Keppel DC REIT - Resilient demand amid tight supply

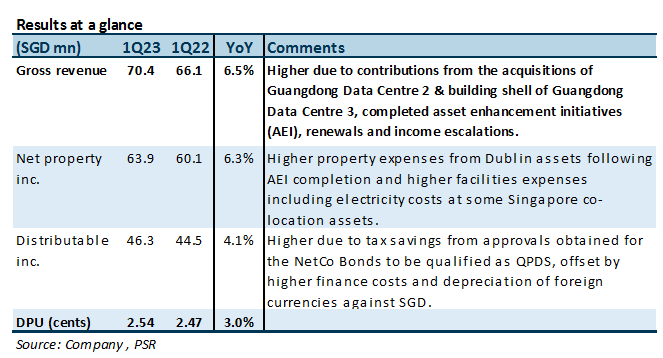

21 Apr 2023- 1Q23 DPU rose 3% YoY to 2.541 Singapore cents, due to the acquisitions of Guangdong Data Centre 2 and 3; completed asset enhancement initiatives (AEI); renewals and income escalations; and tax savings from the approval of the NetCo Bonds being qualified as Qualifying Project Debt Securities (QPDS).

- These were partially offset by lower contributions from some of its Singapore co-location assets arising from higher facilities expenses including electricity costs, higher finance costs and the depreciation of EUR, AUD and GBP against SGD.

- Downgrade from BUY to ACCUMULATE. Target price lowered from S$2.58 to S$2.26 on higher interest expense and cost of equity. Catalysts include more accretive acquisitions and lower-than-expected interest costs. The current share price implies FY23e/24e DPU yields of 4.7%/4.9%.

The Positives

+ Portfolio occupancy remained stable at 98.5% QoQ, with a portfolio WALE of 8.2 years. 14.3% of leases by rental income will expire in 2023. In our view, the likelihood of lease renewal is high due to the high costs of tenant re-location and 54% of its assets are located in Singapore.

+ Prudent capital management, with 73% of debt on fixed rate. Average cost of debt increased from 2.7% in 4Q22 to 2.8% in 1Q23. A 100bps increase in interest rates would lower DPU by c.2.2%. Gearing also edged up from 36.4% at end 2022 to 36.8%. KDCREIT has no refinancing obligations in 2023 after refinancing all loans expiring in 2023 (4.9% of total) in early April at 3-month EURIBOR plus an agreed spread. Foreign sourced income is also substantially hedged till the end of 2023, and partially thereafter until the middle of 2024. EU accounts for c.24% of income.

Outlook

Keppel DC REIT is on the lookout for acquisitions, including off-market transactions. Japan is a potential target market, where acquisition cap rates are around 5% and interest rates remain low. The sponsor also has >S$2bn worth of data centre assets under development and management that KDCREIT could potentially acquire.

There is a final payment of c.S$142mn upon the completion of Guangdong Data Centre 3, expected to take place in 3Q23. Our forecasts assume this would be funded via a cash call.

Downgrade from BUY to ACCUMULATE with a lower DDM TP of S$2.26 (prev. S$2.58)

KDCREIT’s NPI yield of 7.2% and long WALE of 8.2 years is still superior to other asset classes. Its largest tenants are some of the biggest internet enterprises in the world, with its largest contributing 35.5% of rental income. Catalysts include more accretive acquisitions and lower-than-expected interest costs. The current share price implies FY23e/24e DPU yields of 4.7%/4.9%.

About the author

Darren Chan

Research Analyst

PSR

Darren has over three years of experience on the buy-side as a fund manager. During his time as fund manager, he has managed multiple funds and mandates including dividend income, growth, customised, Singapore focused and regionally focused funds. He graduated from the University of London with a First-Class Honours degree in Banking and Finance.

About the author

Darren Chan

Research Analyst

PSR

Darren has over three years of experience on the buy-side as a fund manager. During his time as fund manager, he has managed multiple funds and mandates including dividend income, growth, customised, Singapore focused and regionally focused funds. He graduated from the University of London with a First-Class Honours degree in Banking and Finance.

Trade of the Day - Aztech Global Ltd (SGX: 8AZ)

Trade of the Day - Aztech Global Ltd (SGX: 8AZ) Trade of the Day - Singapore Exchange Ltd (SGX: S68)

Trade of the Day - Singapore Exchange Ltd (SGX: S68)