Frasers Cpt Tr - Stock Analyst Research

| Target Price* | 238.00 |

| Recommendation | ACCUMULATE› ACCUMULATE |

| Market Cap* | - |

| Publication Date | 26 Apr 2024 |

*At the time of publication

Frasers Centrepoint Trust - Robust operating performance in 1H24

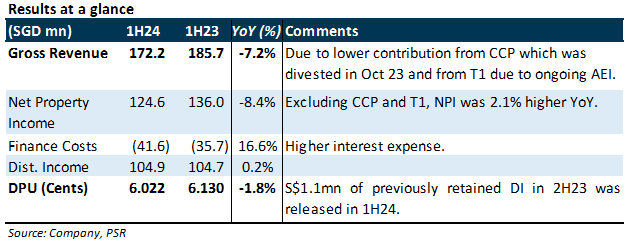

- 1H24 DPU of 6.022 Scts was 1.8% lower YoY, in line with our expectations. Gross revenue/NPI fell 7.2%/8.4% YoY due to the divestment of Changi City Point (CCP) in Oct 23, and ongoing AEI work at Tampines 1 (T1). Excluding these factors, gross revenue/NPI would have risen 2.9%/2.1% YoY.

- 1H24 retail portfolio occupancy was high at 99.9%, with portfolio rental reversions at +7.5%. 2Q24 shopper traffic and tenants’ sales were up 8.1% and 4.3%, respectively. This was an improvement from 1Q24 shopper traffic growth of 3.1% and tenants’ sales decline of 0.7% YoY.

- Maintain ACCUMULATE, with an unchanged DDM TP of S$2.38. We expect 7% positive rental reversion for FY24e, supported by the low occupancy cost of 15.5%. Share price catalysts include more accretive acquisitions and lower-than-expected interest costs. The share trades at an FY24e DPU yield of 5.6%. There is no change in our estimates.

The Positives

+ 2Q24 retail portfolio occupancy remained almost full at 99.9% (unchanged QoQ). Occupancy was at least 99% across all the malls. 1H24 rental reversion of +7.5% exceeded our expectations, and it was above 1H23 rental reversion of +4.3%. We expect this healthy positive rental reversion trend to continue for the remaining 14% of leases (by GRI) that expire in FY24.

+ Improvements in tenants’ sales and shopper traffic. 2Q24 tenants’ sales and shopper traffic were 4.3% and 8.1% higher YoY, respectively. Portfolio shopper traffic is now only 2% below pre-COVID levels, while tenant sales are c.20% higher than pre-COVID levels. We expect tenants’ sales to remain robust, supported by the various government handouts to Singapore residents in 2024.

+ All-in cost of debt improved 10bps QoQ to 4.2%, as FCT used the proceeds from the divestments of Changi City Point and interest in Hektar REIT to pay off some of the higher-cost debt. Aggregate leverage rose 1.3%pts QoQ to 38.5% as loans were drawn down to finance the increased stake in NEX and the Tampines 1 AEI. 68.5% of debt is hedged to a fixed rate. FCT has no debt expiring in FY24, and its ICR is 3.26 times. FY24e all-in cost of debt is expected to be low 4%.

The Negative

– nil

About the author

Darren Chan

Research Analyst

PSR

Darren has over three years of experience on the buy-side as a fund manager. During his time as fund manager, he has managed multiple funds and mandates including dividend income, growth, customised, Singapore focused and regionally focused funds. He graduated from the University of London with a First-Class Honours degree in Banking and Finance.

About the author

Darren Chan

Research Analyst

PSR

Darren has over three years of experience on the buy-side as a fund manager. During his time as fund manager, he has managed multiple funds and mandates including dividend income, growth, customised, Singapore focused and regionally focused funds. He graduated from the University of London with a First-Class Honours degree in Banking and Finance.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU Apr 25th - Things to Know Before the Opening Bell

Apr 25th - Things to Know Before the Opening Bell