DAILY MORNING NOTE | 10 July 2023

Week 28 equity strategy: Despite the disappointing job additions in the U.S., a rate hike on the 26July FOMC meeting is almost certain. June payroll additions of 209k was the weakest since the pandemic. Fed chair Powell’s preferred measure of labour slack, job vacancies to unemployed, remains high at 1.6x vs pre-pandemic 1.2x. Also, there are no signs that wage growth is slowing down. June reading of 4.4% YoY is unchanged for the past three months.

Adding pressure on equities, particular their valuations, is the recent rebound in bond yield. US 10-year Treasuries crossed 4%, reaching the year highs of 4.068%. Judging by the rise in TIPs yield, we think the bond market is pricing in a persistent inflation environment rather than just stronger growth. We think equity markets are heading into the dual strains of slowing growth together with elevated interest rates.

In Singapore, retail sales have slowed significantly post re-opening. In May, sales were only up 1.8% YoY (Apr+4.3%), coming close to pre-pandemic growth rates of 0.5%. It was a discouraging indicator for retail REITs and supermarkets. The sector still enjoying huge momentum is hospitality. Visitor arrivals in June were 1.129mn, up 108% YoY and the highest monthly figure since the pandemic. Another interesting stat was HDB prices are now outpacing private resale. A four-year CAGR of 7.7% vs private resale’s 6.5%.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore stocks fell 0.4 per cent or 10.96 points to close at 3,139.47 on Friday (Jul 7), after the US posted stronger-than-expected economic data overnight. Across the broader market, losers beat gainers 303 to 240 after 1.32 billion securities worth S$1.03 billion were traded. Japan’s Nikkei 225 and South Korea’s Kospi both shed 1.2 per cent, while Hong Kong’s Hang Seng Index fell 0.9 per cent.

Wall Street stocks dipped Friday (Jul 7) following data that showed slower hiring in the United States but which was seen as keeping the Federal Reserve on track to raise interest rates. The world’s biggest economy added 209,000 jobs last month, fewer than expected, but the unemployment rate edged down to 3.6 per cent, remaining close to historic lows. The Dow Jones Industrial Average finished down 0.6 per cent at 33,734.88. The broad-based S&P 500 dipped 0.3 per cent to 4,398.95, while the tech-rich Nasdaq Composite Index slipped 0.1 per cent to 13,660.72.

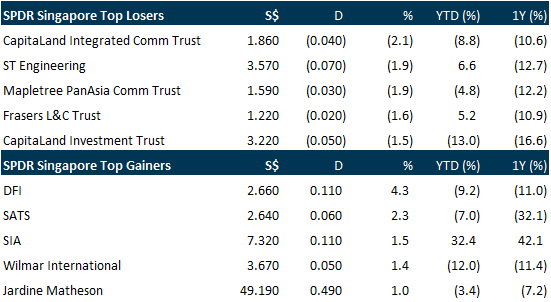

Top gainers & losers

EVENTS OF THE WEEK

SG

Chinese carmaker Maxus will launch its T90 pickup truck in Singapore in the fourth quarter of the year. This will make it the first fully-electric pickup to be sold by an authorised dealer, since the vehicle is currently available through parallel importers. Jardine Cycle & Carriage, the authorised distributor and dealer for Maxus in Singapore, made the announcement at the launch of another Maxus model, the Mifa multi-purpose vehicle, on Friday (Jul 7). Cycle & Carriage representatives said that there is no official estimated pricing yet, but as a fully-electric light commercial vehicle, the truck is likely to qualify for the maximum Commercial Vehicle Emissions Scheme rebate of S$15,000.

Half of the 598 units at Lentor Hills Residences were sold on its launch weekend at an average price of S$2,080 per square foot (psf), said joint developer Hong Leong Holdings on Sunday (Jul 9). A total of 298 units in the 99-year leasehold project were sold as at 5 pm on Sunday. Buyers were predominantly Singaporeans, with the rest being permanent residents. Units were sold at a starting price of S$1,834 psf. All apartment types were “well-received” by homebuyers, with the two-bedroom and the two-bedroom-plus-study units being the most popular, said Hong Leong.

