Company at a Glance

What the company does:

Seatrium is an engineering, procurement and construction (EPC) contractor for offshore energy infrastructure. Its core products include floating production storage and offloading units (FPSOs), offshore wind substations, and gas-related assets such as FSRUs and FLNG units. The group operates a global yard network across Singapore, Brazil and China, serving key markets in Latin America, Europe, Asia and the Middle East. The group generates revenue by designing, fabricating and integrating these assets for customers under project-based contracts, with payments received progressively based on construction milestones.

Major Shareholders: Temasek Holding (36.6%); DBS Group (6.1%)

Main income source:

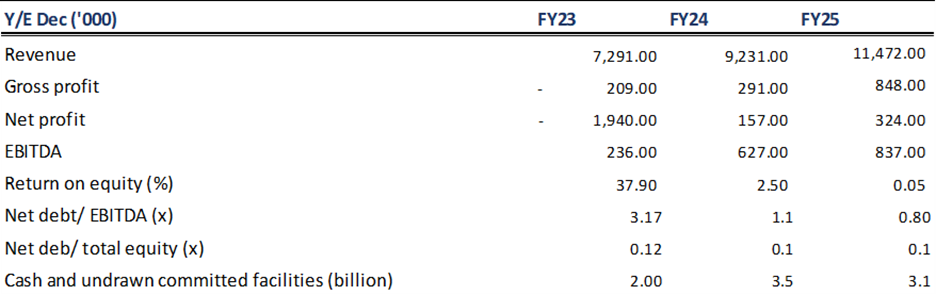

Seatrium’s core income is overwhelmingly driven by large EPC contracts under its “Rigs & Floaters, Repairs & Upgrades, Offshore Platforms and Specialised Shipbuilding” segment, which contributed virtually all group revenue in FY25 at S$11.41bn out of total S$11.47bn. Within this, the single largest revenue driver was ship and rig building or conversion at S$8.09bn, accounting for about 70% of total group revenue, mainly from FPSOs, FSRUs, FLNGs and other offshore energy assets. Offshore platforms contributed S$2.14bn (~19%), while repairs and maintenance added S$840mn (~7%). This means Seatrium’s earnings are still primarily dependent on execution of large offshore fabrication and conversion projects rather than recurring repair work.

What Supports the Credit Profile

Stronger revenue and margin recovery

FY25 revenue up 24% YoY to S$11.5bn, EBITDA rising 34% YoY to S$837mn, and gross margin improving sharply to 7.4% from 3.1%. Performance was driven by stronger execution on Petrobras FPSOs P-84 and P-85, lifting oil and gas revenue from S$6.6bn to S$8.1bn, alongside offshore wind growth from S$1.3bn to S$2.1bn from HVDC projects Beta, Gamma and Nederwiek 2.

Legacy risk is declining

Legacy contracts inherited from former Sembcorp Marine now account for only ~1% of Seatrium’s backlog, as most major lower-margin US projects have largely been delivered. These contracts had previously weighed on earnings through weaker pricing, COVID-related delays and cost overruns that drove sizeable provisions. With legacy exposure now largely phased out, provision risk is expected to decline from FY26 onward, supporting improved earnings stability.

Source: Seatrium Presentation Slides

Source: Seatrium Presentation Slides

Multi-year revenue visibility

Net order book stands at S$17.8bn (~1.5x FY2025 revenue), while ~95% now comprises Series Build projects, which are more repeatable and standardised, supporting better cost control and lower overrun risk. At the same time, Seatrium’s divestment and monetisation programme is expected to unlock >S$330m of cash by FY26, with a further >S$200m of non-core assets still earmarked for divestment, thereby strengthening liquidity.

Credit metrics improved with low leverage and strong liquidity

Net debt remained stable at S$0.68bn (FY24: S$0.69bn), while net leverage improved to 0.8x from 1.1x. Net gearing remained low at 0.1x, with all assets unencumbered. Liquidity is strong, with S$3.1bn in cash and undrawn committed facilities, providing ample headroom for working capital and project execution. Cost of debt declined to 3.4% (FY24: 4.9%), with average maturity of debt extended to 30 months (FY24: 29 months).

Main Areas to Monitor:

1) FY25 margin gains were supported partly by contingency releases and project milestone progression, which may not fully repeat. The key credit question is whether Seatrium can sustain stronger margins through structurally better execution and utilisation, rather than temporary project-specific tailwinds.

2) Legacy risk has reduced, but it is not fully extinguished. The sharp decline in pre-merger non-core legacy exposure is clearly positive, though recent project delays, such as NApAnt, and unresolved matters, such as P-52, indicate that legacy-related volatility has diminished rather than disappeared entirely.

Financial Overview

Source: Seatrium, Bloomberg

Source: Seatrium, Bloomberg

Seatrium SGD Bond Opportunities

* YTM/YTC shown are indicative only and subject to market conditions, price fluctuations, and final trade execution. For bond pricing, further information, and available offerings, please contact bonds@phillip.com.sg

* YTM/YTC shown are indicative only and subject to market conditions, price fluctuations, and final trade execution. For bond pricing, further information, and available offerings, please contact bonds@phillip.com.sg

Our Credit View

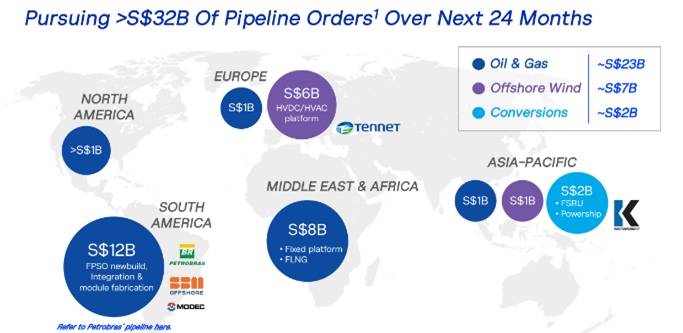

Seatrium’s FY25 results reinforce growing confidence in its post-merger recovery, supported by improving project execution and lower legacy drag. However, sustaining the current revenue scale remains dependent on continued project wins and the successful conversion of its S$32bn pipeline.