ComfortDelGro Corp Ltd - Higher pricing supporting margins

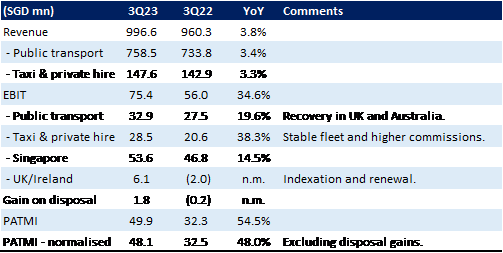

16 Nov 2023- 3Q23 normalised PATMI jumped 48% YoY to S$48mn and was within our expectations. Revenue was softer than expected. 9M23 revenue and PATMI were 73% and 78% of our FY23e forecast.

- Earnings growth was driven by a turnaround in the UK bus operation and growth in Singapore taxi operations. UK benefited from higher pricing through contract indexation and renewal. Singapore taxi margins expanded with platform fees.

- We lower our FY23e revenue by 4% and PATMI is maintained. Our BUY recommendation and DCF target price of S$1.57 is unchanged. Earnings momentum will be sustained by higher bus service fees in the UK, taxi platform fees in Singapore and lagged pricing of rail services in Singapore.

Source: Company, PSR #Note – Only selected financials are provided in the 3Q23 update.

The Positive

+ UK operations turnaround. A major part of earnings growth in 3Q23 was the turnaround in UK operations. From an operating loss of S$2mn, UK swung to a S$6mn profit. Around 70% of the routes have been re-indexed. Another boost to margins will be re-contracting of the bus contract routes that can expire up to 5 years. Recent re-contracting has seen a significant improvement in margins.

The Negative

– Rail profitability is still weak. We believe profitability in Singapore rail remains weak despite the jump in passenger traffic. Rail operations are burdened by the higher electricity and a lagged re-pricing of fares. The next round of higher fares will be in December this year.

Outlook

We expect earnings growth to sustain into FY24e, supported by re-pricing of bus contracts in the UK, improvement in bus efficiency in Australia as drivers return, platform fees raising taxi margins and higher fares driving up Singapore rail profitability. Taxi operations in Singapore have seen a resurgence in competitive pricing by other platforms but Comfort’s taxi fleet has remained stable with market share rising.

Maintain BUY with an unchanged TP of S$1.57

ComfortDelgro pays around 4.6% dividend yield, enjoys a net cash balance sheet of S$500mn and visibility of earnings recovery.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Phillip Macro Update - Key Points for May FOMC Meeting

Phillip Macro Update - Key Points for May FOMC Meeting Far East Hospitality Trust - Higher RevPAR by ramping up occupancy

Far East Hospitality Trust - Higher RevPAR by ramping up occupancy