FIRST SPONSOR GROUP LIMITED (Initiation)- Your financier, developer and landlord

21 Sep 2020- Unrecognised property development revenue of S$586mn with another S$1.95bn worth of gross development value (GDV) to be unlocked, equivalent to 5 years of sales.

- Property financing loan book grew at 19% CAGR in the past 5 years. These securitised loans offer recurring income at low to mid-teens returns. We are estimating loan book growth of around 8% for FY20e and FY21e.

- Initiate coverage with BUY and target price of S$1.65.

The report is produced by Phillip Securities Research under the ‘Research Talent Development Grant Scheme’ (administered by SGX).

Company Background

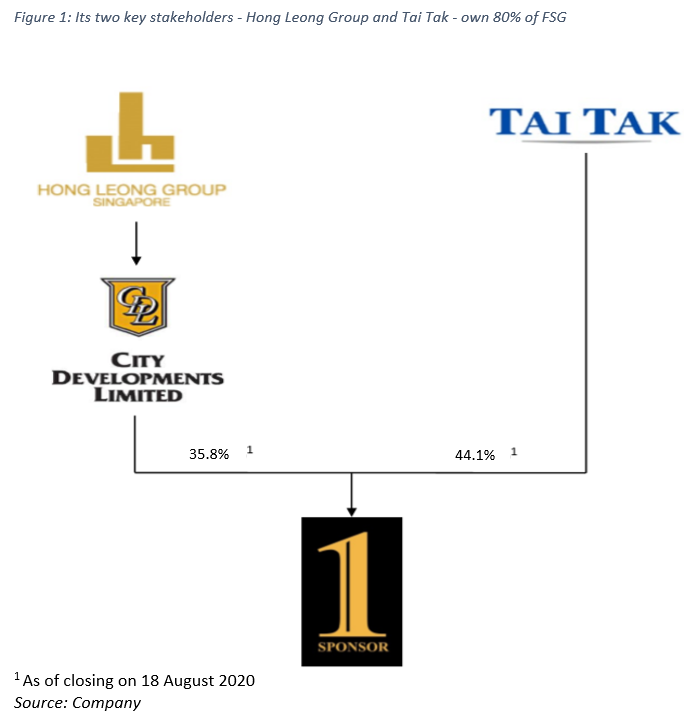

Listed on the mainboard of the SGX on 22 July 2014, First Sponsor Group (FSG) is a property developer (FY19 revenue: 50%), owner (22.5%) and financier (27.5%). It operates in China (FY19 assets: 58%), Europe (40%) and Australia (2%). Hong Leong Group Singapore (35.8%) and Tai Tak Estates (44.1%) are its two controlling shareholders.

Investment Merits

- 1H20 unrecognised revenue equates to 1-2 years of sales; GDV to unlock is equivalent to 5 years of sales; demand for Dongguan’s residential properties exceeds expectations. Unrecognised revenue as of 1H20 from development properties amounted to S$586mn. FSG holds GDV of S$1.95bn that has yet to be unlocked. Buying sentiment in Dongguan exceeded FSG’s expectations after business resumed in late February 2020. Residential units at most of its projects that were launched in April have been almost fully sold. Another residential block in The Pinnacle was launched for pre-sales on 14 July and has sold more than 85%.

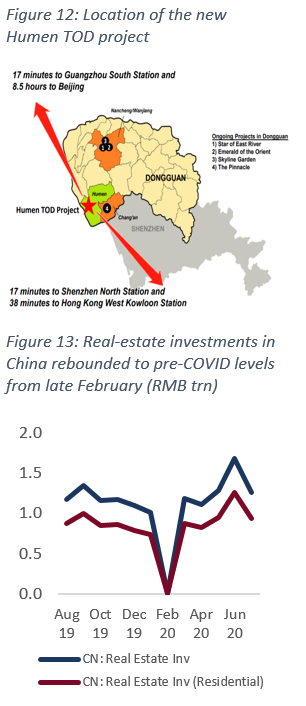

- Humen TOD to become one of FSG’s largest development projects. FSG won the bid for a mixed-use development on 29 June at RMB6.6bn (c.S$1.3bn) in a joint venture with China Poly Group (CPOLYZ CH, Not Rated) and China State Railway Group (390 HK, Not Rated). The land will be developed into a transit-oriented development with more than 1mn sqm Gross Floor Area (GFA). FSG has a c.17% effective equity interest in the JV.

- High recurring income for its Chinese property financing business plus double-digit growth in securitised loan book. FSG charges interest rates of low to mid-teens p.a. for its property financing business. LTV of its loan book is 40-60%. PRC loan book grew at a CAGR of 19% from 2015 to 2019. 1H20 loan book grew 12% YoY to RMB2,295mn (S$459mn). To date, FSG has not incurred any bad-debt losses in property financing. We are estimating loan book growth of around 8% for FY20e and FY21e.

Key risks

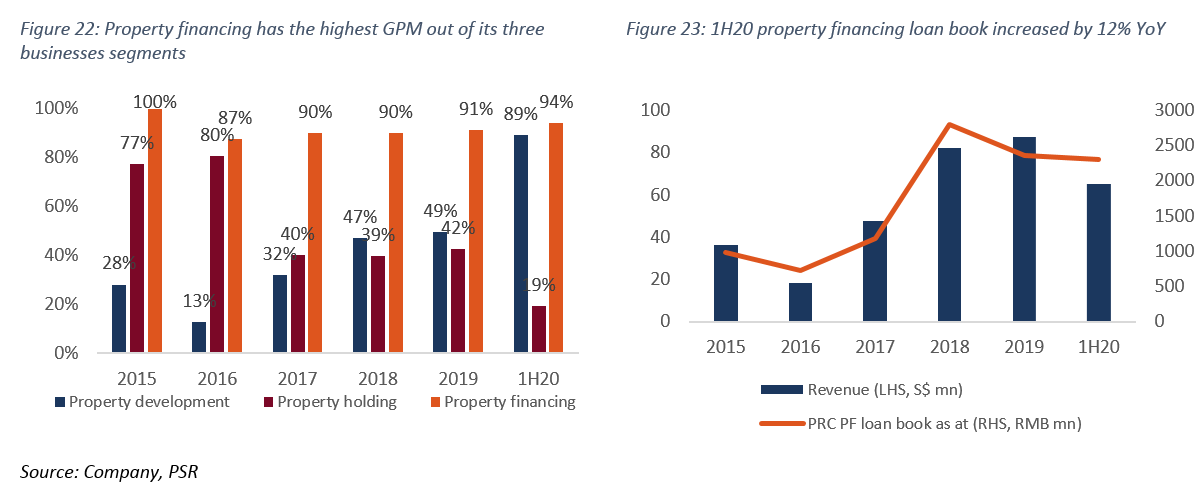

- Worst may not be over for the hotel portfolio; stunted recovery is expected. As of 30 June 2020, all temporarily closed hotels except Bilderberg Garden Amsterdam had re-opened. FSG’s well-diversified portfolio is situated in areas where most hotels saw a greater recovery in August (Netherlands portfolio ex-Amsterdam/Rotterdam and Germany). However, the Netherlands has seen a resurgence of Covid-19 cases lately as new cases in September exceeded its peak in April. We are expecting a stunted recovery for the hotel portfolio.

We initiate coverage with a BUY rating. Our target price is S$1.65, based on its historical 30% average discount to RNAV. This implies a potential total return of 33.6% and dividend yield of 1.75%.

About First Sponsor Group Limited

FSG has been listed on the mainboard of the SGX since 22 July 2014. The group is supported by controlling shareholders, the Hong Leong group of companies, through its shareholding interest in City Developments Limited (CIT SP, Current: S$8.09,TP: S$11.68), and Tai Tak Estates Sendirian Berhad, both recognised property-holding companies in Asia.

Hong Leong Group is a globally diversified company with gross assets of over S$40bn, owned by the Kwek family. It employs some 30,000 people around the world. The Group’s four core businesses are property development, hotels, financial services, and trade & industry.

Tai Tak is a family-owned (Ho family) private company incorporated in Singapore in 1954. It invests in a wide range of businesses, including plantations, listed and private equities, property holding and development. The Tai Tak family is one of the largest shareholders of United Overseas Bank (UOB SP, ACCUMULATE, TP: S$20.40). The family was a co-founder of the bank with the Wee family and was the second largest shareholder until the merger of UOB and Overseas Union Bank.

Revenue

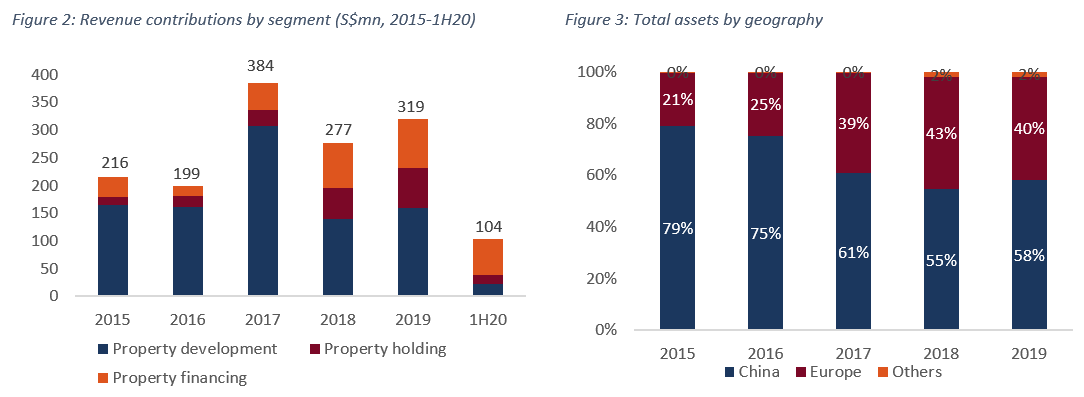

FSG has three operating segments: Property Development, Property Holding and Property Financing.

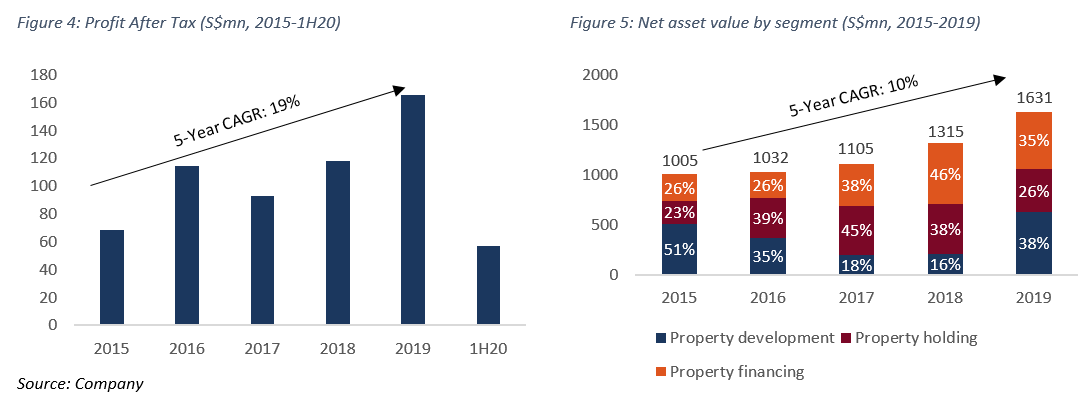

Property Development is historically its largest revenue contributor. In FY19, it contributed 50%, followed by Property Financing’s 27% and Property Holding’s 22%. The bulk of FSG’s income is derived from its operations and assets in the PRC (FY19: 58%) and Europe (40%). In 2015-2019, profit after tax and net asset value grew at CAGRs of 19% and 10% respectively. Property Financing has the highest gross profit margin (Fig. 20).

I. Property Development

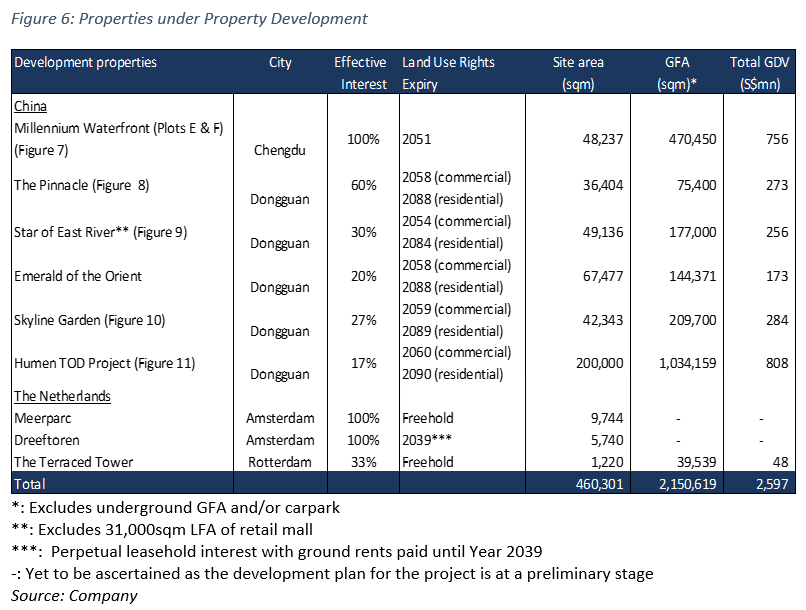

Presently, FSG is working on the Millennium Waterfront, Dongguan portfolio and The Terraced Tower in The Netherlands. Its Dongguan portfolio consists of Star of East River (SoER), Emerald of the Orient (EoO), The Pinnacle, Skyline Garden and the Humen Transit Oriented Development (TOD) Project.

Investment Merits

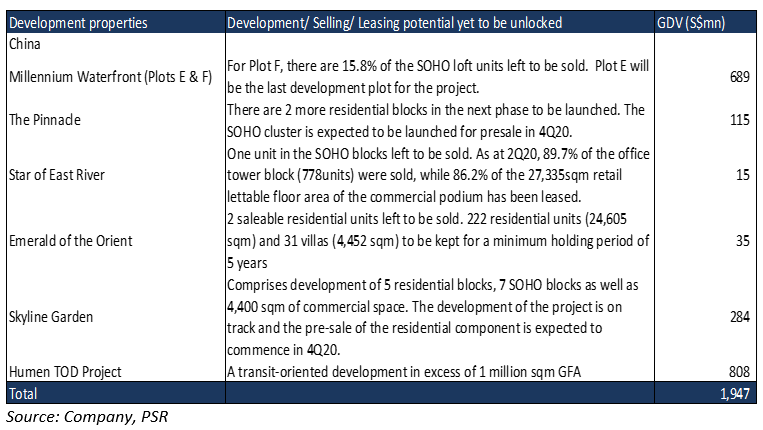

1. Unrecognised revenue from development properties amounts to S$586mn, or 1-2 years of sales. Revenue is only recognised upon handover for its Chinese properties and by percentage of completion for The Terraced Tower. As most of its projects are due for handover either in late 2020 or 2021, we expect the bulk of the revenue to be reflected this and next year.

2. GDV of S$1.95bn for unlocking, equivalent to 5-6 years of sales. The largest projects in its pipeline are Plot E Millennium Waterfront and its recently secured Humen TOD project.

3. Humen TOD to become one of FSG’s largest development projects to date (Figs. 11-12). FSG successfully won the bid for a mixed-use development on 29 June at RMB6.6bn (c.S$1.3bn) in a JV with China Poly Group and China State Railway Group. The land will be developed into a transit-oriented development with more than 1mn sqm in GFA, encompassing the different interchanges along Guangzhou, Hongkong, Shenzhen, Humen and Dongguan. FSG has a c.17% effective equity interest in the JV.

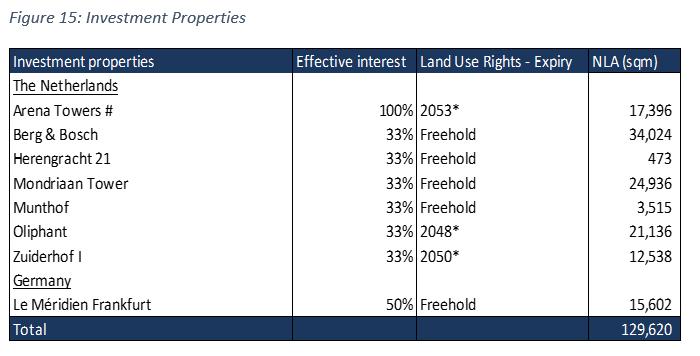

4. Unrelenting demand in Dongguan residential market. Dongguan, a city in China’s Greater Bay Area, is located between Shenzhen and Guangzhou. It is a manufacturing hub that is receiving an influx of talent, as more companies move to the city. As Shenzhen remains a highly-sought-after market due to its proximity to Hong Kong, Dongguan is benefitting from spillover demand for properties in the Greater Bay Area.

Buying sentiment in the Dongguan property market has exceeded FSG’s expectations after normal business activities resumed in late February. As of 30 June, almost all the SOHO units in its SoER project and saleable residential units in its EoO project had been sold. The Pinnacle project launched five residential blocks for sale in phases from April. These were also almost fully sold soon after their launches. Another residential block in The Pinnacle was launched for pre-sales on 14 July and has since sold more than 85%. The current resurgence of demand has triggered price-control measures from the Dongguan municipal, though the measures appear to have failed to slow down sales. The Group will pace the launch of its remaining two residential blocks in The Pinnacle and five residential blocks in its Skyline Garden project appropriately.

Key Risks

1. Rental abatements provided to retail tenants during Covid-19. Due to the impact of Covid-19, several retail tenants in the Star of East River retail mall requested for concessions to their rental obligations. The amount of rental abatements provided as of 1H20 was about three months of rent. We are expecting an additional waiver of three months to help the tenants tide over the crisis. Total amount of arrears is estimated to be S$2mn.

2. Reassessment of development pipeline to slow down growth plans. FSG obtained an irrevocable building permit to redevelop and increase the net lettable floor area of its Dreeftoren Amsterdam office property (acquired for €11.7mn) by 74% in 2019. In light of prevailing market conditions, it is re-assessing the feasibility of this new residential and office project. If it does not materialise and assuming a net yield of 3%, we are expecting S$0.98mn worth of delay in recurring profits.

II. Property Holding

FSG owns a portfolio of hotels and investment properties in Europe (FY19: 13.6% of total assets) and China (7.8%).

Investment Merits

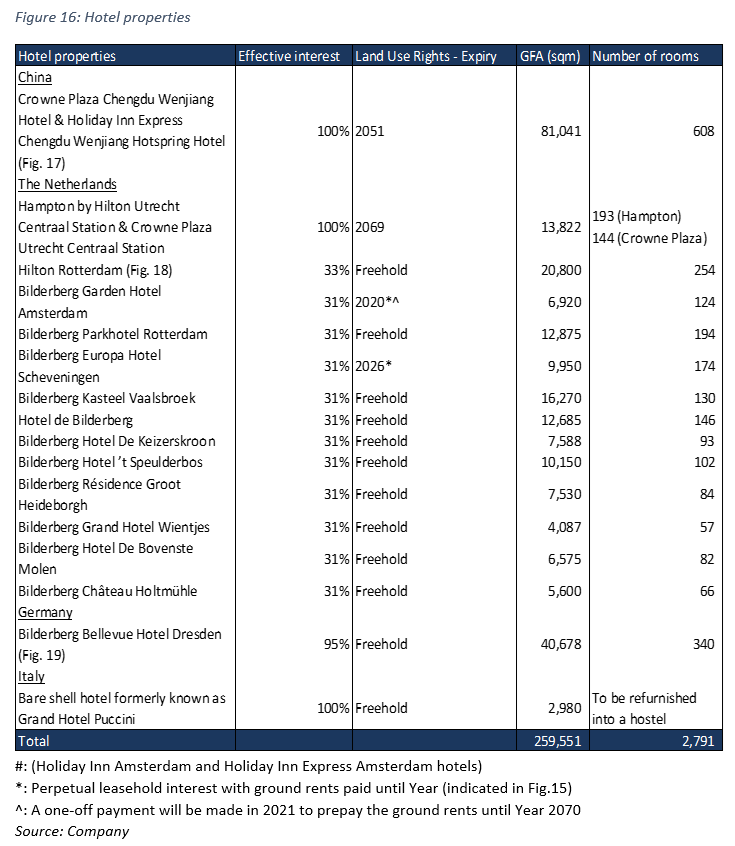

1. Arena Towers provide recurring income at yields of more than 6%. Arena Tower comprise two hotels in Amsterdam and their adjoining car parks that have been leased to external tenants. Each lease contains annual rents indexed to consumer prices and an initial non-cancellable period of 25 years. Despite Covid-19, tenant is still paying rent. In case of default, FSG holds three months of bankers’ guarantees. With regards to the other investment properties, most are paying rent except for a few small tenants.

2. Strong financial standing opens FSG to new opportunities. With cash of S$474.9mn and a low net debt-equity ratio of 0.16x, balance sheet remained robust as at end-1H20. Additionally, undrawn committed long-term debt facilities of S$520.1mn and potential equity infusions from the exercise of outstanding warrants of S$460mn should equip FSG financially to take advantage of acquisition opportunities.

Key Risks

1. Worst may not be over; stunted recovery is expected. FSG’s hotels are located in the parts of Europe where hotels saw a greater recovery in August (Netherlands portfolio ex-Amsterdam/ Rotterdam and Germany), boosted by demand for staycations. However, The Netherlands has seen a resurgence of Covid-19 cases lately, with new cases in September exceeding their peak in April. We are thus expecting a stunted recovery for its hotel portfolio till the end of 2020.

2. Rental arrears at Le Méridien Frankfurt. Le Méridien Frankfurt’s lessee, MHP, closed the hotel in March 2020 without the permission of the landlord and did not pay rent for April 2020. The Group has sought legal advice from its German lawyers on the non-payment of rents for May and June and half the rent for July. As at 21 July 2020, rental arrears amounted to €1.0mn, excluding VAT. The tenant re-opened the hotel on 15 May 2020. FSG holds a one-year banker’s guarantee for this lease. Results of the court hearing will be announced in 3Q20.

3. Reassessment of development pipeline to slow down growth plans. FSG is reconsidering its plan to convert its bare-shell hotel in Milan acquired for €10.7mn in January 2019 into a high-density youth hostel in light of current market conditions. If this development does not materialise and assuming a 5% net yield, we are expecting S$0.86mn worth of delay in recurring profits

III. Property Financing

According to the World Economic Forum, China has one of the largest shadow-banking industries, with about 40% of its outstanding loans tied up in shadow banking. Shadow banking is mainly driven by the need for funding by small and medium-sized private companies (SMEs). These companies are unable to obtain loans from banks, which often prefer to lend to state firms and the larger listed private companies. FSG operates its property-financing business primarily in China via entrusted loans, The Netherlands, Germany, and Australia. In China, FSG only lends in first-tier and second-tier cities where it has a presence in. (Refer to Appendix I – Entrusted Loans).

Investment Merits

1. High recurring income coupled with double-digit growth in loan book. Of all its business lines, property financing has the highest gross profit margin (Fig. 22). This is because funding for this business in China is derived from its Chinese operations, which allows the business to grow at minimal to no costs. The business gives FSG high recurring income underpinned by interest rates of low to mid-teens p.a. Its China loan book grew at a CAGR of 19% from 2015 to 2019, largely attributable to high demand for credit among the SMEs. We are estimating loan book growth of around 8% for FY20e and FY21e. Average tenure for its China loan book is 3 years.

As of 1H20, two defaulted loans had been fully repaid. The YoY increase in revenue in 1H20 (Fig. 21) was mainly due to one-off loan restructuring income of S$15.5mn and establishment fees from its new development venture in Australia.

2. Zero bad-debt losses in eight years of operations; conservative LTV range of 40-60%. FSG started its property-financing business in 2012. To date, it has not incurred any bad-debt losses. Although there were two cases of default in 2015 and 2016, FSG has managed to recover both its principal and interest. A 30.4% annual return was registered for one of these defaulted loans. Average loan to value (LTV) ratio for its portfolio ranges from low 40% to 60%.

3. Maiden venture in Australia to redevelop City Tattersalls Club. FSG holds an equity stake of 39.9% in ICD SB Pitt Street Trust, which is renovating Sydney’s City Tattersalls Club’s premises and developing the airspace above into a hotel and residential apartments. Apart from development fees payable to the trust, FSG will also charge a single-digit interest rate p.a. on a A$370mn (S$368mn) construction loan financing facility to fund the project. The project has received approval for its Stage 1 concept development and construction is expected to start in 2022.

Key Risks

1. Subject to interest-rate cuts for penalty interest. China’s Supreme Court announced a plan in July to cut interest rates that shadow banks can charge for default penalties. The default penalty rate is now limited to 4x the Loan Prime Rate (4.35%) + a court-judged default rate (6%). This means FSG’s return on default loans is now capped at 23.4%, versus no limits previously. The Group had ever recovered defaulted loans at 30.4% p.a. penalty rates in the past.

2. Short-term deferral for interest payments provided for 40% of its China loan book. Amid Covid-19, FSG has given consent to two borrowers of a RMB580mn loan and RMB330mn loan respectively for the short-term deferral of their interest payments.

- The RMB580mn loan is secured on a Guangzhou city hotel with a 44% LTV. The borrower could defer 50% of its monthly interest payments for a few months from 2Q2020, on condition that it contributes additional equity to a bank account jointly controlled by the borrower and FSG.

- The RMB330m loan is secured on a residential villa (RMB50m @ 46% LTV) and a 5-floor retail mall (RMB280m @ 55% LTV) in Shanghai. The related borrower group has been given consent to defer interest payments for one month.

Others

East Sun and Wanli portfolios. Through a 90% stake in Dongguan East Sun Limited, which has a 49% stake in Dongguan Wan Li Group Limited (Wanli), FSG owns a portfolio of commercial and industrial properties in Dongguan. The East Sun and Wanli portfolios are tenanted with positive running yields.

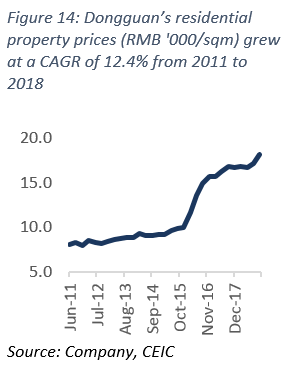

Update on sale of certain parts of Chengdu Cityspring. In February 2020, the buyer of certain parts of FSG’s Chengdu Cityspring project wrote to the Group to terminate their sale and purchase agreement. In June 2020, the buyer entered into a supplemental agreement with the Group to obtain a discount of RMB3.5m on the purchase consideration for 292 car-park spaces and to acquire another 268 car-park spaces. The total purchase consideration was increased by RMB5.9m to RMB470.9m. The buyer has also withdrawn its termination letter. To date, 89% of the total purchase consideration has been collected, or RMB421.3mn. The outstanding RMB49.6mn will be repaid via monthly instalments of at least RMB10mn.

Disposal of Villa Nuova Office, Zeist, The Netherlands. FSMC completed the sale of Villa Nuova, a 1,428 sqm office property in Zeist, The Netherlands, on 31 Jan 2020. The property was 100% leased with lease expiry on 1 Jun 2022. The sale was completed before the Covid-19 pandemic hit The Netherlands, at a premium of about 8% over its allocated cost. FSMC had enjoyed an annual net rental yield of more than 10% since its purchase in November 2015.

Market Outlook

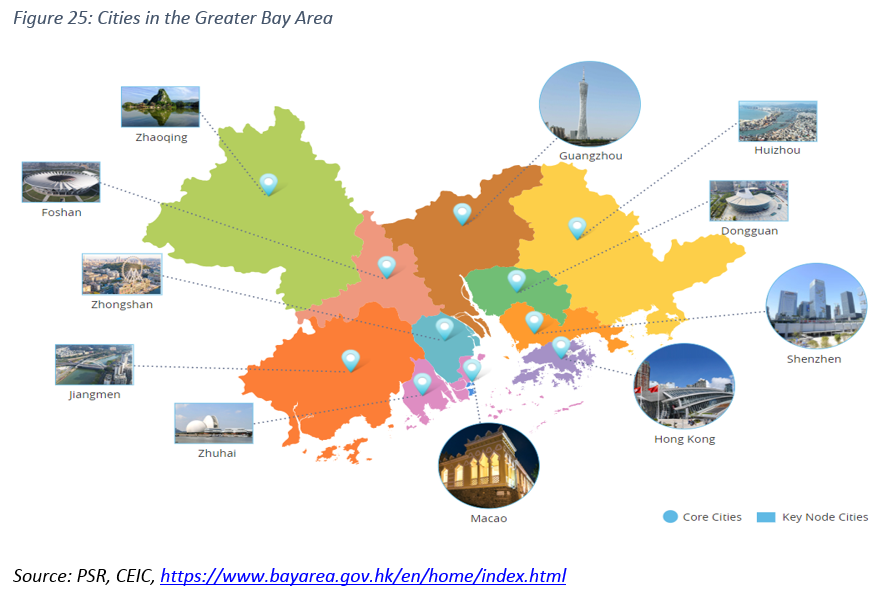

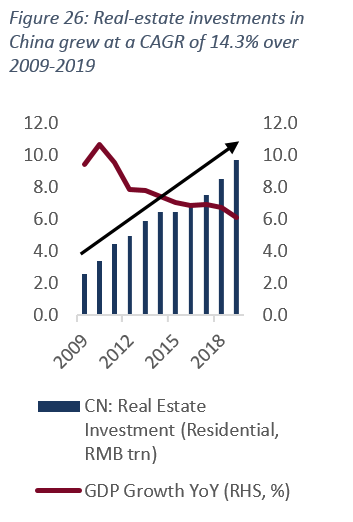

Property development in China. Hong Kong and mainland China are closely connected. With well-developed cross-boundary transportation networks and cross-boundary facilities, cross-boundary passenger traffic has been on the rise in recent years. In 2018, over 235mn passenger trips were made across the border via land crossings, bringing the daily average to over 640,000 passenger trips.

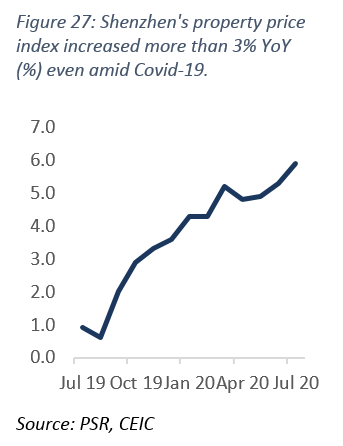

Initiated in July 2017, the Greater Bay Area (Fig. 25) covers the four core cities of Hong Kong, Macao, Guangzhou and Shenzhen as engines for regional development, while supporting Zhuhai, Foshan, Huizhou, Dongguan, Zhongshan, Jiangmen and Zhaoqing to become key node cities with distinct characteristics. The ultimate aim is to raise the development quality of this cluster of cities. The Dongguan property market is expected to continue to benefit from the development of the Greater Bay Area. Additionally, Shenzhen’s continuing dominance as a tech hub could drive demand from mainland and Hong Kong tenants. In March 2020, 288 apartments in a new Shenzhen property development were sold out online in less than eight minutes. Dongguan’s proximity to Shenzhen is expected to position FSG well for capturing spillover demand for residential properties.

Property financing in China. After 2.5 years of regulatory clampdown, shadow banking has returned as China pledges faster credit growth to rescue its coronavirus-hit economy. According to Moody’s, shadow-banking assets in the world’s second-largest economy grew RMB100bn (US$14bn) to RMB59.1trn (US$8.4trn) in the first quarter of 2020, compared with a RMB1.2trn decline to RMB60.2trn during the same period in 2019. A survey in February 2020 of 2,069 small businesses by Zhenghe Island Research Institute found that more than a fifth of the respondents took private loans after Covid-19 broke out. The borrowing binge came with high interest rates. Private lenders in four provinces said they charged annual interest of 18-40%, compared with the benchmark one-year bank lending rate of 3.85%, to offset credit risks among subprime borrowers.

China’s Supreme Court announced a plan in July 2020 to cut the penalty interest rate that shadow banks can charge. The figure could fall as low as 15% a year from 24%, affecting nearly RMB7trn (US$1trn) of outstanding loans. As a result, multiple shadow-banking lenders may stop servicing medium to high-risk borrowers. FSG is selective about the loans it makes, with several criteria to be met by its borrowers (Appendix I – Entrusted Loans). It is also not in the ‘high risk’ business, as evident from the interest rates it charges on its loans relative to the other lenders. Given current economic conditions, it has received overwhelming requests for loans. However, FSG intends to remain discerning and selective.

Property holding in The Netherlands. Amsterdam remains the most attractive city for hotel investments in 2020 for the fourth year in a row due to its positive demand fundamentals and yield profile. Overall arrivals at Amsterdam grew at a CAGR of almost 7% annually over the past 10 years with continuous national y-o-y arrival growth since 2008. In 2019, international inbound tourists (19.5mn) largely comprised EU residents (79%), according to NBTC Holland Marketing. Residents from the US and Asia constituted 11% and 7% respectively. This highlights that inbound tourism is highly reliant on EU travellers.

Member states of the EU were provided with guidelines and recommendations to lift travel restrictions gradually on 13 May. In July, ticket numbers for cross-border air travel within Europe stood at 28% of 2019 levels, as Europeans began to travel again after months of lockdown, according to the travel analysis group, ForwardKeys. However, in recent months, countries across Europe are seeing a resurgence of Covid-19 cases, after successfully slowing down outbreaks earlier. France, Poland, The Netherlands and Spain could be dealing with a much-feared second wave.

The Dutch government has announced specific measures to control the spread of coronavirus. The measures apply to the six safety regions that are currently seeing the sharpest spikes in coronavirus infections. These are Amsterdam-Amstelland, Rotterdam-Rijnmond, Haaglanden, Utrecht, Kennemerland and Hollands Midden. Restrictions include a ban on gatherings of more than 50 people and closing of catering establishments by midnight. The six regions are also adopting specific local measures. We are expecting these restrictions to undo the August recovery for FSG’s hotels in July and August and for hotel occupancy to fall back to YTD levels till the end of the year, before a potential recovery in 2021 should the situation improve.

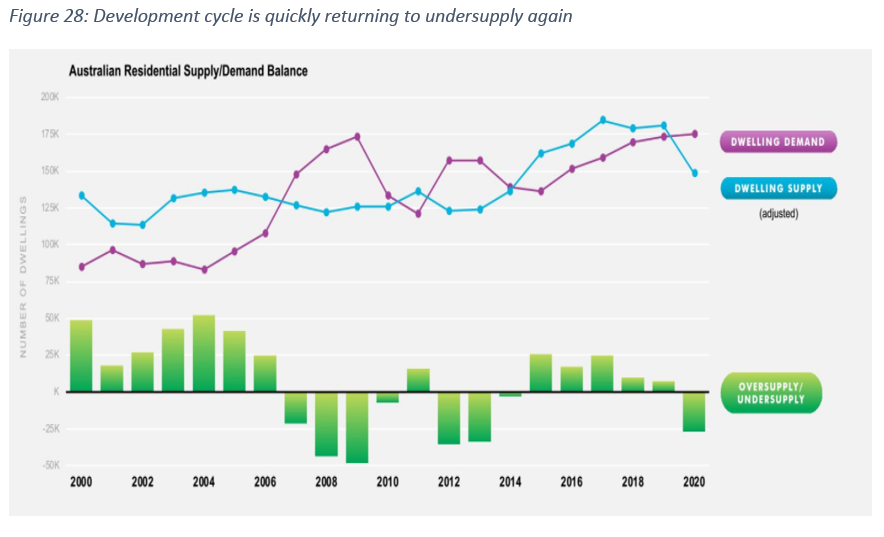

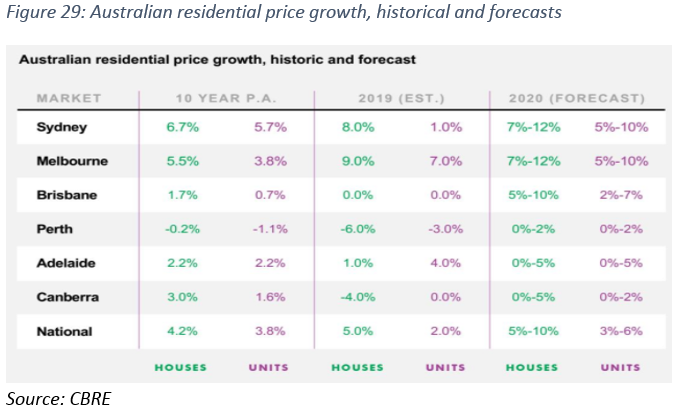

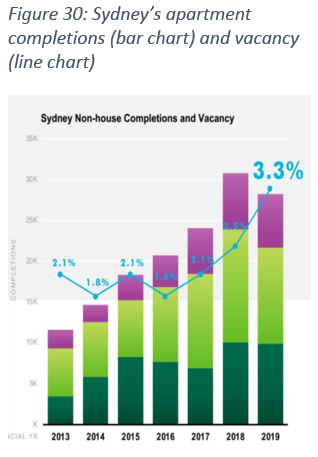

Property Development in Australia. According to CBRE, residential prices in Sydney grew 8% in 2019, though vacancies climbed higher to 3.3% (2018: 2.5%), amid lower apartment completions. We are expecting residential price growth to moderate in 2020 due to existing inventories before the decline in new supply comes through in 2020 and 2021.

