CapitaLand Integrated Commercial Trust - Portfolio reconstitution amidst recovery

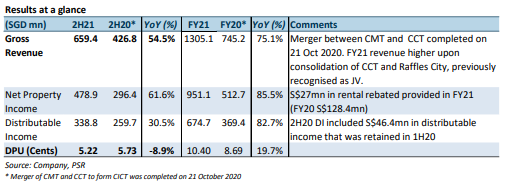

4 Feb 2022- FY21 DPU of 10.40 Scts (+19.7% YoY) was in line, forming 102% of our forecast.

- Operating metrics continue to improve; tenants’ sales lifted by broader recovery amongst trade sectors while negative retail reversions continue to narrow.

- Portfolio occupancy declined by 2.5ppts YoY due to timing of lease expiries at Capital Tower and Six Battery Road and trading impacted Clarke Quay.

- Maintain ACCUMULATE, DDM-based (COE 6.41%) TP lowered from S$2.54 to S$2.39. FY22e-26e DPU lowered by 5.2-6.7% to factor in higher utility and energy costs as well as the rising cost of borrowing. Our DDM-based TP dips from S$2.54 to S$2.39 on lower DPU estimates and higher cost of equity of 6.41% assumption (previous 6.27%). Catalysts for CICT include asset enhancement initiatives and acquisition.

The Positives

+ Recovery in tenant sales and narrowing negative reversions support improving tenant sentiment. Full-year retail reversions narrowed to -7.3% (1H21: -9.1%). Suburban and downtown reversions were -2.4% and -13.8% respectively. Tenant retention remains stable at 82% (FY20 84.5%). Broader recovery amongst trade categories was observed from the 12.2% YoY growth in total tenants’ sales, with nine out of 15 trade categories showing YoY growth. However, FY21 tenant sales psf was still below pre-pandemic levels, at 87.8% of FY19’s monthly average. Rental support has also eased – FY21 rental waivers came in at S$27mn, slightly more than half a month of rent, compared to the S$128.4mn in rebates disbursed in FY20.

+ Valuation uplift of 3.5% or S$752.8mn YoY. Retail assets saw a modest 3% valuation uplift on the back of recovering performance while cap rates remain unchanged. Office and integrated development assets accounted for 45% and 52% of the revaluation gains, owing to cap rate compressions for office assets and CapitaSpring achieving TOP in Nov 21. Clarke Quay and Raffles City took a S$52mn and S$107mn write-down due to CAPEX provisions for upcoming AEI works. Valuation for Gallileo fell by 13.2% of S$76mn as valuers factored in the exercise of lease break option by Commerzbank, which will bring forward the lease expiring from 2029 to 2024.

+ Portfolio reconstitution and entry into new market. CICT divested its 50% stake in OGS for S$640.7mn at an exit yield of 3.17%, 9.1% above valuation price on 30 Sep 21. It also entered a new market, Australia, making a A$1.1bn investment in two Grade A office buildings and 50% interest in integrated development, 101-103 Miller Street and Greenwood Plaza. These three Australian acquisitions carry an average NPI yield of 5.1% and a pro-forma DPU accretion of 2.8%. Post-acquisition, Australia represents c.5% of AUM. Capital recycling continued into FY22 – CICT announced the sale of JCube for S$340.0m at NPI yield of c.4%, 21.9% above FY21 valuation, realising net gains of S$56.7mn.

Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU Apr 25th - Things to Know Before the Opening Bell

Apr 25th - Things to Know Before the Opening Bell JPMorgan Chase & Co - NII continues to rise, guidance maintained

JPMorgan Chase & Co - NII continues to rise, guidance maintained