Sheng Siong Group Ltd - Reopening minus and inflation plus

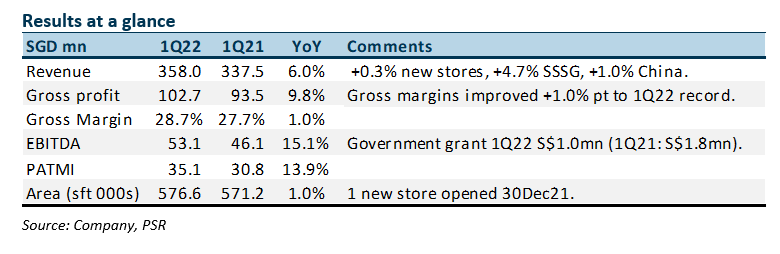

29 Apr 2022- 1Q22 revenue/PATMI was within expectations at 28%/31% of our forecast. We have modelled a decline in sales in 2H22.

- Margins continue to climb. The 28.7% gross margin in 1Q22 is the highest for a festive laden quarter where promotions are more prevalent.

- We maintain our FY22e earnings. Our BUY recommendation and target price of S$1.75 are unchanged. Our valuation is pegged to 23x PE, a 10% discount to the 5-year historical average of 25x PE The reopening of borders and group restrictions is expected to reduce home dining. This will negatively impact the consumption of groceries. The return of Malaysian workers who were temporarily residing in Singapore is another potential loss of customers. A possible implication of rising inflation is consumers downgrading to home dining or shopping more in value grocers such as Sheng Siong. FY22e will be a transition year but valuations have turned more attractive and the resumption of new store openings will help drive earnings growth.

The Positives

+ Gross margins keep rising. A higher mix of fresh food drove margins higher, again. SSG’s strength is in meat and seafood. There is a higher level of complexity in handling these items than fruits and vegetables due to their higher value and level of freshness and perishability.

+ Guiding three to five new stores per annum. In 2021, SSG added only 1 new store. The company is guiding 3 to 5 new stores per year over the next three to five years in HDB housing estates. There are another 17 locations planned to be opened in such estates over the next three years.

+ Same-store sales accelerated. Same-store sales accelerated in 1Q22 to 4.7% YoY. This is faster than 2H22 3.6% YoY. Pre-pandemic, same-store sales grew at 0.1% in 2019 and a negative 1% in 2018.

The Negative

– Nil

Outlook

Borders reopening, lifting of dining restrictions and the return to office will result in less dining at home and grocery shopping. Alternatively, higher grocery prices could lead to consumers shifting more to value grocers or home dining. The secular trend of taking market share from wet markets remains intact. The three new stores will contribute to growth this year as they add another 24.5k sft of space or a 4% increase in total footprint.

Maintain BUY with unchanged TP of S$1.75

SSG’s attractive financial metrics include ROEs of 27%, dividend yields at 3.6% and net cash at S$254mn (as at Mar2022).

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Trade of the Day - iFAST Corporation Ltd (SGX: AIY)

Trade of the Day - iFAST Corporation Ltd (SGX: AIY) Trade of the Day - Singapore Airlines (SGX: C6L)

Trade of the Day - Singapore Airlines (SGX: C6L) Trade of the Day - COSCO Shipping International (Singapore) Co Ltd (SGX: F83)

Trade of the Day - COSCO Shipping International (Singapore) Co Ltd (SGX: F83) Trade of the Day - Microsoft Corp (NASDAQ: MSFT)

Trade of the Day - Microsoft Corp (NASDAQ: MSFT)