Apart from the bigger listed banks in France, such as Credit Agricole, BNP Paribas, and Societe Generale, did you know that there is one other bank that is just as large, except that it is not listed on the exchange.

Company Overview

Groupe Banque Populaire Caisse d’Epargne or “Groupe BPCE” is a combination of two major retail banking networks Banque Populaire and Caisse d’Epargne. So, what is Banque Populaire and Caisse d’Epargne? Banque Populaire is a French group of cooperative banks, with origins in the European cooperative movement, while Caisse d’épargne is also a French semi-cooperative commercial banking group based out of Paris, France.

Groupe BPCE is the 2nd largest banking group in France, and Natixis, which was previously a subsidiary of Groupe BPCE and listed on the Euronext Paris stock exchange, was delisted in 2021 and was brought under full ownership of the group. To have an idea of the size of Groupe BPCE’s operations, the group held EUR1.544 trillion of assets at the end of 2023, alongside EUR84.9b of shareholder equity, and the group’s consolidated net income for FY2023 was EUR2.8b. The group’s main business sectors include Retail Banking & Insurance (66.8%), Global Financial Services (32.6%), and Corporate Center (0.6%), which contribute to its net banking income in FY2023, respectively. BPCE also has a credit rating of Long & Short Term A+/Aa3/A+ from (Fitch/Moody’s/S&P).

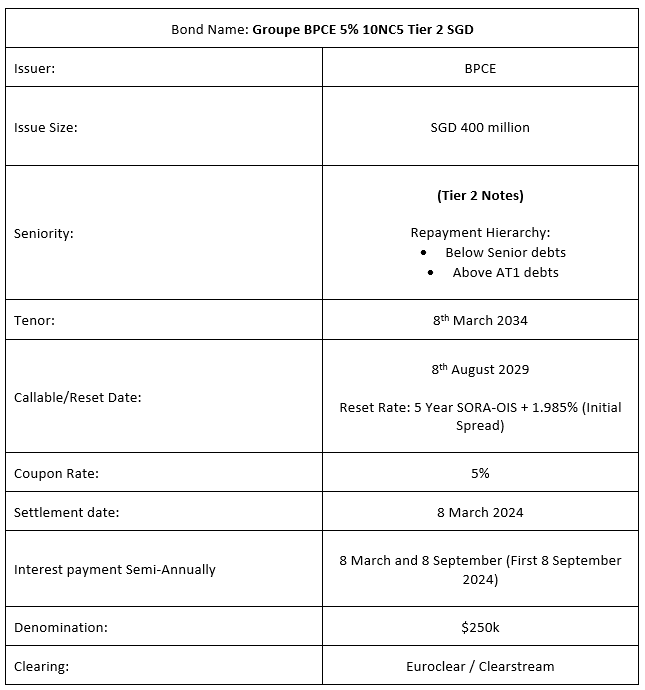

BPCE 5% 10NC5 Tier 2

Groupe BPCE recently announced the issuance of its 10NC5 Tier 2 notes at a final price guidance of 5%. These bonds will be callable on 8 March 2029 and every interest payment date thereafter. In the event the notes are not recalled by 8 March 2029, the bonds will then be reset at the prevailing Mid-Market Swap Rate (5-year SORA-OIS) plus the initial margin of 1.985%. These bonds come with a semi-annual coupon payment scheduled on the 8th of March and the 8th of September each year, with the first coupon payment commencing on the 8th of September 2024. The expected rating for this issuance is Baa2/BBB/BBB+ (Moody’s/S&P/Fitch).

Groupe BPCE FY2023 Financials

In FY2023, the group’s net banking income decreased 7% Y.o.Y from EUR23.9bn in FY2022 to EUR22.1bn in FY2023. This decline was mainly due to the higher interest rate payment that BPCE had to pay on deposits and other forms of borrowed funds, which has led to a strain on their profit margins. Despite the decline in net banking income, the group’s cost-saving initiatives, such as optimizing internal processes and streamlining operations, have reduced its operating expense by 2% Y.o.Y from EUR16.6bn in FY2022 to EUR16.3bn in FY2023. Regarding the provisions set aside by the group for potential loan losses, a positive development was seen as cost of risk for BPCE has come down from 24bps in the previous year to 20bps in FY2023 reflecting stricter credit risk control.

Moving on to its capital strengths, BPCE has further beefed up its solvency in FY2023, with its CET1 coming in at 15.6% in FY2023, an increase from 15.1% from FY2022 and this is also above the European Central Bank’s requirement of 10.46%. Similarly, the group’s liquidity coverage ratio (LCR) has also improved from the previous year, from 139% to 143% in FY2023, 43% well above the regulatory requirement as well. BPCE also currently also has a liquidity reserve of EUR302bn as of FY2023 and a coverage ratio of a short-term debt obligation of 161%. BPCE management has also indicated that the loans that were provided by the ECB (TLTRO III) totaling EUR15.7bn will also be repaid in 1Q2024.

Capital Buffer between the major French players

Although BPCE may not be a listed bank on the European market, in terms of scale and liquidity, it is competing head and shoulders with its peers in the industry. As for the new issuance, it is priced slightly more attractive at 5% FPG as compared to Credit Agricole’s 5.25%, 7 September 2033 which is currently trading at a yield of 4.55%. BNP Paribas’s 4.75%, 15 February 2034, is currently trading at a yield of 4.68%.

Bond Overview