For hotels, softer trading conditions in 2020 will be driven by a combination of supply additions and subdued demand growth. New CBD retail luxury brands are expected to attract international visitors after the relaxation of travel restrictions (Fig. 31).

Property financing in Australia. Non-bank lending in the Australian property market is forecast to expand further in 2020, driven by increased interest from both developers and investors. The Australian non-bank loan market has been an essential source of funding for Australian property developers and investors for decades. Domestic banks currently hold around 70% of the corporate lending market, according to Metrics.

Due to the large balance-sheet capacity and capital required to operate in the market, barriers to entry are high. In recent times, banks have come under regulatory pressure to reign in their loan portfolios to meet stricter capital requirements. This has opened up opportunities for non-bank lenders to claim a greater share of the >US$900bn market. For this reason, we expect non-bank lenders to register modest growth in the coming year.

Valuation

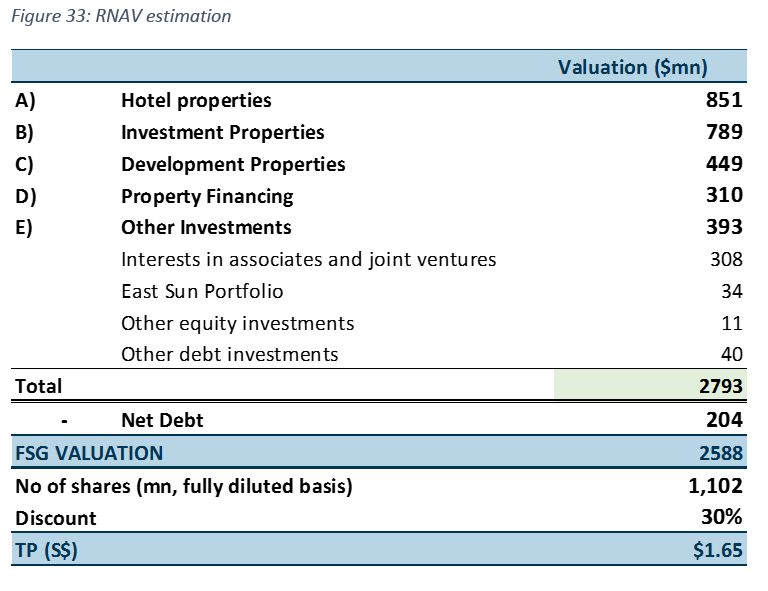

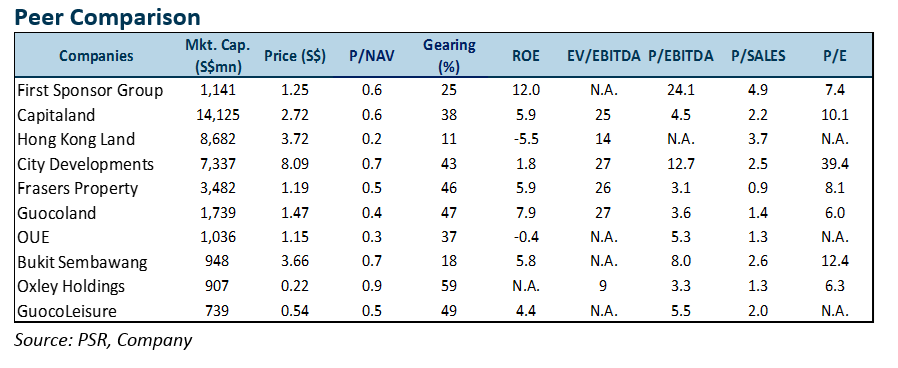

We initiate coverage of FSG with a BUY rating and RNAV-derived target price of S$1.65. Our target price implies a total potential return of 33.6% and dividend yield of 1.75%. It is based on a 30% discount to FSG’s fully-diluted RNAVPS (@1,102mn shares after adding outstanding warrants). Based on its current number of shares (912mn), we derive a target price of S$1.99. FSG trades at 0.6x FY20e P/B versus its historical 5-year average of 0.7x.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

- recipients of the analyses or reports are to contact Phillip Securities Research (and not the relevant foreign research house) in Singapore at 250 North Bridge Road, #06-00 Raffles City Tower, Singapore 179101, telephone number +65 6533 6001, in respect of any matters arising from, or in connection with, the analyses or reports; and

- to the extent that the analyses or reports are delivered to and intended to be received by any person in Singapore who is not an accredited investor, expert investor or institutional investor, Phillip Securities Research accepts legal responsibility for the contents of the analyses or reports.

Frencken Group Ltd - Consolidation before 2H26e recovery

Frencken Group Ltd - Consolidation before 2H26e recovery SIA - Weighed down by associates

SIA - Weighed down by associates