Singapore’s Energy Market Authority (EMA) is seeking proposals that drive the research and development of energy storage systems (ESS). Successful applicants will be awarded a grant under the statutory board’s second ESS grant call. EMA is looking for proposals that develop more land-efficient, cost-effective and safer ESS solutions suited for the Republic’s tropical and urbanised climate. Most recently, EMA, with support from Enterprise Singapore (EnterpriseSG), awarded grants to three local energy startups – Power Facade, Ampotech and EtaVolt – through separate partnerships with Shell and Envision Digital.

US

Oil prices climbed about 3 per cent to a nine-week high on Friday (Jul 7) as supply concerns and technical buying outweighed fears that further interest rate hikes could slow economic growth and reduce demand for oil. Brent futures rose US$1.95, or 2.6 per cent, to settle at US$78.47 a barrel, while US West Texas Intermediate crude (WTI) rose US$2.06, or 2.9 per cent, to settle at US$73.86. That was the highest close for Brent since May 1 and WTI since May 24. Both benchmarks ended up about 5 per cent for the week.

Gold prices rose on Friday (Jul 7) and were on track for their first weekly gain in four as the dollar and bond yields fell after weaker US nonfarm payrolls numbers cast doubts over the trajectory of interest rate hikes beyond July yet again. Spot gold was up 0.8 per cent at US$1,926.54 per ounce at 2.06 pm EDT (1806 GMT). Bullion was up 0.4 per cent so far this week. US gold futures settled 0.9 per cent higher at US$1,932.50.

Electric vehicle maker Tesla rolled out a new program globally allowing buyers to earn extra incentives through referrals from existing customers, a strategy long used by traditional automakers to boost sales. The incentive, which Tesla dubbed as “Refer and Earn” on its websites, is equivalent to about US$500 in cashback for buyers in the US who purchase Model 3 and Model Y. The US incentives also include three months of its Full Self-Driving feature. The program was rolled out in Tesla’s largest markets, including the US, China, Germany, France, Canada, Mexico, Hong Kong and Singapore, according to the company’s regional websites on Friday (Jul 7).

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, PSR

RESEARCH REPORTS

Advanced Micro Devices Inc. – More market share gains expected

Recommendation : ACCUMULATE (Initiation); TP: US$125.00, Last Close: US$113.17

Analyst: Maximilian Koeswoyo

• Significant market share gain in data centre CPU market from ~4% in 2017 to ~20% in 2022. We expect further gain due to more workloads being migrated to AMD-based systems. An opportunity to raise its presence in data centre GPU market as customers look for second source supplier due to increased adoption of generative AI.

• We expect margin to grow post acquisition of Xilinx and Pensando from 45% in FY22 to 48% in FY23e due to growing revenue contribution from Data Centre and Embedded.

• Initiate coverage with ACCUMULATE recommendation and DCF-based target price (WACC 7.4%, g 3.5%) of US$125.00. We expect FY23e revenue to experience marginal growth driven by Data Centre and Embedded segments, offset by the decline in Client and Gaming, with growth re-accelerating in FY24e as Data Centre sales mix shift towards the EPYC 9004 series server CPUs, which we believe to have ~50% higher ASP.

FAANGM Monthly June 23 – Re-rating driving most of the gains

Recommendation: NEUTRAL (Maintained); Analysts: Jonathan Woo, Maximilian Koeswoyo, Zane Aw, Phillip Research Team

• FAANGM was a slight laggard in June, up 5.6% compared to the Nasdaq and S&P 500’s gain of 6.5%. 1H23 Performance: FAANGM +49%, Nasdaq +39%, S&P 500 +16%. We estimate around half of the gains in the S&P 500 YTD has come from FAANGM stocks.

• NFLX was the biggest gainer, up almost 12% on positive subscriber growth following its password crackdown initiative. GOOGL was the biggest laggard, down -2% for the month with price consolidating at a key resistance point.

