United Overseas Bank Limited - Continued NII growth boosts earnings

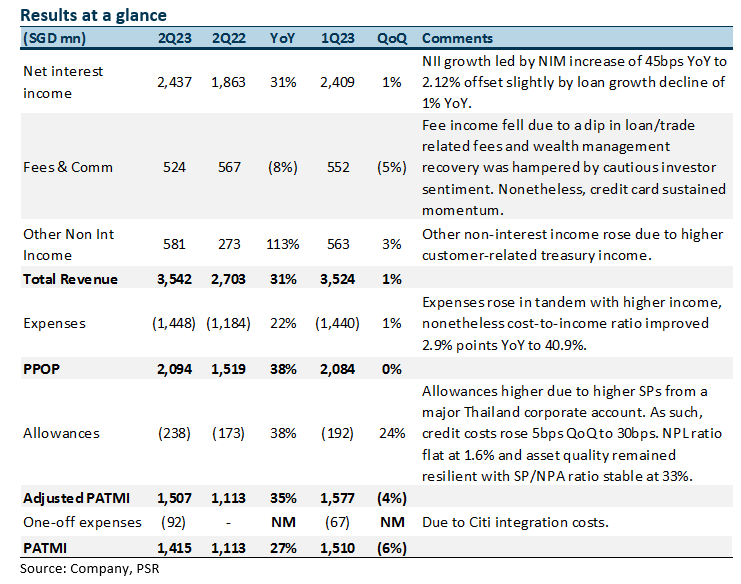

31 Jul 2023- 2Q23 adjusted earnings of S$1,507mn were slightly above our estimates due to higher other non-interest income and higher NII offset by lower-than-expected fee income growth and higher allowances. 1H23 adjusted PATMI was 54% of our FY23e forecast. 2Q23 DPS was up 42% YoY to 85 cents.

- Positives include NII growth of 31% YoY and other non-interest income surging by 113% YoY, while negatives include fee income decline of 8% YoY and allowances increasing 38% YoY. Management has maintained its loan growth guidance of low to mid-single digit and credit costs at around 25bps, while lowering its guidance of NIMs to 2.10-2.15% (prev. 2.10-2.20%) and fee income growth from double digit to high single-digit growth for FY23e.

- Maintain BUY with a higher target price of S$35.90, from S$35.70. We raise FY23e earnings by 4% as we raise other non-interest income estimates but lower NII, fee income and increase provisions estimates for FY23e. We assume 1.48x FY23e P/BV and ROE estimate of 12.9% in our GGM valuation.

The Positives

+ NII surges on the back of strong NIM expansion. NII grew 31% YoY, despite a decline in loans growth of 1% YoY, while NIM surged 45bps YoY to 2.12% but declined 2bps QoQ due to excess liquidity deployed to high quality assets. Loan growth decline was due to weakness in Singapore and North Asia offset by growth in the rest of ASEAN. UOB has maintained its loan growth guidance for FY23e at low to mid-single digit.

+ Other non-interest income surged in 2Q23. Other NII increased 113% YoY largely due to higher customer-related treasury income and strong performance from trading and liquidity management activities this quarter. Management also noted record high customer-related treasury income from increased hedging demands and good performance from trading and liquidity management activities.

+ New NPAs fall 45% YoY. New NPA formation fell by 45% YoY to S$364mn as asset quality stabilised during the quarter. The NPL ratio remained stable YoY and improved 10bps QoQ to 1.6%. Asset quality remained resilient with SP/NPA increasing slightly to 33%. 2Q23 NPA coverage is at 99% and unsecured NPA coverage at 209%.

The Negatives

– Fee income fell YoY and QoQ. Fees fell 8% YoY largely due to lower loan-related fees and wealth management fees as investor sentiments remained subdued, offset by a continued increase in credit card fees. On a QoQ basis, fee income fell 5% from lower wealth fees as investor sentiments remained muted offset by sustained momentum in credit card fees.

– Credit costs increase due to higher SPs and GPs. Total allowances rose by 38% YoY to S$238mn mainly due to specific allowance increasing by 22% YoY to S$202mn largely due to a major Thailand corporate account and general allowance of S$36mn (2Q22: S$7mn). This resulted in credit costs increasing by 8bps YoY to 30bps. Nonetheless, total general allowance for loans, including RLARs, was prudently maintained at 1.0% of performing loans. UOB has increased its guidance for credit cost from 20-25 bps to around 25bps for FY23e. Management said that the major Thailand corporate account is in the manufacturing sector and was hit by fraud, for which they had to fully provide for, nonetheless they do not see any systemic risk from this account.

– Expenses up 22% YoY. Excluding one-offs, expenses rose 22% YoY to S$1,448mn. The increase was due to continued focus on investments to enhance capabilities to drive strategic initiatives. Nonetheless, the cost-to-income ratio (CIR) improved 2.9% points YoY to 40.9% on the back of strong income growth. UOB has maintained its guidance for a CIR of 43-44% for FY23e, and to trend below 42% by FY24e.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

Far East Hospitality Trust - Higher RevPAR by ramping up occupancy

Far East Hospitality Trust - Higher RevPAR by ramping up occupancy Trade of the Day - Aztech Global Ltd (SGX: 8AZ)

Trade of the Day - Aztech Global Ltd (SGX: 8AZ)