Asian Pay Tv Tr - Stock Analyst Research

| Target Price* | 0.130 |

| Recommendation | BUY› BUY |

| Market Cap* | - |

| Publication Date | 21 Nov 2022 |

*At the time of publication

Asian Pay Television - Trust Huge drag from currency

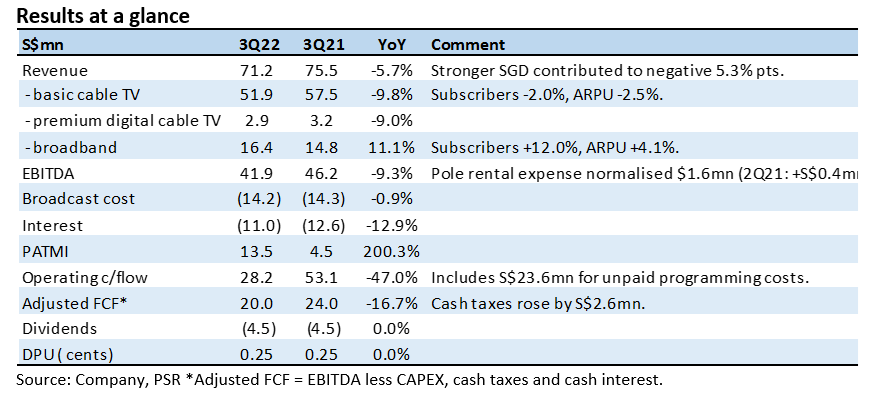

- 3Q22 earnings was below expectations due to the 5% weakness in the Taiwan dollar. YTD22 revenue and EBITDA were at 73%/71% of our FY22e estimates. 3Q22 distribution was maintained at 0.25 cents per unit.

- FY23e distribution is raised 5% to 1.05 cents, paid half yearly. Broadband enjoyed healthy 11% revenue growth, but weakness in basic cable dragged group revenue to fall 6% YoY.

- We lowered our EBITDA by 6% as we cut our Taiwan dollar forecast. Our BUY recommendation is unchanged, but we lower our target price to S$0.13 (prev. S$0.15). based on 8.5x FY23e EV/EBITDA, a 20% discount to Taiwanese peers. The current dividend yield of 9.6%, or S$19mn payout, is supported by free cash flows of around S$73mn p.a.

The Positive

+ High margin broadband growth. Broadband continues to grow strongly led by higher subscriber growth and improvement in ARPU. Monthly subscribers expanded by 9k to 307k as marketing efforts together with wireless operators continue to gain traction. ARPU has risen 4% YoY to TWD379 (S$16.72) with more subscribers opting for higher speeds.

The Negative

– Rising broadcast and content costs. Despite the 10% decline in basic cable TV revenue to S$51.9mn, content cost was stable at S$14.2mn. As a percentage of revenue, content cost in this quarter is a record 30.4% (excluding non-subscription revenue) of cable TV revenue.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU