Sheng Siong Group Ltd - Tough comparison but better-than-expected sales

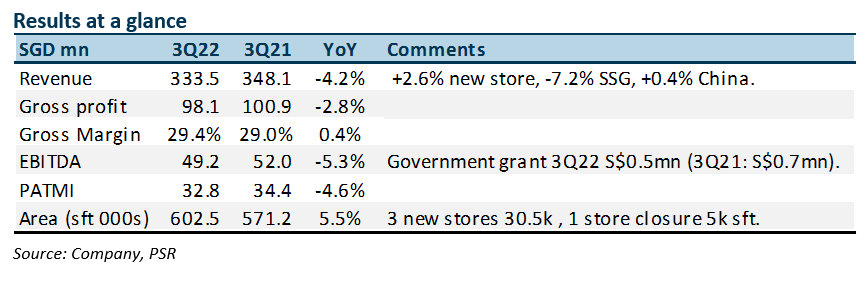

31 Oct 2022- 3Q22 revenue and PATMI beat expectations. YTD22 revenue and PATMI were 78%/82% of our FY22e forecast.

- Same-store sales declined 7% YoY in 3Q22, as it was a tough base year. In 3Q21 Jurong Fishery Port and Pasir Panjang Wholesale Centre closure diverted huge fresh food sales to Sheng Siong stores. The four new stores added 2.6% points of revenue growth.

- We lift FY22e earnings by 5% to S$127.8mn. The increase in GST from 1 January 2023 could also pull some sales into 4Q22. Our BUY recommendation is maintained. The target price is unchanged at $1.86. Valuation is pegged to 22x PE, a 10-15% discount to the 5-year historical average of 25x PE. Revenue is normalising post-relaxation of COVID-19 restrictions but at a run-rate around 25% higher than the pre-pandemic period. We believe Sheng Siong’s strength in fresh food continues to drive its grocery market share.

The Positives

+ Still healthy margins. The higher contribution from fresh food helped Sheng Siong (SSG) margins to creep up. The ability to manage fresh food effectively from direct sourcing to processing (meat/seafood) in the stores gives SSG the edge over peers, in our opinion. Food inflation has also seen the downgrading by consumers into SSG higher margin house brands. To cater to the store expansions, SSG will need a larger distribution centre with more automation and specialised equipment

+ Store roll-out normalising. This quarter SSG added a new 10,000 sft store in Margaret Drive. Meantime there was a closure of a 5,000 sft Yishun store. The increase in the store footprint in 3Q22 was 5.5% YoY. A new 6,000 sft store in Sanja Valley will be added in 4Q22. This will increase total sft in FY22e to 608k sft, a 5% rise. Expectations are for 3 to 5 new stores per annum over the next five years.

The Negative

– Weak same-store sales. 3Q22 same-store sales are down 7.2% YoY. It is the 2nd consecutive quarter of decline in same-store sales and accelerating from the 2Q22 5% decline. Since the relaxation of COVID-19 control measures in April, we expect less home dining as household activities normalise.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU