Japan-Weekly Strategy Report “AT1 bonds, downward revision of domestic regional banks, foreign bonds and yen appreciation / bond appreciation”

28 Mar 2023Report type: Weekly Strategy

AT1 bonds, downward revision of domestic regional banks, foreign bonds and yen appreciation / bond appreciation

Banking instability caused by a string of US regional bank failures spilled over into Europe, and in Switzerland, Credit Suisse agreed to be acquired by UBS. At that time, the bond market was shocked when about 2.2 trillion yen worth of “Additional Tier 1 Bonds (AT1 Bonds)”, a type of subordinated bond issued by Credit Suisse for core capital expansion, was deemed worthless. These AT1 bonds are also known as contingent convertible bonds (CoCo bonds) and are sometimes referred to as “high-yield investments with a hand grenade attached”. CoCo bonds are essentially a hybrid of bonds and stocks, and are considered a means of pulling financial institutions out of a crisis while avoiding burdening taxpayers and diluting existing shareholders’ stock in the event of a bank failure. When a bank’s capital level falls below a certain level, the bonds may be converted into bank shares (capital), or the value of some or all of the bond’s principal may be reduced.

Silicon Valley Bank is said to have invested and managed its rapidly growing deposits in long-term US Treasury bonds and mortgage-backed securities, which led to unrealized losses on bonds as interest rates rose, eating up most of its equity capital. This is a special exception and does not apply to Japanese regional banks. Nevertheless, before the announcement of financial results for the fiscal year ending March 2023, some regional banks have begun to revise their full-year earnings outlook downward. Fukuoka Financial Group (8354) was reported to have executed loss-cutting measures due to an expansion of unrealized losses in its US bond investments. Mebuki Financial Group (7167), which owns Joyo Bank and Ashikaga Bank, is selling foreign bonds that have become less profitable due to rising overseas interest rates to improve its portfolio. Nara-based Nanto Bank (8367), Nagoya Bank (8522), and Hirogin Holdings (7337), which has Hiroshima Bank as its core, have also revised their earnings forecasts downward for similar reasons.