• We see most of the stock performance this year a result of multiple expansion due to cost-cutting measures and AI-driven hype, rather than positive earnings revision. We believe near-term weakness in demand for tech consumer goods, digital advertising, and Cloud, still persist. As such, we remain NEUTRAL on FAANGM.

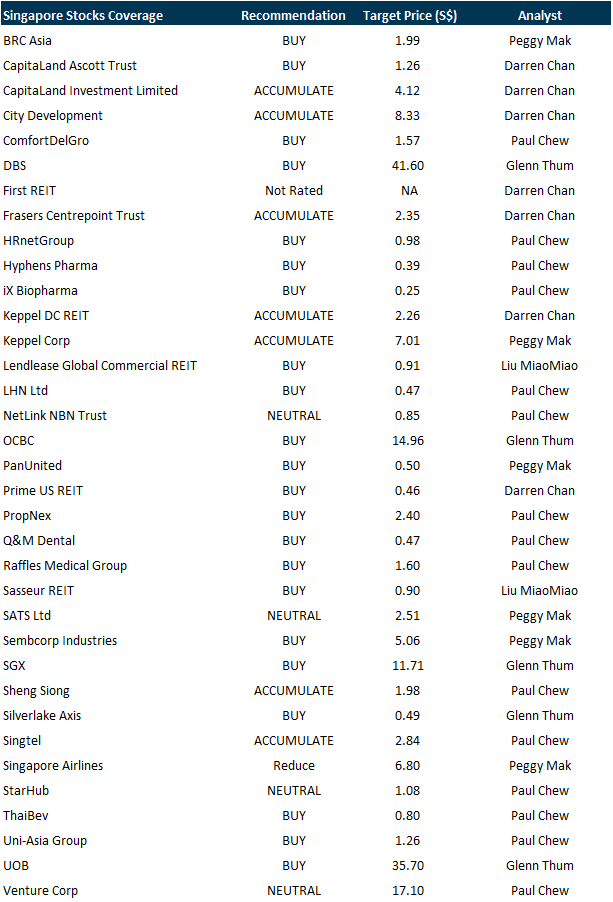

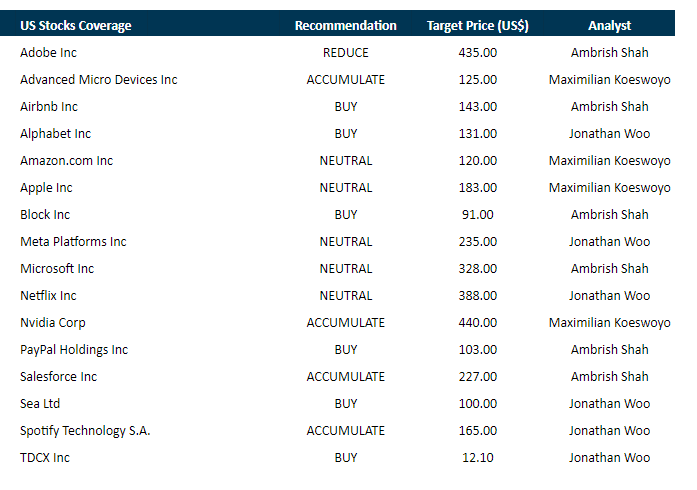

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Strategy & Stock Picks 3Q23 (US)

Date: 13 July 2023

Time: 7.30pm – 9pm

Register: https://tinyurl.com/5n7cuwtm

Strategy & Stock Picks 3Q23 (SG)

Date: 15 July 2023

Time: 10am – 12pm

Register: https://tinyurl.com/2fsww93d

Guest Presentation by Ohmyhome [NEW]

Date: 20 July 2023

Time: 12pm – 1pm

Register: https://tinyurl.com/52fef7dh

POEMS Podcast:

Research Videos

Weekly Market Outlook: UHReit, SG Property, Tech Analysis, SG Equity 3Q23 Strategy, SG Weekly & More

Date: 3 July 2023

Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Phillip Research in 3 minutes: #29 Keppel Corporation; Initiation

Click here for more on Phillip in 3 mins.

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials