ComfortDelGro Corp Ltd - Recovery building momentum from repricing

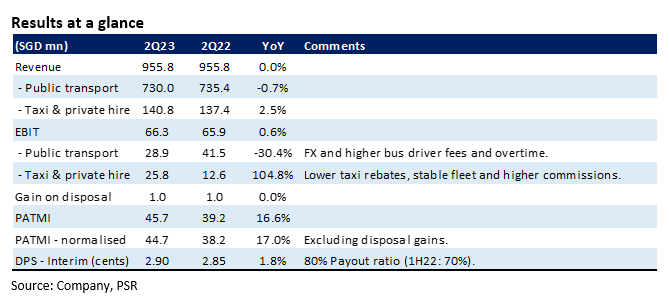

17 Aug 2023- 2Q23 results were within expectations. 1H23 revenue and PATMI were 45% and 47% of our FY23e forecast. PATMI grew 17% YoY to S$45mn as taxi earnings doubled.

- Public transport remains a drag on earnings from weaker foreign exchange and higher bus driver costs in the UK. We expect a strong rebound in earnings as bus contracts service fees in the UK are repriced higher from inflation indexing and more rational pricing.

- No changes to our FY23e forecast but we raised our FY23e DPS to 6.08 cents (prev. 5.3 cents), as the company increased their minimum payout ratio from 50% to 70%. Our BUY recommendation and DCF target price of S$1.57 is unchanged. The largest driver to earnings in 2H23 will be the repricing of services in the key public transport and taxi operations. We believe the key earnings driver in 2H23 include higher bus service fees in the UK, increased hiring of Australian bus drivers, the introduction of taxi platform fees in Singapore and lower taxi rental rebates in Singapore and China.

The Positives

+ Taxi profits doubled. 2Q23 margins improved with higher booking volumes, additional booking commissions, lower rebates in Singapore (15% to 10% from Apr23) and reduced taxi rebates and costs in China. Another driver to earnings has been a stable taxi fleet in Singapore. Comfort’s taxi fleet grew 0.8% YoY to 8,782, after several years of decline.

+ Cash piling up and returning to shareholders. Comfort continues to generate healthy free-cash-flows (FCF). 1H23 FCF was S$86.4mn (1H22: S$88.5mn), pilling up the net cash to S$565mn. Capital expenditure is now trending at S$350mn p.a. compared to pre-pandemic S$450-500mn. Comfort has raised its minimum dividend payout ratio from 50% to 70%. We estimate S$131mn of dividends to be paid out this year.

The Negative

– Lethargic in margins for public transport. Public transport operating margin has been the weakest spot for Comfort. 2Q23 margins was 4%, an improvement over 3.4% in 1Q23 but far below pre-pandemic 8%. Bus operations across the UK, Australia and Singapore are depressing margins. The worst hit is the UK which reported an operating loss of S$0.5mn. A combination of irrational tendering activity and a spike in bus driver fees has negatively impacted margins. Australia is suffering from higher overtime salaries and other “running time” charges due to the lack of bus drivers.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Phillip Macro Update - Key Points for May FOMC Meeting

Phillip Macro Update - Key Points for May FOMC Meeting Far East Hospitality Trust - Higher RevPAR by ramping up occupancy

Far East Hospitality Trust - Higher RevPAR by ramping up occupancy