and sector resilience.

Infrastructure Challenges Mitigated by Government Intervention

The sector faces headwinds from the Iran war’s impact on fuel costs, with diesel prices surging 104% year-on-year to a record S$4.6 per litre in April 2026 following the closure of the Straits of Hormuz. Infrastructure companies bore the brunt of these pressures, declining 3% over the quarter as investors worried about margin compression from elevated diesel and bitumen prices.

However, the Building and Construction Authority (BCA) announced crucial support measures in April 2026, committing to cover 50% of direct additional costs from diesel and bitumen usage between March and May 2026. This intervention particularly benefits contractors involved in earthworks, foundation and piling works, and roadworks—segments most exposed to diesel-powered equipment costs.

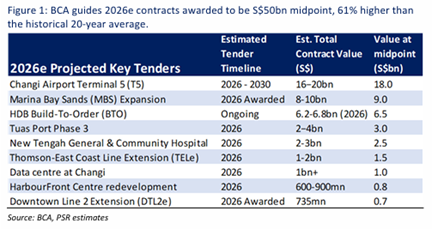

Robust Project Pipeline Supports Medium-Term Growth

The sector’s medium-term outlook remains strong, underpinned by substantial government project commitments. The BCA has guided S$50bn in contract awards for 2026, representing a 61% premium to the historical 20-year average. Major project tenders for the remainder of 2026 include the Changi Airport Terminal 5 development, Tuas Port Phase 3 expansion, and the new Tengah General and Community Hospital, each valued at over S$2bn.

Looking ahead, construction demand is projected at S$39-46bn annually from 2027-2030, maintaining a 37% premium to the historical average of S$31bn yearly. Key upcoming projects include the Cross Island MRT Line Phase 3 expansion, Integrated Waste Management Facility Phase 2, Greater Sentosa Master Plan infrastructure works, and Woodlands Checkpoint redevelopment Phase 3.

The sector benefits from Singapore’s relative insulation from Middle East conflicts, with labour and raw material supplies remaining available. Companies with higher exposure to public sector contracts are particularly well-positioned to capitalise on the government’s substantial infrastructure investment programme.

Frequently Asked Questions

Q: What is Phillip Securities Research's recommendation on Singapore construction companies?

A: Phillip Securities Research maintains an OVERWEIGHT rating on construction-related companies, believing the sector remains relatively insulated from Middle East conflicts and is positioned to benefit from strong government project visibility.

Q: How have construction companies performed recently?

A: Construction-related companies rose an average of 7% over the three months to May 2026, though this was a moderation from the previous quarter's 26% gain. Infrastructure companies were the biggest laggards, declining 3% due to margin compression concerns.

Q: What support has the government provided for rising fuel costs?

A: The BCA announced in April 2026 that the government would cover 50% of direct additional costs from diesel and bitumen usage from March 1 to May 31, 2026, helping contractors manage cost pressures from fuel price surges.

Q: How significant is the 2026 construction pipeline compared to historical levels?

A: The BCA has guided S$50bn in contract awards for 2026, which is 61% higher than the historical 20-year average, indicating exceptionally strong government demand for construction services.

Q: What major projects are expected in 2026?

A: Key project tenders for 2026 include Changi Airport Terminal 5 development, Tuas Port Phase 3 expansion, and the new Tengah General and Community Hospital, each worth more than S$2bn.

Q: What is the medium-term construction demand outlook?

A: The BCA projects construction demand of S$39-46bn annually from 2027-2030, representing a 37% premium to the historical 20-year average of S$31bn yearly.

Q: Which contractors are most affected by diesel price increases?

A: Contractors relying on diesel-powered equipment are most exposed, particularly those involved in earthworks, foundation and piling works, and roadworks, as diesel prices surged 104% year-on-year to S$4.6 per litre in April 2026.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.