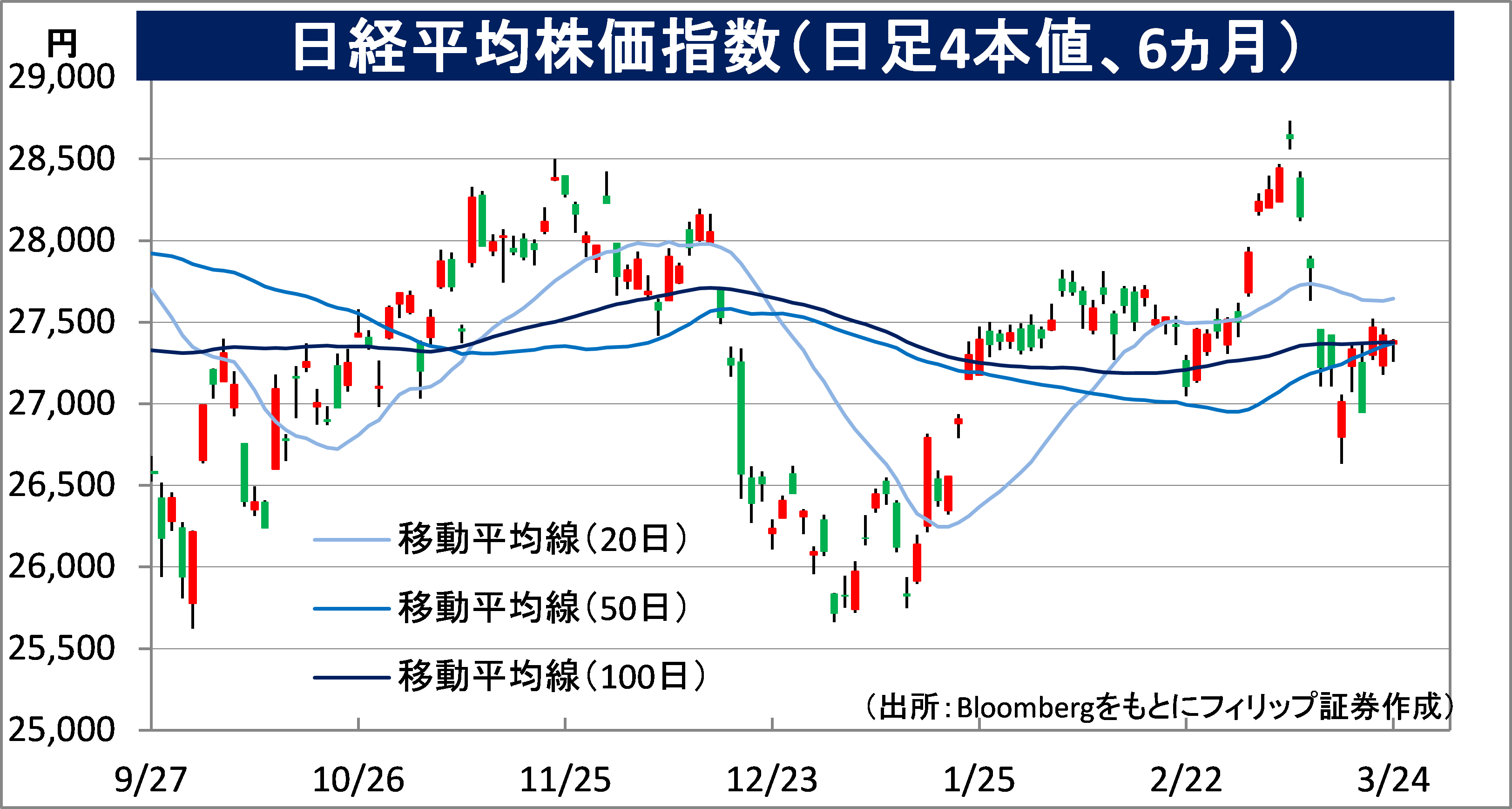

As of the close of 23/3, the domestic bond market was hovering around a yield of 0.3% for the benchmark new 10-year JGB, well below the upper limit of the allowable range of 0.5% under the BOJ’s YCC (Yield Curve Control) policy. While in large part keeping pace with the foreign bond market, it is also believed that in many cases funds from the sale of foreign bonds are repatriated to Japan to purchase domestic bonds, which may in part support a stronger yen and higher domestic bond prices (i.e., lower long-term interest rates). The Nikkei Average is therefore expected to remain firm until the end of the March fiscal year, as lower domestic long-term interest rates are likely to support the Japanese stock market.

The consumer price index (CPI) for February, announced on 24/3, showed a 3.1% increase YoY in the composite CPI (excluding fresh food), the first slowdown in 13 months. However, the composite CPI excluding fresh food and energy increased by 3.5% YoY, accelerating from January’s 3.2% increase. The national average of public land prices as of 1/1, announced on 22/3, rose for the second consecutive year by 1.6% YoY for all uses. The domestic inflation trend will be closely monitored.

In the 27/3 issue, we will be covering Daiseki Eco Solution (1712), Stella Chemifa (4109), Life Corp (8194), and NTT Data (9613).

Daiseki Eco Solution Co. Ltd (1712) 921 yen (24/3 closing price)

・Established in 1996. With Daiseki (9793), a major industrial waste management company based in Nagoya as its parent, company operates various businesses including the mainstay soil contamination survey and treatment business, waste gypsum board recycling, environmental analysis, PCB and BDF (biodiesel fuel) businesses.

・For 9M (Mar-Nov) results of FY2023/2 announced on 5/1, net sales decreased by 10.6% to 11.872 billion yen compared to the same period the previous year, and operating income decreased by 48.9% to 930 million yen. Sales and operating income increased in the waste gypsum board recycling business due to higher sales volume, but sales in the mainstay soil contamination survey and treatment business declined 13% YoY and operating income fell 48% YoY due to lower-than-planned large-scale infrastructure improvement projects.

・For its full year plan, net sales is expected to decrease by 13.3% to 14.8 billion yen compared to the previous year, operating income to decrease by 52.4% to 1.0 billion yen, and annual dividend to increase by 2 yen to 10 yen. Both operating income and operating margin are expected to recover from 1Q (Mar-May) to 3Q (Sep-Nov) on a quarterly basis due to focus on high value-added projects. The industrial waste treatment industry has high barriers to entry and tends to become an oligopoly through M&A. In this context, it may be easier to improve profit margins through group restructuring.

Stella Chemifa Corp (4109) 2,596 yen (24/3 closing price)

・Founded by Jisaburo Hashimoto in Sakai City in 1916 to manufacture nitrate salt. Besides its High-purity Chemical Business, which includes fluorides for semiconductors and lithium-ion rechargeable batteries, Stellar Pharma (4888) is involved in boron pharmaceuticals for cancer radiotherapy.

・For 9M (Apr-Dec) results of FY2023/3 announced on 10/2, net sales increased by 4.2% to 28.27 billion yen compared to the same period the previous year, and ordinary income including equity in earnings of affiliates decreased by 4.7% to 3.75 billion yen. Net income declined 47.5% YoY to 1.658 billion yen due to impairment losses on property, plant, and equipment held for the purpose of increasing production of additives for lithium-ion rechargeable batteries in the High-purity Chemical Business.

・Company has revised its full year plan downwards. Net sales is expected to decrease by 4.5% to 35.6 billion yen (original plan 37.5 billion yen) compared to the previous year, and operating income to decrease by 18.2% to 3.75 billion yen (original plan 4.6 billion yen). Annual dividend to remain unchanged at 60 yen. Sales in the semiconductor sector of the High-purity Chemical Business, which was the main cause of the downward revision, are expected to improve due to the Japanese government’s decision to relax strict export controls on hydrogen fluoride to the ROK. Estimated PER of 15.3x and PBR of 0.7x at the closing price on 23/3.

About the author

Phillip Research Team (Japan)

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

- recipients of the analyses or reports are to contact Phillip Securities Research (and not the relevant foreign research house) in Singapore at 250 North Bridge Road, #06-00 Raffles City Tower, Singapore 179101, telephone number +65 6533 6001, in respect of any matters arising from, or in connection with, the analyses or reports; and

- to the extent that the analyses or reports are delivered to and intended to be received by any person in Singapore who is not an accredited investor, expert investor or institutional investor, Phillip Securities Research accepts legal responsibility for the contents of the analyses or reports.

About the author

Phillip Research Team (Japan)

Latest Reports

Software Quarterly Update 4Q25 - Fundamentals remain intact

Software Quarterly Update 4Q25 - Fundamentals remain intact 名創優品 (9896.HK) 1-2 月同店超預期高增,有望驅動全年戴維斯雙擊

名創優品 (9896.HK) 1-2 月同店超預期高增,有望驅動全年戴維斯雙擊- MINISO (9896.HK) The strong same-store sales growth in Jan and Feb exceeded expectations, potentially driving a Davis Double Play for the full year

Lion-Phillip S-REIT ETF - Valuation attractive as rate outlook stays supportive

Lion-Phillip S-REIT ETF - Valuation attractive as rate outlook stays supportive