Silverlake Axis Ltd - Earnings dip due to change in revenue mix

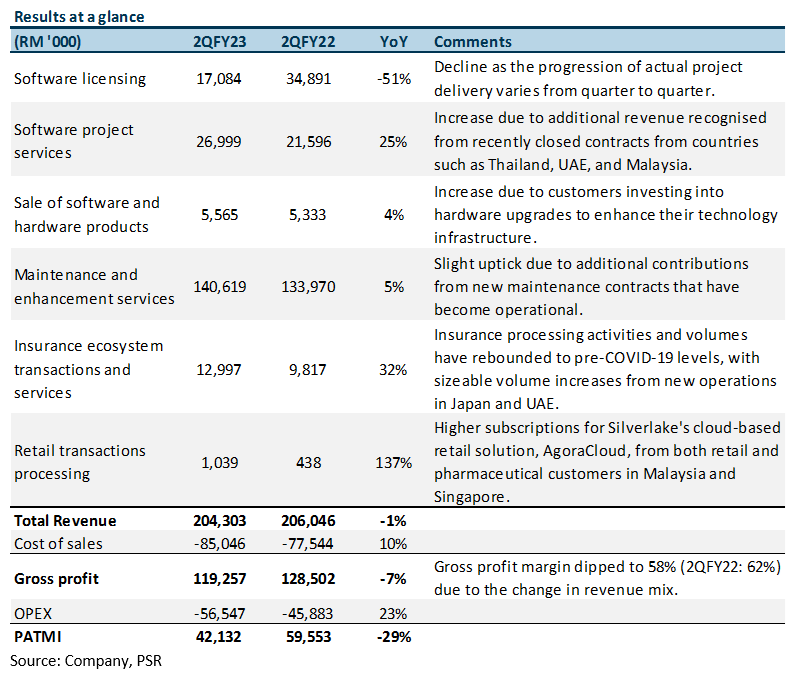

16 Feb 2023- 2QFY23 earnings of RM42.1mn were in line with our estimates despite a dip. 1HFY23 earnings were at 48% of our FY23e. The 29% YoY dip in earnings came from a drop in gross profit margin due to the change in revenue mix as lower project-related revenue was slightly offset by higher recurring revenue.

- Project-related revenue comprising software licensing and software project services fell 22% YoY as the progression of actual project delivery varies from quarter to quarter, while recurring revenue rose 7% YoY due to additional contributions from new maintenance contracts that have become operational.

- We maintain BUY with an unchanged target price of S$0.49. Our FY23e estimates remain unchanged. Our FY23e estimates remain unchanged. Our target price is pegged to 20x P/E FY23e. We expect MOBIUS and the recovery in bank IT spending after two cautious pandemic years to be the key growth drivers for the company.

The Positives

+ Recurring revenue rose 7% YoY. Recurring revenue comprises maintenance and enhancement services, insurance ecosystem transactions and services, and retail transactions processing revenue. Maintenance and enhancement services increased 5% YoY to RM141mn as the dip in enhancement services revenue was more than offset by the increase in maintenance revenue, due additional contributions from new maintenance contracts that have become operational. Furthermore, the decline in enhancement services revenue is temporary as the Group will direct more resources to fulfil their enhancement services contract backlog in 2HFY23. Insurance ecosystem transactions and services revenue increased 32% YoY as volumes have rebounded to pre-COVID-19 levels, with sizeable volume increases coming from new operations in Japan and the UAE. Revenue from retail transactions processing also surged 137% YoY mainly due to higher subscriptions for Silverlake’s cloud-based retail solution, AgoraCloud, from both retail and pharmaceutical customers in Malaysia and Singapore.

+ Order backlog healthy. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the 5 largest Southeast Asia-based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.8bn (1QFY23: RM2.1bn), with an order backlog of RM275mn on the verge of closing in 3QFY23. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

– Project-related revenue fell 22% YoY. Software licensing revenue fell 51% YoY to RM17mn. This was mainly due to the progression of actual project delivery varying from quarter to quarter, resulting in a lag in revenue contribution. However, this was offset by software project services revenue increasing 25% YoY to RM27mn as there was additional revenue recognised from recently closed contracts from countries such as Thailand, UAE, and Malaysia. As for the ongoing implementation of two new MOBIUS contracts secured in FY22, one has been completed and went live in 2QFY23 while the other is near completion and will be entering maintenance mode sometime in mid-2023.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

About the author

Glenn Thum

Research Analyst

PSR

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.

PayPal Holdings Inc - Consumer spending remains resilient

PayPal Holdings Inc - Consumer spending remains resilient Cromwell European REIT - A resilient 1Q24

Cromwell European REIT - A resilient 1Q24