LHN Limited -Tapping into evolving real-estate trends

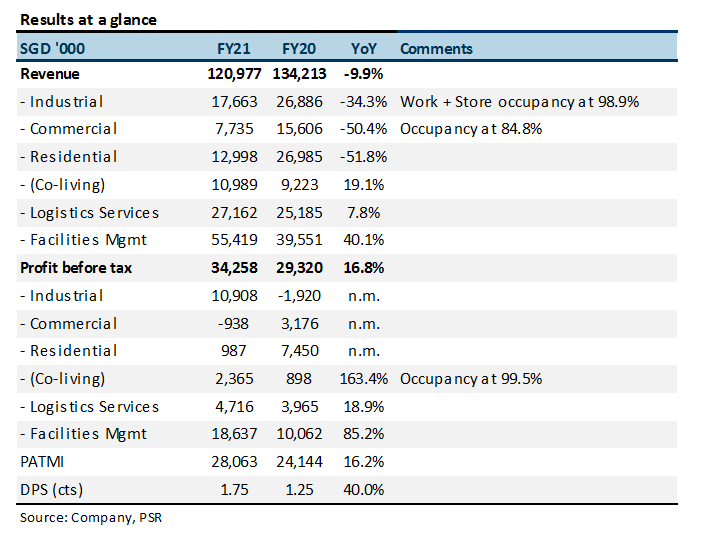

1 Dec 2021- FY21 results were below expectations. FY21 revenue and PATMI at 89%/84% of our forecasts. Revenue from commercial and residential properties and facilities management were lower than expected.

- Maintain BUY with a lower TP of S$0.49 from S$0.54. We roll over our P/E target to FY22e or 7x PE. Our FY22e PATMI has been lowered by 16% as we reduce our forecast revenue for the same segments mentioned. Industry is trading at 14x FY22e, down from 19x. Growth for FY22e includes the five new Coliwoo co-living properties and a new Work Plus Store outlet at 202 Kallang Bahru.

The Positives

+ Higher profit contribution from industrial and co-living properties. FY21 PATMI increased 16% to S$28.1mn. Profit before tax for Coliwoo co-living properties in FY21 was almost thrice that of S$898k in FY20. Industrial properties turned around from a net loss of S$1.9mn in FY20 to a net profit of S$10.9mn in FY21.

+ Higher revenue and profit from facilities management. Profit before tax for facilities management jumped 85%, driven by the joint venture acquisition of Bukit Timah Shopping Centre carpark in December 2020 and the acquisition of 33 JTC carparks in January 2021. There was also an increase in facilities management services amid the pandemic.

The Negatives

– Lower revenue due to streamlining of operations. Revenue contribution from industrial properties decreased due to the expiry of four master leases in FY20. Revenue contribution from commercial properties was lower due to the expiry of three master leases in FY21.

– Commercial properties suffered net loss. Commercial properties swung from a net profit of S$3.2mn in FY20 to net loss of S$938k in FY21. This was mainly due to the lower demand for offices amidst the prolonged work-from-home trend becoming the new normal.

Other updates

Aggressively expanding Coliwoo portfolio. There are five residential properties expected to commence operations in FY22 under the Coliwoo co-living portfolio. Most recently, a Mount Elizabeth Property was acquired, which will be part of LHN’s expansion of its Coliwoo portfolio. It is a residential property with a Gross Floor Area of approximately 104,375 sqft, and 22 storeys. Excluding the Mount Elizabeth Property, we expect five properties to add 200 keys, representing a 25% increase for FY22. The strong momentum of demand for these properties is also expected to continue, with the trend of more millennials moving out, the work-from-home trend becoming the new normal and a gradual reopening of borders.

Proposed spin-off and separate listing of LHN Logistics on Catalist. LHN has submitted a spin-off application to The Stock Exchange of Hong Kong Limited for the proposed spin-off and separate listing of the shares of LHN Logistics Pte Ltd, which will hold the logistics services business of LHN. It is expected that LHN will continue to hold majority shareholding in LHN Logistics, which will remain consolidated with LHN.

The Stock Exchange of Hong Kong Limited and Singapore Exchange are still considering the applications and there is no assurance that the proposed spin-off will be approved.

Maintain BUY with a lower TP of S$0.49, from S$0.54

We have a lower TP of S$0.49, from S$0.54. FY22e PATMI has been lowered by 16% to S$33.8mn as we lower our forecasts of contribution from residential and commercial properties and facilities management. The outlook continues to remain strong for all business segments, especially space optimisation, as we adapt to the new normal. Higher demand for co-living and self-storage spaces are expected.

We now peg the stock to 7x FY22e P/E, down from 9.5x FY22e P/E, still a 50% discount to the industry average.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU