DAILY MORNING NOTE | 29 July 2022

Nasdaq 100 contracts added more than 1% after the US stock market hit a seven-week high Thursday. Amazon jumped over 10% in extended trading, while Apple also advanced, after their revenues beat estimates.

Futures suggest brighter sentiment will lift bourses in Japan and Australia. But Hong Kong may have a muted start after a call between US President Joe Biden and Chinese President Xi Jinping underlined bilateral tension even as the leaders told aides to plan an in-person meeting.

A Treasuries rally drove the 10-year yield to the lowest since April. Bonds jumped on data showing a technical US recession, which bolstered the view that high inflation will cool and that the Fed will become less aggressive.

A dollar gauge retreated, oil topped $97 a barrel and gold held gains. Bitcoin breached $24,000 before slipping back.

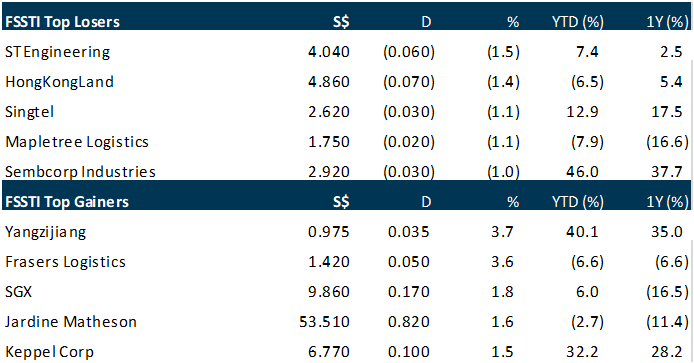

Stocks to watch: Keppel Corporation

SG

Jardine Matheson on Thursday (Jul 28) reported a 22 per cent increase in H1 2022 underlying net profit to US$747 million from US$615 million a year ago. In a regulatory filing after market close, the conglomerate also announced a 4 per cent rise in revenue for the period to US$18.2 billion from US$17.5 billion a year ago. The growth in revenue was driven by Astra’s performance, Jardine Cycle & Carriage and Hongkong Land’s improved underlying profit. Mandarin Oriental also delivered a lower underlying loss for H1. This resulted in Jardine Matheson reporting earnings of US$423 million in the first half, reversing a loss of US$117 million in 1H 2021. South-east Asia contributed to the bulk of the conglomerate’s profit at 58 per cent, while 37 per cent came from China in H1. The directors have declared an interim dividend of US$0.55 per share, up 25 per cent from a year ago.

Conglomerate Keppel Corporation on Thursday (Jul 28) posted a headline net profit of S$497.5 million for the first half of the year ended June, up 65.9 per cent from its earnings of S$299.8 million in the corresponding year-ago period. The group said this was underpinned by profitability across all its segments, including the discontinued offshore and marine operations. On a per-share basis, this translated to earnings of S$0.279, up 69.1 per cent year on year from S$0.165. Net profit from continuing operations rose 26.4 per cent to S$434.1 million from S$343.5 million in the year-ago period.

Sheng Siong Group posted a 2.2 per cent year-on-year increase in net profit to S$67.4 million in the first half of 2022, despite a marginal decline in revenue that the supermarket chain said was related to a lifting of Covid-19 measures. Revenue fell 0.7 per cent year on year to S$676.8 million for the 6 months ended Jun 30, as restrictions were eased in the second quarter, the company said. “This led to increased outdoor dining and overseas travel, especially during the June school holidays, which in turn returned sales revenue to more normalised pre-pandemic levels,” Sheng Siong said. “As Singapore moves towards endemic living with Covid-19, we expect the elevated demand that persisted throughout 2020 and 2021 to continue to taper to a new normal,” it added.

Starhill Global Reit reported a 1.8 per cent increase in distributable income for FY2021/22 to S$89.8 million from S$88.2 million. In a regulatory filing after market close on Thursday (July 28), the Reit reported a 2.8 per cent increase in revenue for the period to S$186.4 million from S$181.3 million. Net property income for FY2021/22 rose in tandem, up 7.4 per cent to S$144.7 million from S$134.7 million. The growth in net property income was driven by the cessation of rental rebates in Malaysia, lower rental assistance for eligible tenants and lower operating expenses. This was partially offset by lower rental contribution from Wisma Atria in Singapore. Distribution per unit for FY2021/22 dropped 3.8 per cent to S$0.038 due to the deferred distributable income for H2 FY2020/21. Excluding that deferred amount, the distribution per unit would have increased 5.6 per cent instead.

Agri-food company Japfa on Thursday (Jul 28) reported a 10.4 per cent increase in 1H 2022 revenue to US$2.5 billion from US$2.3 billion a year ago. However, net profit attributable to shareholders for the period fell 62.9 per cent to US$44 million from US$118.5 million in 1H 2021. Earnings were dragged by high feed raw material costs and the impact of Covid-19 at the beginning of 2022, with lower broiler prices in February 2022. Operating profit for H1 fell 36.9 per cent to US$171 million from US$270.9 million in 1H 2021. Operating profit margin in H1 also dropped 5.2 percentage points to 6.8 per cent from 12 per cent in 1H 2021.

Jardine Cycle & Carriage (Jardine C&C) has reported an improved H1 2022 underlying profit attributable to shareholders of US$522 million, a 51 per cent increase from US$346 million in H1 2021. The directors of Jardine C&C have also declared an interim dividend of US$0.28 per share for H1 2022. Revenue for the period rose 29 per cent to US$10.7 billion from US$8.2 billion. Earnings for H1 2022 surged 115 per cent to US$487 million from US$226 million on higher contributions from its subsidiaries, Astra and THACO. Astra is an Indonesian conglomerate; THACO manufactures, assembles, distributes and sells automotives in Vietnam. Astra contributed US$465 million to H1 2022 underlying profit, up 58 per cent from US$293 million in H1 2021. This was driven by a stronger performance from all its businesses, and particularly its automotive, financial services, heavy equipment and mining operations.

Singapore Airlines (SIA) reported a Q1 FY2022 ending June 30 operating profit of S$556 million, reversing into the black on soaring air travel demand. This is SIA’s second highest quarterly operating profit since Q3 FY2007/08. Earnings for the period likewise reversed into a profit of S$370 million. The Singapore carrier’s group capacity has jumped from a average 47 per cent of pre-pandemic levels in Q4 FY2021/22 to 61 per cent in Q1 FY2022/23.

Hongkong Land on Thursday (Jul 28) reported an 8 per cent rise in 1H 2022 underlying net profit to US$425 million from US$394 million a year ago. The property company also reversed into the black, with H1 earnings of US$292 million, compared to a loss of US$865 million a year ago. Hongkong Land directors have declared an interim dividend of US$0.06 per share. Revenue for the first half rose slightly by 0.9 per cent to US$894 million from US$885.8 million. Rental income for the period dipped 3 per cent from US$469.8 million to US$455.6 million on negative rental reversion from portfolio properties in Hong Kong. Average office rents dropped to HK$112 per sq ft in the first half of 2022, from HK$115 per sq ft in 2H 2021.

The manager of Digital Core Reit (DC Reit) on Thursday (Jul 28) reported a distribution per unit (DPU) of US$0.0206 for the first half of 2022, a performance that slightly missed the mark. The pure-play data centre real estate investment trust (Reit) made its trading debut on the Singapore Exchange on Dec 6, 2021, and at the time, it had forecasted a DPU of US$0.0209 for the half year ended Jun 30, according to its interim financial statements. Together with a DPU of US$0.0031 for the stub period Dec 6-31, 2021, a total DPU of US$0.0237 will be paid to unitholders on Sep 28, the manager said.

US

Pfizer on Thursday (Jul 28) reported a 78 per cent jump in profit and reaffirmed the combined 2022 sales forecast of US$54 billion for its Covid-19 vaccine and pill, as countries rushed to sign contracts to prepare for a surge of cases in the fall season. Shares rose 1.8 per cent in premarket trading as overall net income rose to US$9.91 billion despite a stronger US dollar, thanks to strong demand for the vaccine as well as its antiviral treatment Paxlovid. Demand for the pill, which was used by President Joe Biden during his bout of Covid-19 infection, has picked up recently in the United States and other countries due to fresh outbreaks.

The US dollar rebounded across the board on Thursday (Jul 28) as investors digested the implications of the Federal Reserve’s (Fed) latest comments on the future path of interest rates while the euro slumped broadly as the region’s economic outlook darkened. Traders interpreted the Fed’s decision to drop its commitment to guide markets on the future rate trajectory after a widely expected 75 bps hike as a sign that policymakers may soften their stance, pushing the US dollar lower. But the greenback rebounded broadly in midday London trading as traders cut some of those bets on worries that other economies, notably Europe and China, will continue to struggle in the short term, benefiting US dollar-based assets.

Billionaire Jack Ma plans to relinquish control of Ant Group, Dow Jones reported, citing people familiar with the matter said, part of the fintech giant’s effort to appease regulators following a lengthy crackdown. With Ma giving up control, a revival of Ant’s initial public offering (IPO) could be put back another year or more, Dow Jones reported, citing Chinese securities regulations that require a timeout on public listings for companies that have gone through a change in control. Ma, who doesn’t hold any titles at Ant, currently controls 50.52 per cent of voting rights in the company. He could transfer some of his voting power to other Ant officials including chief executive Eric Jing, Dow Jones cited the people as saying.

The drumbeat of recession grew louder after the US economy shrank for a second straight quarter, as decades-high inflation undercut consumer spending and Federal Reserve interest rate hikes stymied businesses and housing. Gross domestic product (GDP) fell at a 0.9 per cent annualised rate after a 1.6 per cent decline in the first 3 months of the year, the Commerce Department’s preliminary estimate showed on Thursday (Jul 28). Personal consumption, the biggest part of the economy, rose at a 1 per cent pace, a deceleration from the prior period.

Applications for US unemployment insurance fell for the first time in 4 weeks but held near the highest level since November, indicating continued moderation in the labour market. Initial unemployment claims decreased by 5,000 to 256,000 in the week ended Jul 23, Labor Department data showed on Thursday (Jul 28). The median estimate in a Bloomberg survey of economists called for 250,000 applications. Continuing claims for state benefits fell to 1.36 million in the week ended Jul 16.

Gold climbed after the US economy shrank for a second consecutive quarter, pushing the US dollar and Treasury yields lower, and clouding the outlook for further aggressive interest rate hikes as the Federal Reserve fights inflation. Bullion rallied as much as 1.2 per cent to a 3-week high after a report on Thursday (Jul 28) showed that US gross domestic product (GDP) fell 0.9 per cent in the second quarter as inflation weighed on consumer spending. The Fed raised rates by 75 basis points on Wednesday, and chairman Jerome Powell said while a similar move was possible again, the pace of hikes will slow at some point.

Source: SGX Masnet, The Business Times, Bloomberg, Channel NewsAsia, Reuters, CNBC, PSR

RESEARCH REPORTS

Alphabet Inc – Business resilient through macro uncertainty

Recommendation : BUY (Maintained); TP: US$139.00, Last Close: US$113.06

Analyst: Jonathan Woo

• 2Q22 revenue in line, but misses on earnings. 1H22 revenue/PATMI at 45/36% of our FY22e forecasts.

• Cloud continues to push ahead – 2Q22 revenue was at US$6.3bn, 35% YoY growth.

• Earnings miss was due to FX headwinds, and a one-off unrealized loss in debt/equity investments of -US$1.0bn for 2Q22.

• We lower our FY22e earnings forecast to account for the higher-than-expected unrealized loss, and also slightly increase expenses associated with investments in IT infrastructure. We maintain a BUY recommendation with a lowered DCF target price of US$139.00 (prev. US$144.00).

Upcoming Webinars

Guest Presentation by SATS [NEW]

Date: 4 August 2022

Time: 2.30pm – 3.30pm

Register: https://bit.ly/3IXysX5

Guest Presentation by Prime US REIT

Date: 4 August 2022

Time: 3.30pm – 4.30pm

Register: https://bit.ly/3uYlNgS

Guest Presentation by Pan-United Corporation Limited

Date: 5 August 2022

Time: 11am – 12pm

Register: https://bit.ly/3OFbJ41

Guest Presentation by A-Sonic Group

Date: 11 August 2022

Time: 12pm – 1pm

Register: https://bit.ly/3PmoIrl

Guest Presentation by Marathon Digital Holdings

Date: 18 August 2022

Time: 10am – 11am

Register: https://bit.ly/3yNSfUu

Guest Presentation by Audience Analytics

Date: 23 August 2022

Time: 12pm – 1pm

Register: https://bit.ly/3P3eBYR

Guest Presentation by Meta Health Limited (META)

Date: 24 August 2022

Time: 12pm – 1pm

Register: https://bit.ly/3nYZXWx

POEMS Podcast:

Research Videos

Weekly Market Outlook: Netflix, SembCorp, SATS Ltd, Sabana REIT, FAANGM Monthly, SG Weekly…

Date: 25 July 2022

Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Phillip Research in 3 minutes: #29 Keppel Corporation; Initiation

Click here for more on Phillip in 3 mins.

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials