Alphabet Inc. - Focused on reducing expense base

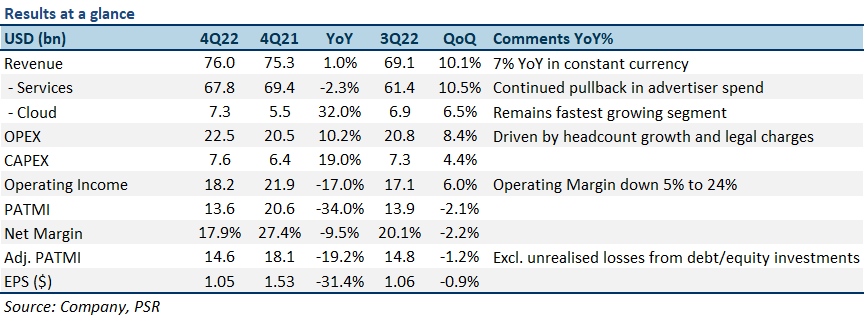

8 Feb 2023- 4Q22 results was within expectations on both revenue and earnings. FY22 revenue/PATMI is at 99%/95% of our FY22e forecasts. Adj. PATMI (excl. unrealised losses) is at 100% of our forecasts. Revenue was dragged by 2% YoY decline in ad revenue, and 6% FX headwinds.

- Cloud momentum is still strong with 32% YoY growth for 4Q22. But there was a -US$480mn operating loss. Cloud accounts for only 10% of total revenue.

- Slowing FY23e expenses growth with 12,000 job cuts in 1Q23e, reducing office facilities, and more prudent investments. Guidance for FY23e CAPEX is roughly in line with FY22

- We cut our FY23e revenue forecast by 9% to account for continued weakness in digital advertising demand, while reducing CAPEX spend by 20% to reflect a general slowdown in expenses. Our FY23e EBITDA forecasts are also cut by 17% to reflect slower-than- anticipated margin expansion due to expected US$2.3bn severance-related charges. We maintain BUY with a raised DCF target price of US$131.00 (prev. US$124.00) due to potential upside from increasing YouTube Shorts monetisation, continued strength in Cloud, and margin expansion in FY24e from the slowing pace of expense growth as a % of revenue, with a WACC of 7.3% and terminal growth of 3.5%.

The Positives

+ Google Cloud momentum still strong, with profitability in focus. Cloud remained GOOGL’s fastest growing segment, increasing 32% YoY to US$7.3bn as customers continue to leverage on Cloud’s AI/Infrastructure/Cybersecurity offerings. Cloud continues to operate in the red, with a 4Q22 operating loss at -US$480mn, although management spoke about its focus on making Cloud profitable sooner rather than later.

+ Slowing expense growth guided moving forward; FY23e CAPEX in line with FY22. Management remains committed to slowing expense growth moving forward; guiding FY23e CAPEX to be at similar levels with FY22 as it consolidates office facilities, offset by continued investments in tech infrastructure. GOOGL also announced the reduction of around 12,000 jobs (~6% of workforce) in 1Q23e as it looks to reduce some of its fixed costs, and will remain prudent and more selective when making investment decisions. FY23e operating margins are still expected to remain relatively similar compared with FY22 at around 27% due to consolidation and severance-related charges, but to expand more meaningfully in FY24e.

The Negative

– Headline earnings missed on weakness in advertising demand, inventory charges, and FX drag. 4Q22 revenue of US$76bn missed estimates marginally by US$440mn, dragged down by a 2% YoY decline in services (advertising) revenue; and a 6% FX headwind. Headline earnings also missed due to higher-than-expected inventory charges of US$1.2bn; and a US$1.5bn unrealised loss on debt/equity investments.

About the author

Jonathan Woo

Research Analyst

PSR

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.

About the author

Jonathan Woo

Research Analyst

PSR

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.

Phillip Macro Update - Key Points for May FOMC Meeting

Phillip Macro Update - Key Points for May FOMC Meeting Far East Hospitality Trust - Higher RevPAR by ramping up occupancy

Far East Hospitality Trust - Higher RevPAR by ramping up occupancy