DBS Group Holdings Ltd - Lower provisions drove earnings

17 Feb 2022- FY21 earnings of S$6.8bn met our estimates as higher fee income and strong loans growth offset lower NIMs. 4Q21 DPS rose 9% to 36 cents.

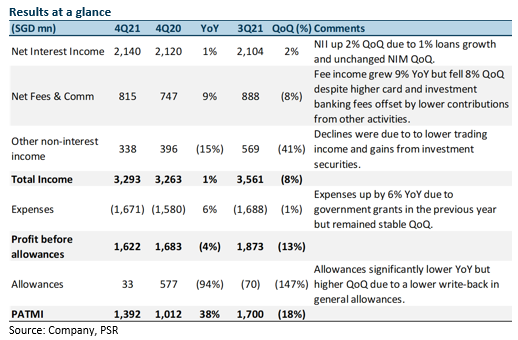

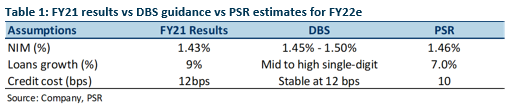

- NIM fell 6bps YoY to 1.43% but loan growth of 9% YoY cushioned NII. NIM remained flat QoQ. SPs down 1% to 67mn in 4Q21.

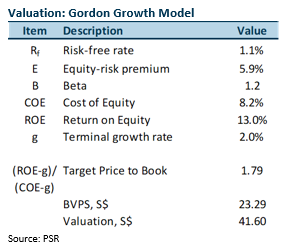

- Maintain ACCUMULATE with a higher GGM TP of S$41.60, up from S$35.90. We raise FY22e earnings by 2% as we raise NII estimates for FY22e. We now assume 1.79x FY22e P/BV in our GGM valuation, up from 1.56x, as we raise our ROE estimates to 13.0%. For FY22e, management guided benign provisions, continued growth in loans and stable NIMs. We believe there is upside to NIM guidance. A 50bps move in interest can raise our earnings by 13%.

The Positives

+ Fee income grew 9% YoY. Fee income growth YoY was broad-based and was led by wealth management and transaction services. However, fee income fell 8% QoQ despite higher card and investment activities which were offset by seasonally lower WM fee income. Full-year fee income grew by 15% YoY to a record S$3.52bn as economic and market conditions improved.

+ Asset quality stable, FY21 total allowances at S$52mn. 4Q21 total allowances were significantly lower YoY but higher QoQ due to a lower write-back in GPs. SPs fell 82% YoY to S$67mn (6bps) but remained relatively unchanged QoQ. Full-year allowances fell 98% YoY to S$52mn due to repayments of weaker exposure, credit upgrades and transfers to non-performing assets resulting in general allowance write-backs during the year. Full-year credit cost of 12bps is below pre-pandemic levels. Management has guided similar allowances for FY22e.

+ Loan growth up 9% YoY in 4Q21. Loan growth was led by non-trade corporate loans with growth led by drawdowns in Singapore and Hong Kong. Housing and WM loan growth was sustained at the previous quarter’s levels. Full-year loan growth of 9% was the highest in seven years as growth was recorded across the region and a range of industries. Management has guided FY22e loan growth of mid to single-digit or better.

The Negative

– NII and NIMs remain relatively unchanged. NIM remained flat QoQ but declined 6bps YoY to 1.43% as a result of lower market interest rates as customer deposits grew 3% QoQ to S$502bn. NII grew 2% QoQ to S$2.1bn as higher loan and deposit volumes were moderated by stagnant NIMs. Management guided similar FY22e NIMs of 145-150bps.

Outlook

Business momentum strong: Despite economic uncertainties from Singapore’s return to Phase 2 (Heightened Alert), loans and transaction pipelines are expected to be strong.

GP reserves sufficient: With its capital position and liquidity – CET-1 ratio of 14.4% in 4Q21 vs 13.9% in 4Q20 – well above regulatory requirements and high allowance reserves, we believe the bank has sufficient provisions to ride out current economic uncertainties. If we were to include the acquisition of Citigroup’ Taiwan consumer banking business and MAS’ operational risk penalty, the CET-1 ratio of 13.3% is still at the upper end of DBS’ target operating range. 4Q21 DPS is up 9% to 36 cents, above pre-pandemic levels.

Upside from higher rates: DBS mentioned that a 1 bps rise in interest rates could raise NII by $18mn-20mn (or NII sensitivity of 2% for every 10bps). Assuming two rate hikes of 50bps this year, our FY22e NII can climb S$2bn (or 21%) resulting in an increase in our FY22e PATMI by 26%.

Benign provisioning cycle. DBS guided credit cost of 12 bps. This is below the pre-pandemic FY18/19 credit cost of 19/20bps. The lower credit cost is due to lower SPs and an improving environment.

Investment Action

Maintain ACCUMULATE with a higher target price of S$41.60, up from S$35.90.

We raise FY22e earnings by 2% as we raise NII estimates for FY22e. We now assume 1.79x FY22e P/BV in our GGM valuation, up from 1.56x, as we raise our ROE estimates to 13.0%.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU