Singapore Banking Monthly – Loans and interest rates dip further

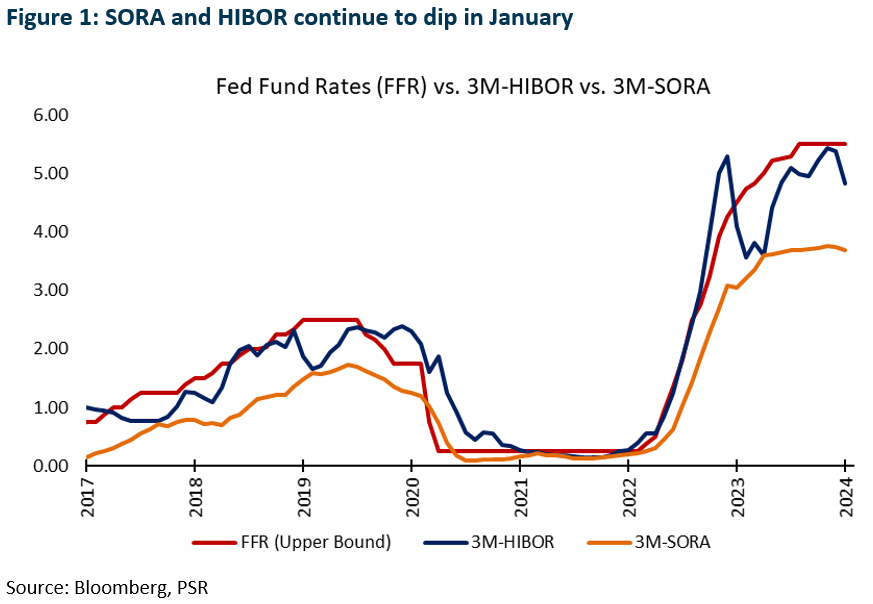

19 Feb 2024- January’s 3M-SORA was down 5bps MoM to 3.69% and was 5bps lower than the 4Q23 average. This is the largest MoM decline since July 2020. 3M-HIBOR was down 55bps MoM to 4.82%, the largest MoM decline since January 2023.

- Singapore domestic loans dipped 2.4% YoY in December, below our estimates. The loan decline was the smallest decline recorded in 11 months. The CASA balance was maintained at 18.5% (Nov23: 18.5%).

- Maintain OVERWEIGHT. All three banks declined in January. The worst performer was DBS with a 4.6% decline. We remain positive on banks. NIMs may see flat growth despite the higher-for-longer interest rate environment, but a recovery in loan growth and fee income will uplift profits. Bank dividend yields are also attractive with upside surprises due to excess capital ratios and a push towards higher ROEs.

3M-SORA and 3M-HIBOR decline continues in January

Singapore interest rates dipped in January, the largest MoM decline since July 2020. The 3M-SORA was down 5bps MoM to 3.69%. Nonetheless, January’s 3M-SORA rose by 64bps YoY but was 5bps lower than the 4Q23 3M-SORA average of 3.74% (3Q23: 3.69%).

Hong Kong interest rates declined in January. The 3M-HIBOR was down 55bps MoM to 4.82%, the largest MoM decline since January 2023. Nonetheless, January’s 3M-HIBOR improved by 72bps YoY but was 52bps lower than 4Q23 3M-HIBOR average of 5.34% (Figure 1).

Singapore loan growth decline flattens

Overall loans to Singapore residents – which captured lending in all currencies to residents in Singapore – fell by 2.44% YoY in December to S$794bn. This was below our estimate of low-single-digit growth for 2023 as the rise in interest rates started to be fully felt by consumers. Nonetheless, this is the smallest decline recorded in 11 months.

Business loans fell by 3.92% YoY in December. Loans to the building and construction segment, the single largest business segment, fell 0.27% YoY to S$168bn, while loans to the manufacturing segment fell 13.4% YoY in December to S$22.5bn.

Consumer loans were flat YoY in December to S$313bn, as dips in other segments were offset slightly by strong loan demand in the housing segment. Housing loans, which comprise ~70% of consumer lending, grew 1.34% YoY in December to S$226bn for the month.

Total deposits and balances – which captured deposits in all currencies to non-bank customers – grew by 4.29% YoY in December to S$1,790bn. The Current Account and Savings Account, or CASA proportion, was maintained at 18.5% (Nov23: 18.5%) of total deposits, or S$331bn.

Hong Kong loan growth decline flattens

Hong Kong’s domestic loan growth declined 3.58% YoY and was flat MoM in December. The YoY decline in loan growth for December was lower than the decline of 4.30% in November 2023, and the MoM decline was lower than the decline of 0.46% in November 2023.

Volatility fell as the market stabilised

SDAV for January dipped 20% YoY to $924mn (Figure 4), while the DDAV grew 5% YoY and 10% MoM in January. The VIX, a market index that measures the implied volatility of the S&P 500 Index, averaged 13.4 in January, up from 12.7 in the previous month. This is the second lowest the VIX has reached since Dec 2019.

The top four equity index futures turnover saw an increase of 22% YoY in January to 12.96mn contracts (Figure 5) due to the higher trading volumes of its FTSE China A50 Index Futures and FTSE Taiwan Index Futures. Notably, the FTSE China A50 Index Futures increased 25.6% MoM, while the Nikkei 225 Index Futures fell 22% MoM in January.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

May 17th - Things to Know Before the Opening Bell

May 17th - Things to Know Before the Opening Bell Trade of the Day - Boeing Co. (NYSE: BA)

Trade of the Day - Boeing Co. (NYSE: BA) Singapore Banking Monthly - Fee income the driver

Singapore Banking Monthly - Fee income the driver May 16th - Things to Know Before the Opening Bell

May 16th - Things to Know Before the Opening Bell