Company at a Glance

What the company does:

Koh Brothers Group Ltd is a Singapore-listed group mainly involved in engineering & construction, building materials, bio-refinery and renewable energy (via Oiltek), real estate, and hospitality. Its core business is engineering & construction through Koh Brothers Eco Engineering and Koh Brothers Building & Civil Engineering Contractor, which undertakes civil infrastructure, water treatment, tunnelling and public-sector building projects in Singapore. Major ongoing projects include Changi Airport Terminal 5 intra-terminal tunnels, the Lorong Halus Bus Depot, and the Tuas Water Reclamation Plant.

Main income source:

KBGL’s income is primarily from Construction & Building Materials. In FY25, this segment generated S$321.0mn revenue out of total group revenue of S$329.4mn (97.4% of group revenue).

What Supports the Credit Profile

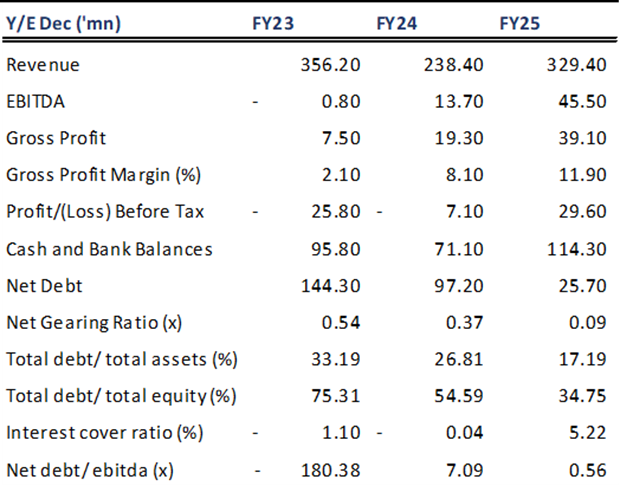

FY25 profit turned around mainly due to stronger core construction performance, supported by one-off disposal gains.

Revenue rose 38.2% YoY to S$329.4mn, while gross profit more than doubled 103% YoY to S$39.1mn, with gross margin improving to 11.9% from 8.1%. FY25 margin recovery likely reflects improved project execution and project mix relative to prior years, after FY23 profitability was pressured by prolonged construction periods and elevated material, manpower and subcontractor costs. In addition, reported profitability was further supported by higher other gains of S$14.0mn (FY24: S$3.4mn), largely due to a one-off land disposal gain in Johor.

Source: Koh Brothers Presentation Slides

Source: Koh Brothers Presentation Slides

Changi T5 and Lorong Halus are now the main backlog drivers

FY25 construction order book rose to S$1.126bn (+35.8% YoY), driven increasingly by new large-scale projects. Key projects include the S$999.1mn Changi Airport T5 intra-terminal tunnel (2.3% complete) and the S$313.9mn Lorong Halus Bus Depot (2.9% complete), which should provide stronger medium-term revenue visibility.

Credit metrics strengthened

Net gearing declined from 0.54x in FY23 to 0.09x in FY25, while net debt / EBITDA improved significantly from 7.09x in FY24 to 0.56x in FY25 as EBITDA recovered and net debt reduced. Interest coverage also strengthened to 5.22x from near-breakeven levels, indicating operating earnings are now far better positioned to support debt obligations.

Main Areas to Monitor:

1) FY25 profitability improved sharply, but part of the earnings was supported by non-core gains including land disposal. The key forward question is whether core construction margins can sustain earnings as one-off gains fade.

Financial Position

Source: Koh Brothers Presentation Slides

Source: Koh Brothers Presentation Slides

Koh Brothers SGD Bond Opportunities

* YTM/YTC shown are indicative only and subject to market conditions, price fluctuations, and final trade execution. For bond pricing, further information, and available offerings, please contact bonds@phillip.com.sg

* YTM/YTC shown are indicative only and subject to market conditions, price fluctuations, and final trade execution. For bond pricing, further information, and available offerings, please contact bonds@phillip.com.sg

Our Credit View

Koh Brothers’ credit profile improved in FY25, supported by stronger construction execution and stronger credit metrics. However, key watchpoints remain the sustainability of core earnings beyond one-off gains.