Sheng Siong - Stock Analyst Research

| Target Price* | 1.66 |

| Recommendation | ACCUMULATE› ACCUMULATE |

| Market Cap* | - |

| Publication Date | 1 Mar 2024 |

*At the time of publication

Sheng Siong Group Ltd - Lack of new stores

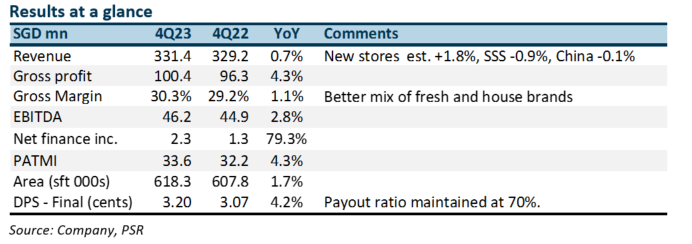

- FY23 revenue and PATMI were within expectations at 99%/99% of our forecast. Revenue growth was 2.1% YoY. Same-store sales contracted and new-store expansion was muted.

- For 2023, Sheng Siong only expanded with two new stores or a footprint growth of 1.7% (2022: +5.4%). The lack of new stores will weigh on revenue growth this year. The company aims to expand a minimum of three stores or equivalent 2.4% expansion per year.

- Same-store sales growth is expected to improve as outbound travel normalises. Inflationary pressure will also support more dining at home. The company has secured two stores so far this year in Singapore, with another ten likely to be tendered. We marginally lower our FY24e earnings by 2%. With a more sluggish growth outlook, we lower our target valuations from historical 20x PE to 18x. The target price is reduced to S$1.66 (prev. S$1.80). Until new stores accelerate, growth will be muted.

The Positives

+ Rise and rise of margins. Gross margins have been on an upward trajectory since listing. A decade ago, gross margins were 23% in FY13 and now stand at 30%. Scale, distribution centre, direct sourcing, and fresh food mix have been the major driver of margin expansion. The new driver is house brands. Competitors have also been raising prices to pass on their cost of production.

The Negatives

– No new stores. There were no new stores this quarter, and only two were opened this year. Expansion in new stores is a cumulative 8% over three years. Before this lull, new stores grew 7-8% p.a. The lack of new stores was due to fewer tenders made available. Of the five stores tendering in 2023, Sheng Siong has been successful in securing three.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU