Salesforce Inc - Focused on improving earnings

4 Dec 2023- 9M24 revenue was within expectations but earnings were ahead. 9M24 revenue/PATMI were 74%/78% of our FY24e forecasts. 3Q24 PATMI spiked 483% YoY to US$1.2bn driven by higher operating leverage.

- For 4Q24e, Salesforce expects total revenue to grow 10% YoY to US$9.2bn driven by resilient demand for its Sales Cloud, Service Cloud, and MuleSoft offerings. GAAP EPS to be about US$1.27 vs -US$0.10 in 4Q23 led by cost-containment efforts.

- We maintain ACCUMULATE with a raised DCF target price of US$270.00 (prev. US$242.00), with a WACC of 7% and terminal growth of 4%. Our FY24e/FY25e revenue estimates remain unchanged; while we have increased PATMI estimates by 14%/13% to account for lower expenses. We believe Salesforce is well-positioned to benefit from cloud-based digital transformation trends as companies look to form a more holistic view of their customer data to provide better customer experiences.

The Positives

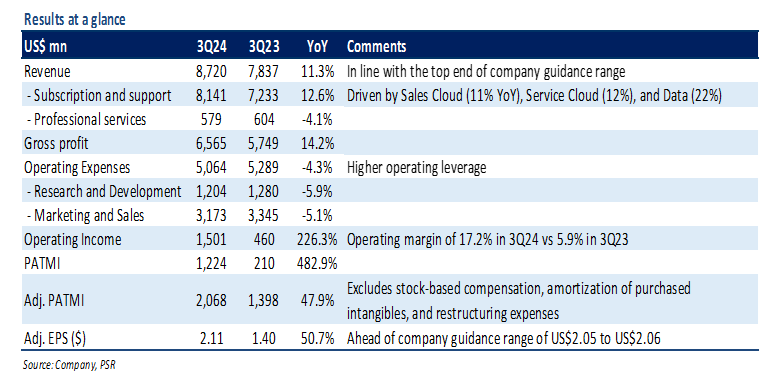

+ Strong demand across all products. 3Q24 total revenue grew 11% YoY to US$8.7bn, in line with the top end of company guidance, driven by higher subscription and support revenues. Salesforce witnessed resilient demand from large enterprises for its core products with Sales Cloud and Service Cloud revenues growing 11% YoY and 12% YoY to US$1.9bn and US$2.1bn, respectively. Within Data Cloud segment, revenues for integration software MuleSoft grew 26% YoY, while revenues for data visualization tool Tableau grew 16% YoY.

+ cRPO growth continued to accelerate. Salesforce’s current remaining performance obligations (cRPO), a measure of contracted sales to be recognised in the next 12 months, jumped 14% YoY to US$23.9bn. The cRPO growth came above the 11% company guidance and was driven by strong early renewals and large customer wins. Management highlighted that the number of deals over US$1mn grew by 80% YoY. We expect large deals and multi-cloud adoption momentum to support near-term growth as it will lead to higher subscription sales.

+ Margins rise on cost discipline. In 3Q24, Salesforce’s operating expenses fell by 4% YoY to US$5.1bn resulting in an operating margin of 17.2% (vs. 5.9% in 3Q23). The improvement was mainly driven by a leaner cost structure after significant cost-cutting measures over the last 12 months, including job cuts and lower sales-related costs. Headcount was down -11% YoY.

The Negative

– NIL

May 21st - Things to Know Before the Opening Bell

May 21st - Things to Know Before the Opening Bell Trade of the Day - Coinbase Global, Inc. (NASDAQ: COIN)

Trade of the Day - Coinbase Global, Inc. (NASDAQ: COIN) Sea Ltd. - Growth Supported by Spending

Sea Ltd. - Growth Supported by Spending Singapore REITs Monthly: April24 - Pricing in higher-for-longer interest rates

Singapore REITs Monthly: April24 - Pricing in higher-for-longer interest rates