Singapore Telecommunications Ltd - Currency headwinds everywhere

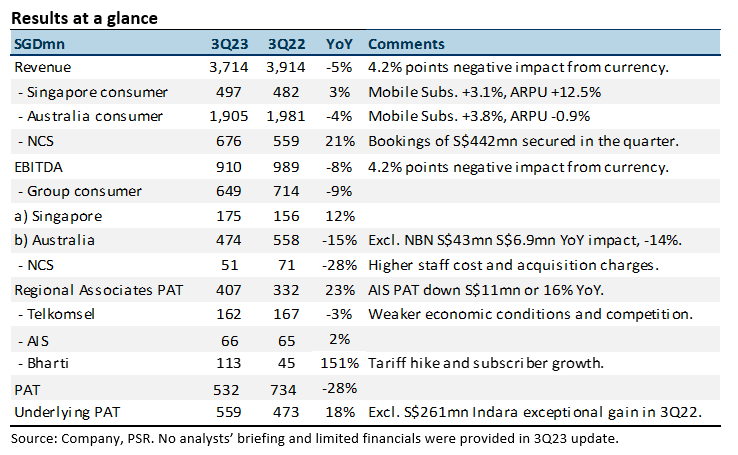

20 Feb 2023- 9M23 revenue met expectations at 73% of our FY23e estimates. EBITDA was below at 67%. There was an 8% point drag from the weaker Australian dollar. Underlying PAT rose 18% YoY to S$532mn, supported by a 23% rise in associate profit to S$407mn.

- Bharti net profit spiked 151% YoY to S$113mn, despite a 7% decline in the Indian Rupee. Optus operating metrics were stable post the cyber-attack in September.

- We lower our FY23e revenue/EBITDA by 5% and 7% respectively as we lower our Australian dollar assumptions by 10%. Our target price declined from S$3.05 to S$2.84 and we maintain our ACCUMULATE recommendation. Earnings growth continues to build up in India and Singapore. Weaker segments are sluggish earnings in Optus and NCS.

The Positive

+ Bharti is still the star performer. 3Q23 PAT for Bharti jumped 151% YoY to S$113mn despite the 7% currency headwind. Earnings growth was supported by mobile ARPU in India rising 18% YoY to Rs193 (S$3.10) and 4G subscriber growth of 11% to 216.7mn subscribers.

The Negative

– Optus sluggish profits. Mobile subscribers were flat QoQ at 10.3mn despite some initial churn post the cyber attack. Nevertheless, EBITDA contracted 14% YoY to S$474mn from increased staff and investments in new businesses.

Outlook

The two growth drivers for Singtel remain Bharti and Singapore mobile. Optus and NCS profitability is still sluggish. Optus requires significant realignment of cost to improve on its persistently paltry returns of 0.8% ROE (annualised). NCS is in an investment phase in building up its IT headcount, especially in more competitive geographies.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

May 13th - Things to Know Before the Opening Bell

May 13th - Things to Know Before the Opening Bell BRC Asia Ltd - Bountiful five years ahead

BRC Asia Ltd - Bountiful five years ahead Oversea-Chinese Banking Corp Ltd - Non-interest income the growth driver

Oversea-Chinese Banking Corp Ltd - Non-interest income the growth driver