Company at a Glance

What the company does:

Perennial Holdings (PREHSP) is a Singapore-based real estate and healthcare platform with operations across China, Singapore, Malaysia, and Ghana, with China remaining its core market. The group combines property ownership, development, and healthcare operations, positioning itself to capture both asset value and long-term healthcare demand. Its shareholder base includes Kuok Khoon Hong (29%), Wilmar International (16%), Hopu Investments (14%), Perpetual Capital (11%), Ron Sim (13%), Bangkok Bank (9%), and Pua Seck Guan (8%).

Main income source:

PREHSP’s revenue increased from S$287.7mn in FY2024 to S$384.6mn in FY2025 (+33% YoY), driven mainly by the healthcare segment, which contributed approximately 56% of total revenue. Around 60% of healthcare revenue comes from partnership-based models, in which the group collaborates with doctors and earns a combination of fees and profit-sharing.

What Supports the Credit Profile

The group owns a sizeable asset base, including key Singapore assets such as CHIJMES, Capitol Singapore and Golden Mile valued at ~S$4.8bn, alongside China healthcare developments in Tianjin, Chengdu, Kunming and Xi’an at ~RMB56bn. These assets can monetised if required. Management has guided ongoing capital recycling initiatives, including a China C-REIT spin-off (target Sep 2026) and the potential disposal of Capitol Singapore.

From a growth perspective, PREHSP is exposed to a high-demand yet underpenetrated private healthcare market, with only ~0.9% of patients currently using private healthcare despite ~47% of the population being able to afford it (based on management data). The group has a visible pipeline (~88%) concentrated in Tier 1 and quasi-Tier 1 cities such as Tianjin, Chengdu and Kunming, with total capacity expected to exceed ~37,000 beds. Its doctor partnership model, together with proven execution (e.g. Chengdu achieving breakeven within ~12 months), supports faster ramp-up and utilisation.

Main Areas to Monitor:

EBITDA declined sharply to S$47.5mn (vs S$223.6mn in FY2024), mainly due to the absence of fair value gains, and remains below FY2023 levels (S$146.8mn), where earnings were similarly supported by such gains. This suggests that the underlying operating performance is still in the ramp-up phase. Management has guided that Tianjin is expected to reach breakeven in 2026, which should support further earnings growth.

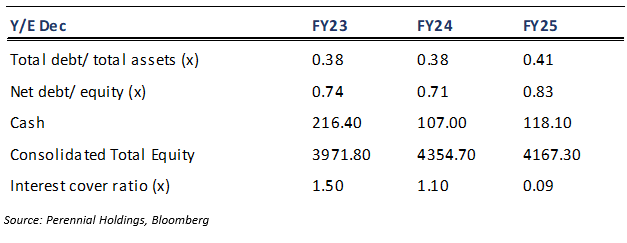

Credit metrics remain weak. Approximately S$1.29bn of debt is maturing in 2026, with leverage rising (debt/assets: 0.38x to 0.41x; net debt/equity: 0.71x to 0.83x). Interest coverage declined sharply from 1.10x to 0.09x, highlighting weak debt servicing capacity and continued reliance on refinancing and asset monetisation.

Financial Position

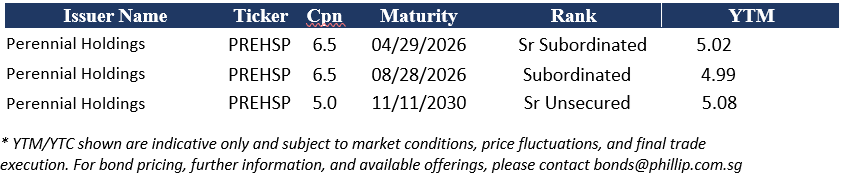

PREHSP SGD Bond Opportunities

Our Credit View

We are neutral on PREHSP’s credit profile, supported by strong structural demand, a visible Tier 1 pipeline, and demonstrated execution (e.g. Chengdu breakeven within ~12 months; Tianjin expected breakeven in 2026). The group also benefits from a sizeable asset base (~S$4.8bn in Singapore; ~RMB56bn in China), which provides monetisation flexibility. Management is actively executing capital recycling initiatives, including a China C-REIT (target Sep 2026) and asset divestments (e.g. Capitol Singapore). However, the credit profile remains constrained by it sharply deteriorated interest coverage of ~0.09x in FY2025.