propnex - Stock Analyst Research

| Target Price* | 1.160 |

| Recommendation | ACCUMULATE› ACCUMULATE |

| Market Cap* | - |

| Publication Date | 14 Aug 2023 |

*At the time of publication

PropNex Ltd - Expecting a stronger 2H23

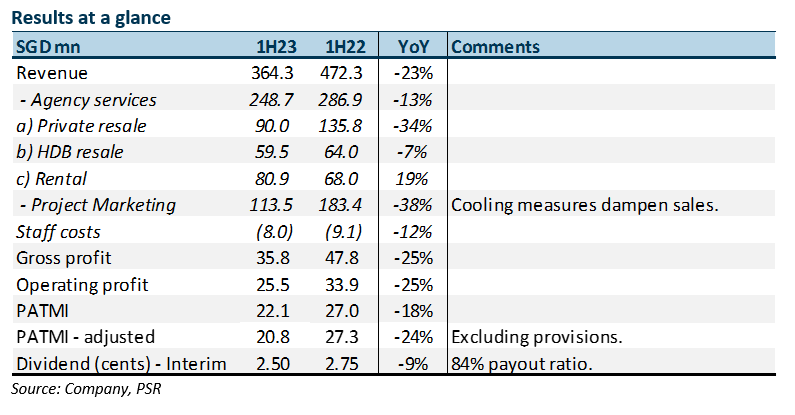

- 1H23 results were below expectations. Revenue and PATMI were 33%/30% of our FY23e forecast. Adjusted PATMI declined 24% YoY to S$20.8mn. Cooling measures and a dearth of new launches pushed revenue lower.

- We expect the pick-up in new launches and market share to drive a stronger performance in 2H23. We expect 8,100 units to be launched in 2H23 compared with 1H23’s 3,400. Market share from the recent launches has been around 43%.

- We lower our FY23e earnings by 9% to S$62.1mn and reduce the DCF target price to S$1.16 (prev. S$1.20). Our recommendation is downgraded from BUY to ACCUMULATE. The dividend yield is attractive at 6.3%, well supported by FCF and S$140mn net cash on balance sheet. We expected a rebound in 2H23 as it will benefit from larger number of new launches and market share gains. Meanwhile, private resale support will come from its large price discounts compared to new launches and surge in completions. HDB resale will be resilient from attractive grants and more units reaching their minimum occupancy period.

The Positive

+ Returning the surge in cash-flow. The highly cash generative model was evident despite the weakness in earnings. FCF generated in 1H23 improved to S$30.0mn (1H22: S$23mn). Capital expenditure remained minimal at S$0.5mn. The net cash was generally stable at S$139.6mn (1H22: S$133.9mn). PropNex announced an interim dividend of 2.5 cents by raising the payout ratio from 75% to 84%. Our forecast dividends of 6.5 cents or S$48mn is well sustained by FCF and strong net cash balance sheet.

The Negative

– Weakness in revenue. Revenue contraction has been larger than expected. Weakness was especially in private new launches and resale. Lack of new launches over the six months 4Q22 till 1Q23 and softness in sentiment post cooling measures drove volumes down.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU Apr 25th - Things to Know Before the Opening Bell

Apr 25th - Things to Know Before the Opening Bell JPMorgan Chase & Co - NII continues to rise, guidance maintained

JPMorgan Chase & Co - NII continues to rise, guidance maintained