Company at a Glance

What the company does:

Global Resource Construction Ltd. is a Singapore-based, construction-led group spanning building construction, civil infrastructure, environmental engineering, prefabrication and procurement. The group scaled up materially following the April 2025 acquisition of Chip Eng Seng Construction Pte. Ltd. and its subsidiaries in April 2025.

Main income source:

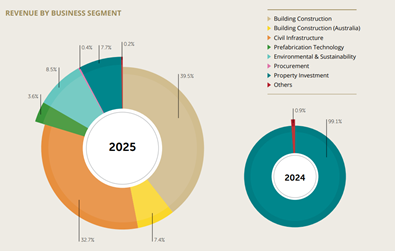

GRC’s main income source is now predominantly construction-led following the CES Construction acquisition, with earnings primarily driven by Singapore public-sector projects. In 1H26, Building Construction contributed 56.2% of revenue, mainly from HDB and large-scale public housing projects, while Civil Infrastructure contributed 27.5% from MRT, airport and water infrastructure works, 84% of group revenue is derived from core construction execution. Smaller segments such as Australia construction (6.5%), environmental & sustainability (6.0%), prefabrication (2.0%), procurement (0.5%) and property investment (1.2%) provide diversification. This implies GRC’s credit profile is largely dependent on construction project execution and order book replenishment rather than recurring rental or asset-based income.

What Supports the Credit Profile

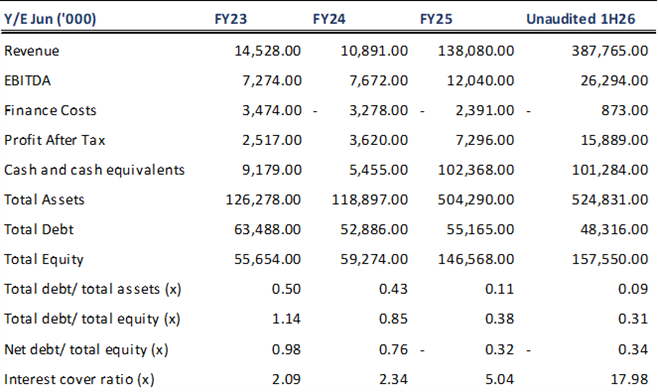

Acquisition expanded scale and diversified earnings base. The April 2025 acquisition transformed GRC from a rental-centric to an integrated construction-focused group spanning building construction, civil infrastructure, environmental engineering, prefabrication, and procurement. This has improved operating scale, liquidity and earnings capacity, reflected in FY25 revenue rising to S$138.1mn from S$10.9mn and net current liabilities of S$9.9mn reversing to net current assets of S$46.6mn. The acquisition also broadened GRC’s earnings base from primarily rental and property-related income into multiple construction-linked income streams, including public housing, MRT, water infrastructure, prefabrication and procurement.

Public-sector anchored order book supports earnings visibility. The group’s S$2.9bn order book provides near- to medium-term revenue visibility, with management guiding that 42% is expected to be recognised in FY2026 and a further 31% in FY2027. A significant portion is anchored by public-sector projects with HDB, LTA and PUB, supporting lower counterparty risk and partial protection against key material cost fluctuations. Ongoing contract replenishment, including the recently secured A$67mn Max Apartments project in Australia, further extends pipeline continuity into FY26.

Low leverage credit profile. Despite materially scaling up following the acquisition, GRC maintained conservative credit metrics at 1H26, with debt/assets of 0.09x, debt/equity of 0.31x and interest coverage of 17.98x, supporting strong near-term debt-servicing capacity.

Financial Position

Our Credit View

We are positive on GRC’s credit profile, supported by its expanded operating scale following the CES Construction acquisition, a diversified earnings base, and a sizeable S$2.9bn order book that provides near- to medium-term revenue visibility. The acquisition transformed GRC from a narrower, rental-centric platform into a broader construction-led group with stronger liquidity, greater business relevance, and wider access to public-sector infrastructure pipelines. Credit metrics remain conservative despite the scale-up, with low leverage and strong interest coverage supporting balance sheet resilience.